Can TVF Pop the AI Bubble?

A stress test of the financing cycle behind artificial intelligence.

There is a lot of noise around the AI bubble debate.

Some people treat AI as if it is obviously the next industrial revolution. Others treat it as if the whole thing is one giant speculative cycle waiting to collapse. Both views are too clean. AI can be useful, economically important and still be financed too aggressively in certain parts of the system.

In our previous AI cycle post, we looked at the full chain behind AI: physical inputs, compute supply, datacenter infrastructure, cloud, models, data, applications and the final financial return. This post is narrower. We are not going to rebuild the entire chain again, and we are not trying to prove that AI is fake.

We are stress testing the financing.

The question is simple: can the financing cycle around AI survive until the cashflows arrive?

That means looking at the gap between capital committed today and profits generated tomorrow. It means looking at circular financing, leverage, private credit, leases, purchase commitments and the moment where the bottleneck may shift from compute to cash.

TVF cannot literally pop the AI bubble. But we can test where it would be weakest.

Disclaimer

Do you appreciate our publication? Then you help us enormously with a like, comment, share and/or restack.

Chapter 1: The Infrastructure Paradox

The most interesting thing about the AI bubble debate is that both sides can be right at the same time.

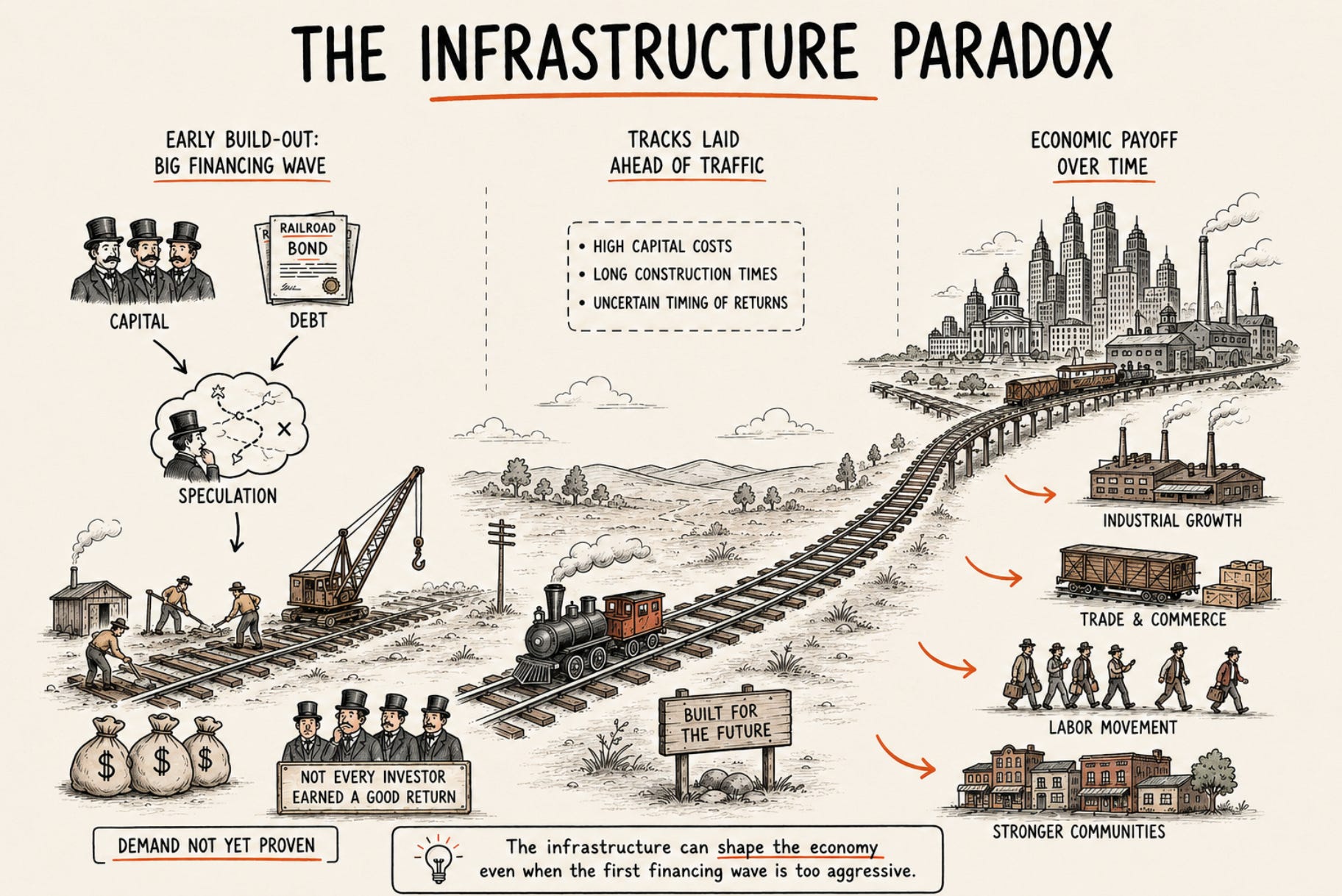

AI can become one of the defining technologies of the next decade, while the first financing wave around it still becomes too aggressive. Large infrastructure cycles often work this way. Railroads reshaped trade, cities, labor mobility and industrial growth, but the build-out was also financed with enormous amounts of capital, debt and speculation. Tracks were laid before demand was fully proven, investors funded future traffic before the traffic existed, and many projects only worked as long as financing remained available. The economy was changed for decades, but that did not mean every railroad investor earned a good return.

Telecom fiber followed a similar pattern. The internet was real, and the world eventually needed far more bandwidth than it had before. But during the first build-out, companies financed too much capacity too quickly, often with capital structures that assumed demand would arrive on schedule. The infrastructure became useful later. The timing and financing were the problem earlier.

That is the right lens for AI. The relevant question is not whether AI matters. It probably does. The question is whether today’s financing cycle is building the right infrastructure at the right price, with enough time for real cashflows to catch up.

A technology can shape the next decade while parts of the financing behind it still break. A datacenter can be useful and still be overpaid for. A cloud contract can be real and still depend on optimistic assumptions. A model can be powerful and still fail to generate enough margin after compute costs. A company can report strong AI revenue and still destroy value if the capital required to produce that revenue earns a poor return.

Infrastructure bubbles usually break in that gap. The story does not have to die. It only has to need more capital than the market is willing to provide before the cashflows are large enough to carry it.

Chapter 2: Not All Capex Is Equal

The railroad comparison is useful, but only if we understand where it breaks.

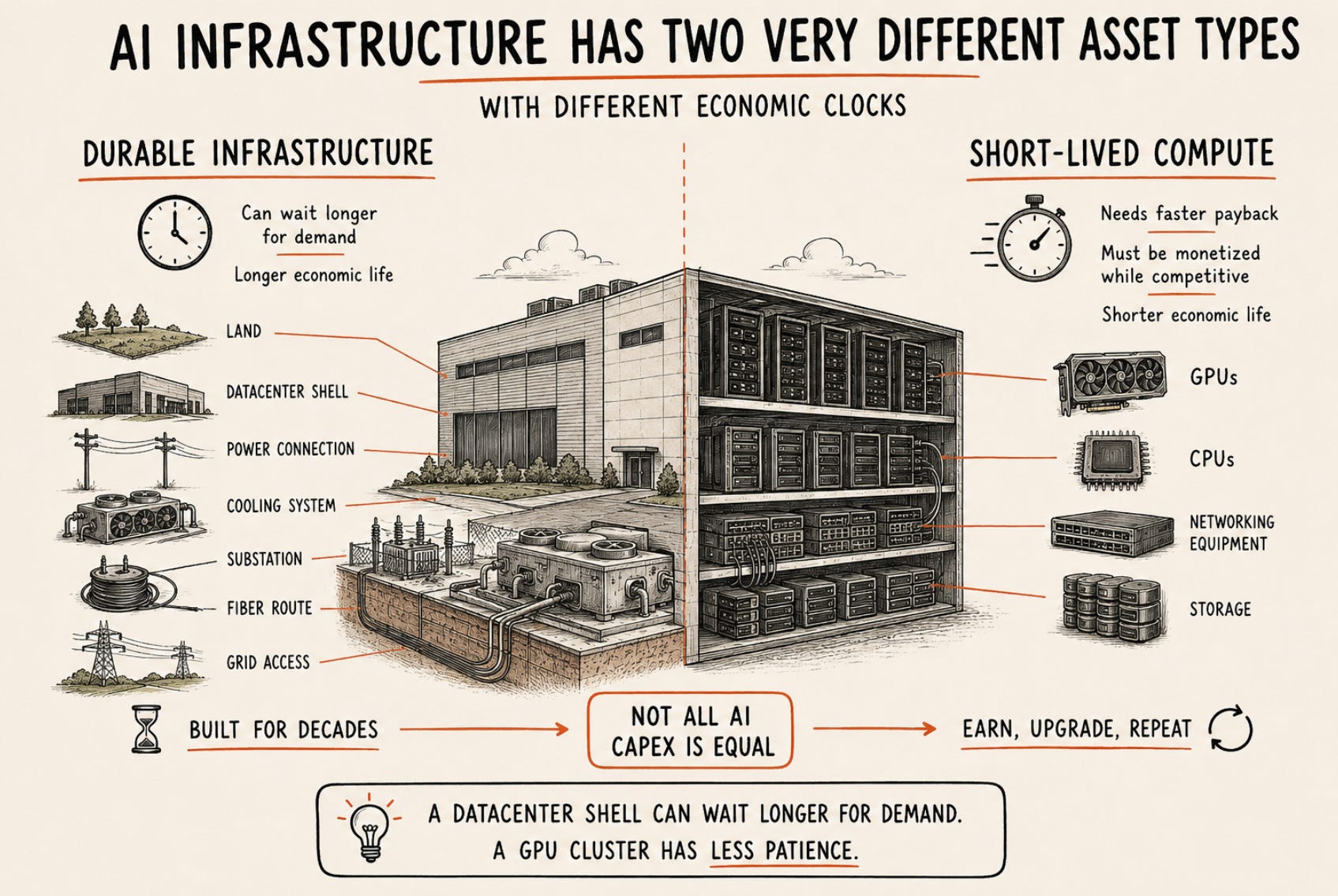

Railroads required enormous upfront investment before the economics were visible, but the physical asset could remain useful for decades. Even when the first owners failed, the tracks continued to shape trade, cities and industrial development long after the original capital structure was gone.

AI has a similar timing problem, but the asset mix is different. Part of the build-out looks like classic infrastructure: land, datacenter shells, power connections, cooling systems, substations, fiber routes and grid access. These assets can have long economic lives if they are located in the right places and tied to real demand. But a large part of current AI spending sits inside the building: GPUs, CPUs, servers, networking equipment and storage. Those assets behave less like railroad tracks and more like high-end production equipment in a fast-moving technology cycle.

Durable infrastructure can wait for demand longer than short-lived compute can. A railroad track can be underused for a while and still become valuable later if traffic eventually arrives. A datacenter shell can retain strategic value if power, land and connectivity remain scarce. A GPU cluster has less patience. It needs to be installed, powered, cooled and monetized while it is still competitive.

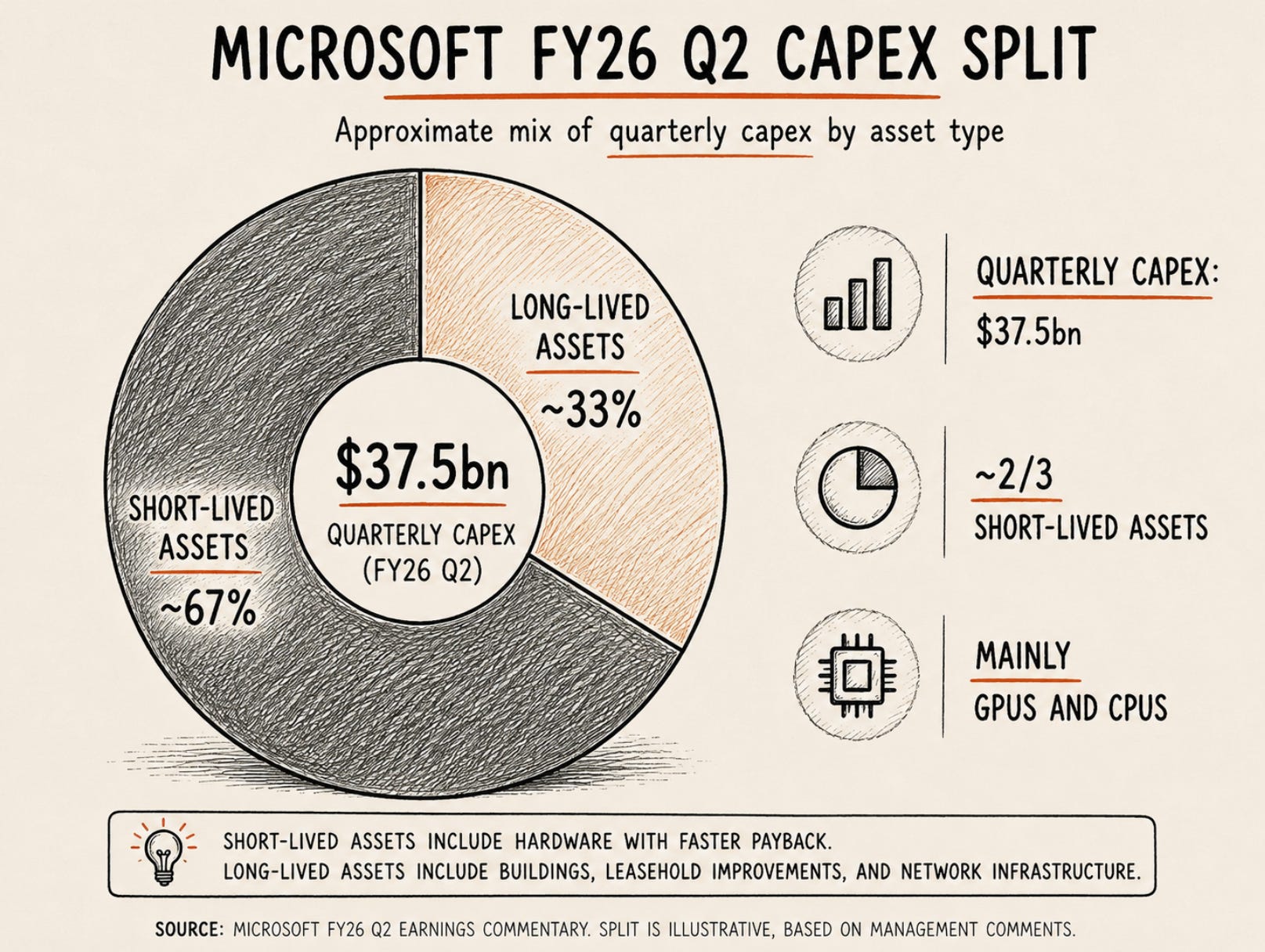

Microsoft made this distinction unusually clear in its FY26 Q2 earnings. The company reported $37.5 billion of capital expenditures in one quarter, and roughly two thirds of that spend went to short-lived assets, primarily GPUs and CPUs. In simple terms, around $25 billion of one quarter’s capex was tied to compute assets that need a faster payback than land or buildings.

The useful-life disclosures from other companies point in the same direction. Microsoft usually depreciates computer equipment over two to six years, while buildings and improvements last much longer. Alphabet depreciates servers and networking equipment over a shorter period than datacenter buildings. Amazon shortened the useful life of a subset of servers and networking equipment from six years to five years from 2025, citing the faster pace of technology development, especially in artificial intelligence and machine learning. Meta moved the other way by extending the useful life of most servers and network assets to 5.5 years, which lowered depreciation expense.

The headline capex numbers are now too large for this to be an accounting footnote. Alphabet guided for 2026 capital expenditures of roughly $175–185 billion, up from $91.45 billion in 2025. Meta raised its 2026 capex outlook to $125–145 billion, including principal payments on finance leases. Amazon reported $128.3 billion of cash capital expenditures in 2025, up from $77.7 billion in 2024, while free cash flow fell from $38 billion to $11 billion as property and equipment purchases increased sharply.

The strongest counterargument is that these companies can afford it. Microsoft, Alphabet, Amazon and Meta still have enormous profit pools, real customers and strategic reasons to build before competitors do. But the stress test is not whether they can spend the money. It is whether the incremental capital earns enough return after depreciation, power, maintenance, replacement cycles and financing costs.

The first weakness in the AI financing cycle is therefore not simply that capex is high. The more precise concern is that a meaningful part of AI capex has a short economic clock. If the end-market cashflows arrive quickly enough, the spending can be justified. If they do not, the infrastructure may still matter while the first financing wave turns out to have been too expensive.

Chapter 3: The Bubble Needs Air

A bubble does not have to be bad.

In large infrastructure cycles, capital often arrives before the economics are fully proven. Railroads were not funded by daily ticket sales. They were funded by investors who believed future traffic would eventually justify the tracks. That belief created speculation, debt and losses, but it also helped build infrastructure that shaped the economy for decades.

AI may work in a similar way. The current bubble is not only made of hype. It is made of real companies, real contracts, real infrastructure and real demand for compute. The question is whether the bubble is being filled by cashflows that already exist, or by capital that assumes those cashflows will arrive later.

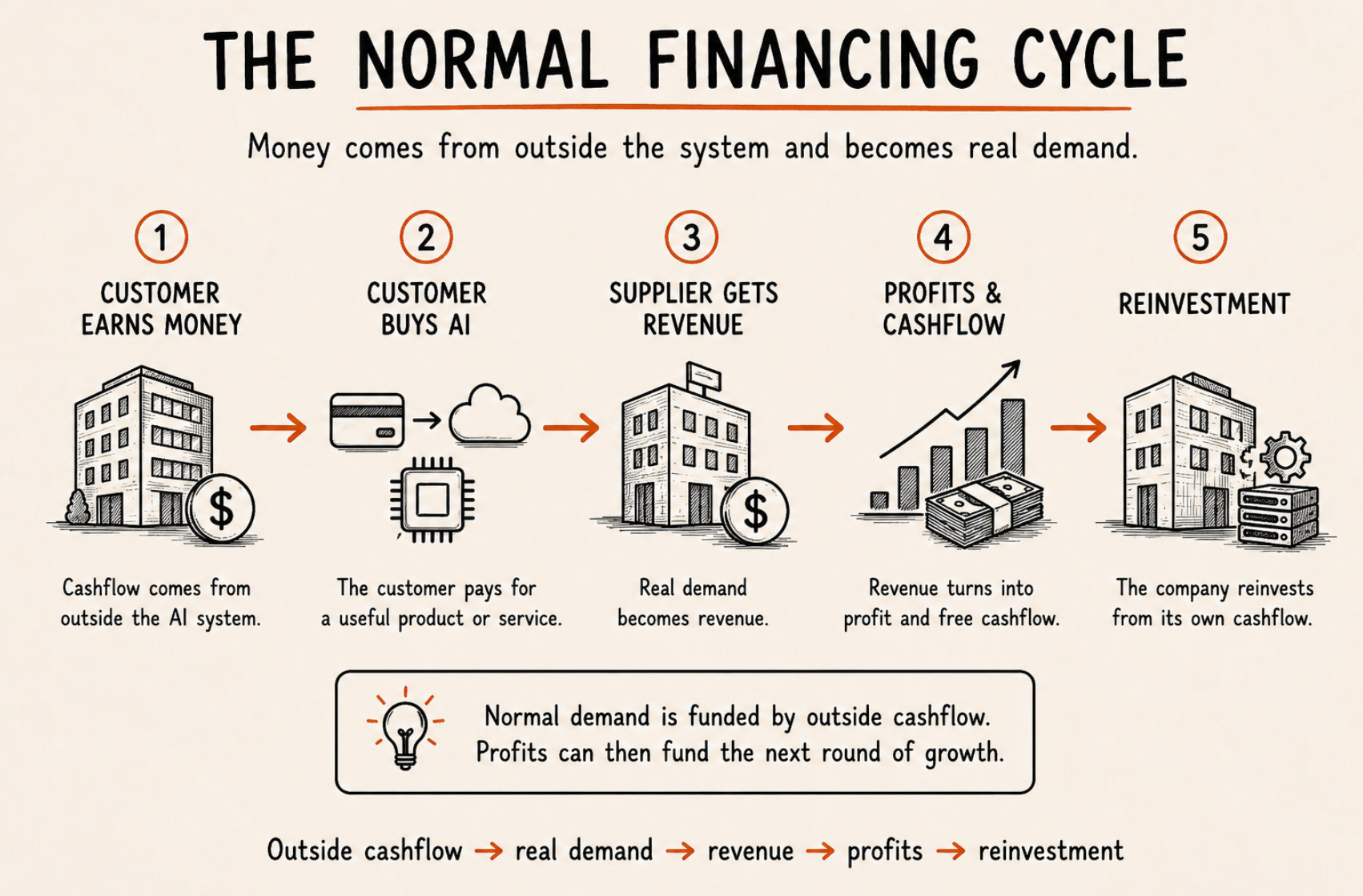

In a normal financing cycle, money comes from outside the system. A customer earns cashflow from its own business, uses part of that cashflow to buy a useful product or service, and the supplier turns that demand into revenue. If the supplier earns attractive profits, it can reinvest from its own free cashflow. That is the clean version of demand: outside cashflow becomes real demand, real demand becomes revenue, and revenue becomes profits that fund the next round of growth.

The AI cycle is less clean because capital often enters before the end-market economics are fully proven. Investors, strategic partners, cloud providers or suppliers inject money into the system. That money gives AI labs or infrastructure companies purchasing power. Purchasing power becomes chip orders, cloud commitments and datacenter contracts. Those commitments become revenue and backlog for suppliers. Revenue and backlog support higher valuations. Higher valuations then make it easier to raise more capital.

That is how the AI bubble expands: capital creates demand, demand supports valuation, and valuation attracts more capital.

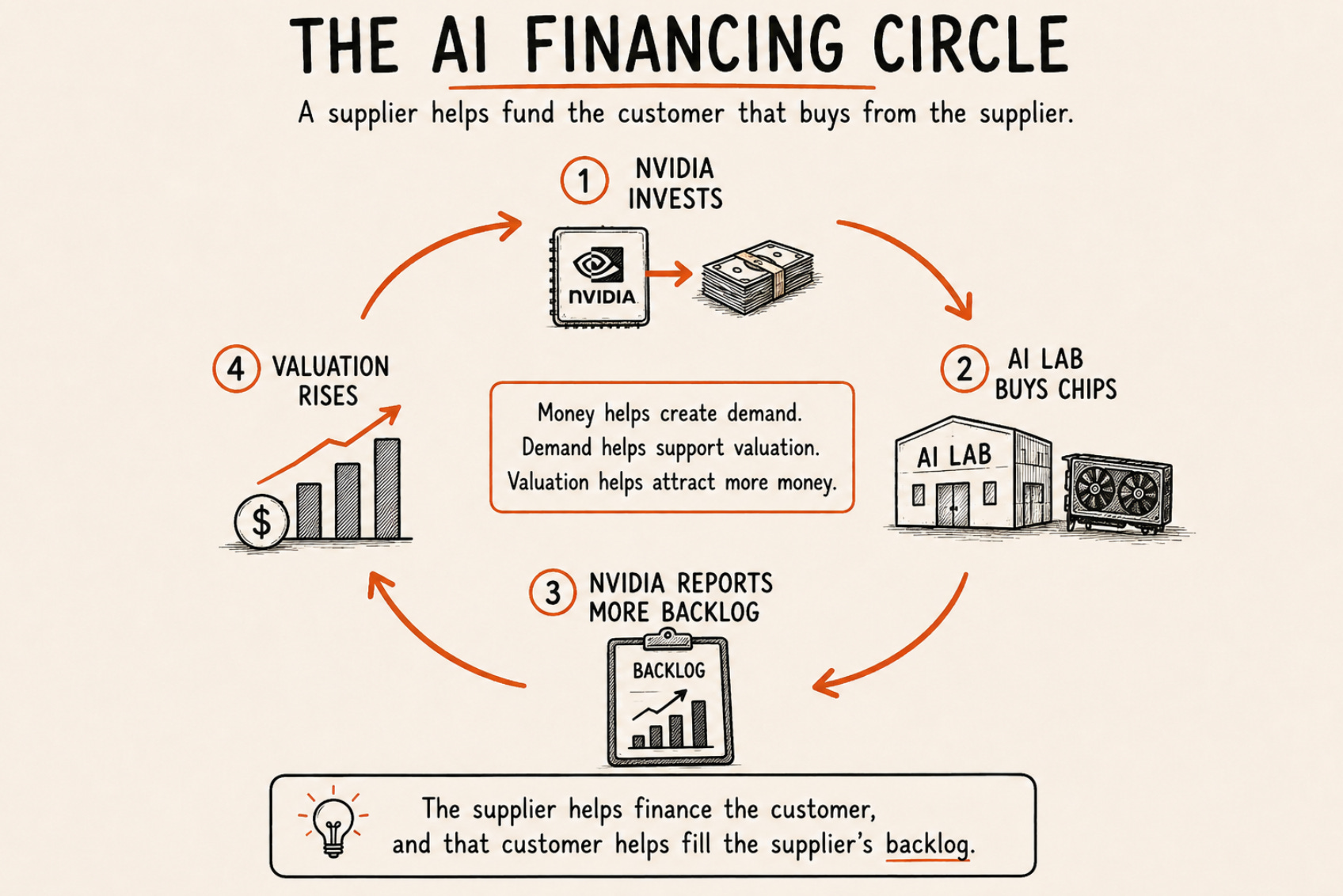

The clearest example is Nvidia and OpenAI. Nvidia announced plans to invest up to $100 billion in OpenAI, while OpenAI would use Nvidia systems for a massive AI infrastructure build-out. The strategic logic is easy to understand. OpenAI needs enormous compute capacity. Nvidia controls the most important compute ecosystem. Both sides want to secure the relationship before the market becomes more competitive.

But financially, the loop is also clear. The supplier of the scarce input helps finance one of the largest buyers of that input. OpenAI’s infrastructure ambitions create demand for Nvidia systems. That demand supports Nvidia’s revenue outlook and valuation. Nvidia’s valuation gives it more capacity to invest, partner and defend its position in the AI stack. The system feeds itself.

That does not make the demand fake. OpenAI really needs compute, and Nvidia really supplies the infrastructure that makes frontier AI possible. The problem is that the demand signal becomes less independent. A customer buying chips from profits generated outside the AI ecosystem is one kind of demand. A customer buying chips while being financed by the same ecosystem that benefits from those purchases is another.

Oracle shows where this circularity becomes visible in reported backlog. OpenAI reportedly agreed to buy around $300 billion of computing power from Oracle over roughly five years. For Oracle, that is a huge demand signal. It supports cloud backlog, datacenter expansion and the idea that Oracle has become a central AI infrastructure player. But the quality of that backlog still depends on OpenAI’s ability to raise capital, grow revenue and eventually turn AI usage into profitable cashflow.

Together, Nvidia and Oracle show two sides of the same financing bubble. Nvidia shows supplier-financed demand. Oracle shows how that demand becomes backlog for infrastructure providers. OpenAI sits in the middle, turning capital into compute commitments before the full end-market economics are proven.

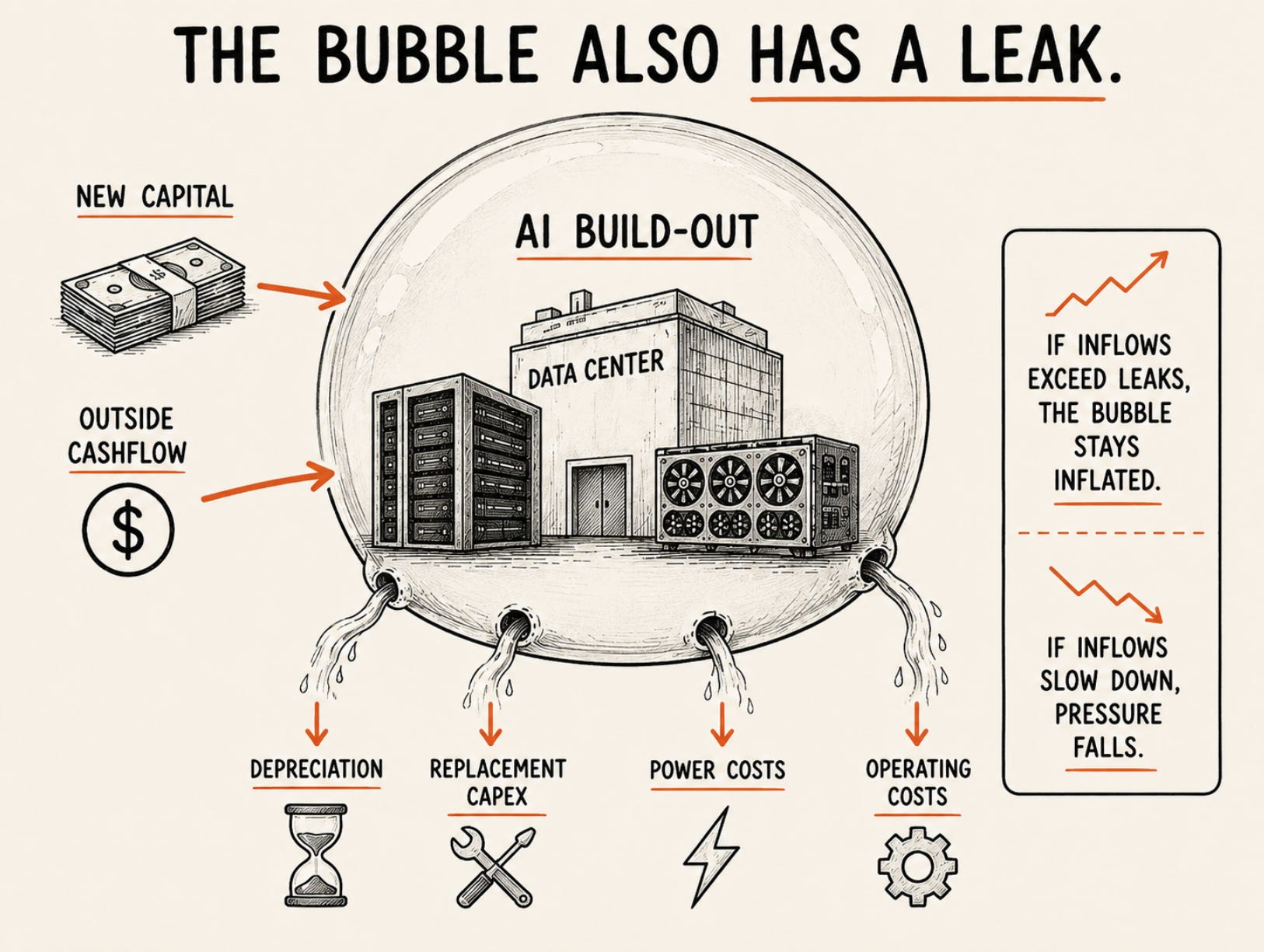

The bubble also has a leak.

AI infrastructure is not only land, buildings and power connections. A large part of the spending goes into GPUs, servers and networking equipment that age quickly. Those assets have to be replaced, upgraded and monetized while they are still competitive. So the system does not only need capital to grow. It also needs capital to offset depreciation, replacement capex, power costs and operating expenses.

That is why the AI bubble does not have to pop in one dramatic moment. It can also leak. If new capital keeps entering faster than depreciation and replacement capex drain it, the bubble can keep expanding. If capital becomes more selective, or if external customer cashflows grow too slowly, pressure starts to fall. Capex slows, backlog becomes less valuable, suppliers lose visibility and valuations compress.

Chapter 4: Measuring the Wall

A bubble is not only about how much air is inside it. It is also about the wall that holds the air in.

For AI, the air is invested capital. Every dollar of capex, debt, equity, lease financing, strategic investment or private-credit funding increases the size of the bubble. The wall is different. The wall is the financial structure that keeps that capital in place long enough for cashflows to arrive.

A simple way to picture this is a bicycle tire. Two tires can hold the same amount of air, but they do not have the same strength. One may be thick, new and well-supported. The other may be patched, thin and under pressure. The amount of air can be identical. The risk is completely different.

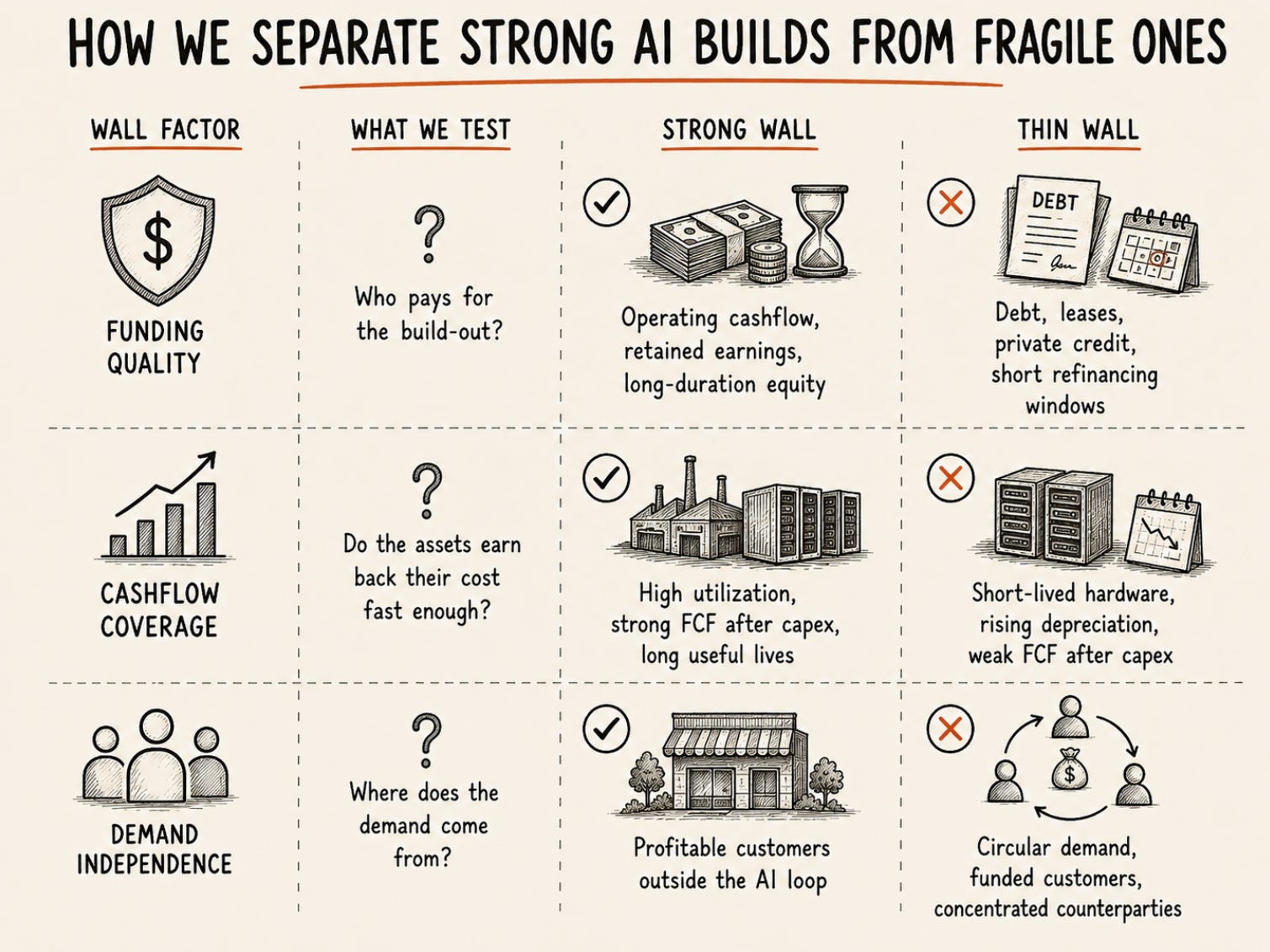

For TVF, the wall has three parts: funding quality, cashflow coverage and demand independence.

Funding quality

Funding quality asks who pays for the build-out.

On this test, AI still scores relatively well at the core. Microsoft, Alphabet, Amazon and Meta are not speculative shells. They have real profit pools in software, search, advertising, cloud, commerce and enterprise distribution. This is what makes the current AI bubble stronger than many weaker bubbles. The biggest companies inflating it have actual cash machines underneath them.

But the score is no longer perfect. AI capex has become so large that the system is increasingly reaching beyond internal cashflow. Reuters reported that AI-related debt sales are already reshaping global corporate bond markets, with Amazon raising a record €14.5 billion in euro bonds and Alphabet setting borrowing records in several non-dollar markets. Hyperscaler debt issuance has become large enough to push U.S. non-financial corporate borrowing in European markets above €60 billion in 2026.

That does not mean the wall is weak. It means the wall is no longer made only of operating cashflow.

Meta shows the same change through structure. The company raised its 2026 capex outlook to $125–145 billion, including principal payments on finance leases, and agreed to a $27 billion financing structure with Blue Owl Capital for its Louisiana datacenter project. Meta keeps a minority equity interest, while Blue Owl-managed funds own the majority of the joint venture. This can be smart capital allocation, because it allows Meta to build more capacity without carrying the full project directly on its own balance sheet. But it also means part of the wall is now built with external capital structures that depend on lease terms, project economics and investor appetite.

CoreWeave is the more leveraged version of that same pressure. It secured $8.5 billion through a delayed-draw term loan facility to expand its AI cloud platform, bringing its total equity and debt financing commitments over the previous twelve months to around $28 billion. That kind of financing can scale capacity quickly, but it is not the same as Microsoft funding capex from mature operating cashflow. It depends much more directly on customer contracts, lender confidence, asset values and refinancing conditions.

On funding quality, the AI wall is thick at the center and thinner at the edges.

Cashflow coverage

Cashflow coverage asks whether the assets earn back their cost fast enough.

This is where the wall becomes more mixed. AI infrastructure is often described as one long-lived asset class, but that is too simple. Land, datacenter shells, power connections and grid access can last for a long time. GPUs, CPUs, servers and networking equipment have a much shorter economic clock.

Microsoft’s FY26 Q2 numbers make that visible. The company reported $37.5 billion of capex in one quarter, and roughly two thirds of that went to short-lived assets, mainly GPUs and CPUs. This means the AI wall is not only tested by how much capacity gets built, but by how fast that capacity must be monetized before it becomes less competitive.

Amazon shows the same pressure through free cashflow. Its cash capex rose sharply in 2025, while free cashflow fell from $38 billion to $11 billion. That does not make Amazon weak, but it shows how quickly AI infrastructure spending can absorb even very strong operating cash generation.

A fully utilized AI cluster with strong pricing can support the wall. An underutilized cluster leaks pressure. If the cashflow arrives quickly, short-lived compute is not a problem. If it arrives slowly, the hardware clock keeps moving while the revenue curve is still developing.

On cashflow coverage, the AI wall is medium-strength. The largest companies can absorb the pressure, but the asset mix is demanding. A large part of the AI build-out has to earn its return faster than the infrastructure narrative suggests.

Demand independence

Demand independence asks where the demand comes from.

A contract backed by profitable customers outside the AI ecosystem makes the wall stronger. A contract backed by a customer that still needs repeated funding rounds makes the wall harder to inspect. The revenue can be real in both cases, but the second version depends more on financing conditions.

This is why the OpenAI-linked contracts matter. If a mature enterprise pays for AI out of its own operating budget, the demand is externally validated. If an AI lab signs a massive compute commitment while still needing large amounts of outside capital, the contract may be real, but the wall behind it depends on the lab’s ability to keep raising money, growing revenue and eventually producing durable cashflow.

Oracle is the clearest backlog example. The company’s remaining performance obligations surged with AI cloud contracts, and OpenAI reportedly agreed to buy around $300 billion of computing power over roughly five years. That is a huge demand signal for Oracle. But Reuters also reported that OpenAI expected to burn $115 billion through 2029 as compute spending rises. The question is not whether the contract exists. The question is how much of the future payment capacity is already supported by profitable end-market demand, and how much still depends on the next rounds of capital.

Circularity does not reduce the amount of air in the bubble. It changes the quality of the wall. When suppliers, cloud providers and strategic investors help finance the customers that create their own demand, the market gets revenue, backlog and valuation support before the final customer economics are fully proven. That can be a bridge to a real platform shift. It can also make the wall look stronger than it is.

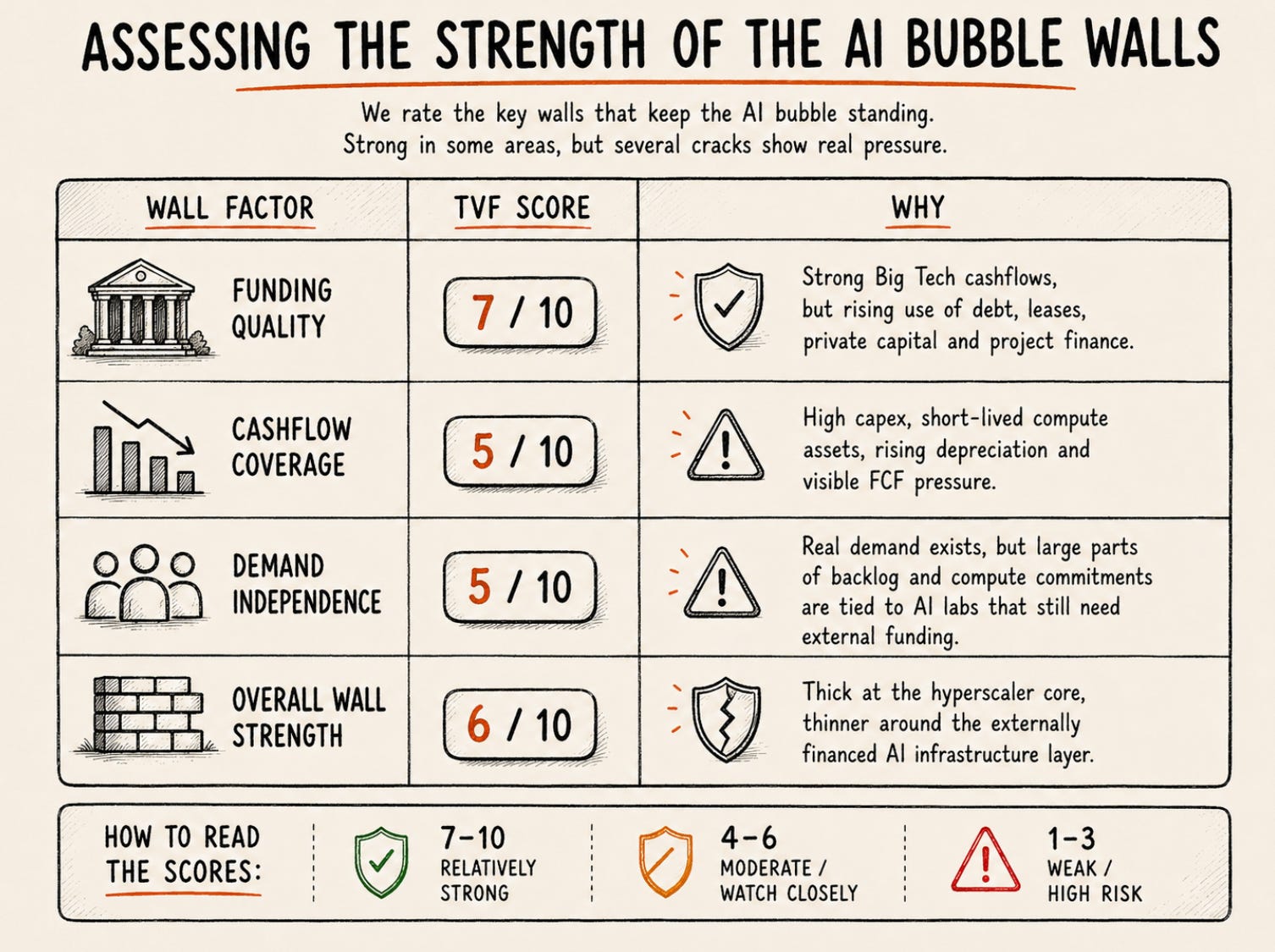

Our wall score

Our rough score would be 6 out of 10: strong enough at the core to avoid calling this a fragile bubble, but not thick enough to ignore the financing risk.

Funding quality gets a 7 out of 10. Big Tech cashflows are still strong, but the rising use of debt, leases, private capital and project finance makes the wall more sensitive to financing conditions.

Cashflow coverage gets a 5 out of 10. The capex is large, a meaningful part of it is tied to short-lived compute assets, and free cashflow pressure is already visible in some places.

Demand independence also gets a 5 out of 10. Real demand exists, but parts of the backlog and compute commitments are tied to AI labs that still need external funding.

That leaves the overall wall at 6 out of 10.

This is not a bubble made of paper. The core is too profitable for that. But it is also not a perfectly solid wall. The structure is strongest where AI spending is funded by internal cashflow, supported by durable assets and paid for by profitable customers outside the AI loop. It becomes thinner where short-lived compute is financed with debt or leases and backed by customers that still depend on the next round of funding.

Chapter 5: Pop, or Leak?

A weak wall does not always break at once.

Sometimes a tire explodes. More often, it slowly loses pressure. The ride becomes heavier, the tire deforms, and only later do you notice that the problem was not one dramatic rupture, but a steady loss of air.

That is probably the better way to think about the AI bubble. The most likely stress scenario is not that AI suddenly stops working. It is that the financing cycle becomes less willing to keep feeding the build-out at the same speed, while depreciation, replacement capex and operating costs keep draining the system from the inside.

A pop is a confidence break

A popping bubble is a break in confidence. A large customer cannot finance its commitments. A major cloud contract is renegotiated. A neocloud misses funding. A private-credit loss forces lenders to step back. Hyperscalers cut capex at the same time. Supplier orders are delayed. Backlog quality is questioned. Valuations reprice quickly because investors no longer trust the chain of commitments.

That is the hard-break scenario. The loop turns in reverse: an AI lab cuts compute spending, the cloud provider delays datacenter expansion, the chip supplier loses order visibility, the datacenter developer loses financing, private lenders step back, valuations fall and the next financing round becomes harder.

A leak is more likely than an immediate pop

A leaking bubble is less dramatic, but still painful. Capex growth slows. AI labs become more careful with compute. Cloud providers prioritize returns over speed. Datacenter projects are delayed rather than cancelled. Suppliers keep growing, but with less visibility. Valuations compress because the market moves from “build at any cost” to “show me the payback.”

Right now, the evidence points more toward leak risk than immediate pop risk. The core of the AI bubble is still supported by very strong companies. Microsoft, Alphabet, Amazon and Meta have large profit pools and can keep investing through disappointment. But the edges of the system are already becoming more sensitive to financing conditions.

Reuters reported that U.S. direct-lending issuance fell to $44.76 billion in the three months through May 2026, down roughly 40% from the first quarter. Lending to private-equity-backed borrowers and leveraged buyouts also dropped sharply. Retail inflows into private credit weakened, and several large managers faced redemption pressure.

That is not an AI-specific collapse, but it matters because private credit is one of the capital sources now being asked to help finance datacenters, neoclouds and infrastructure vehicles.

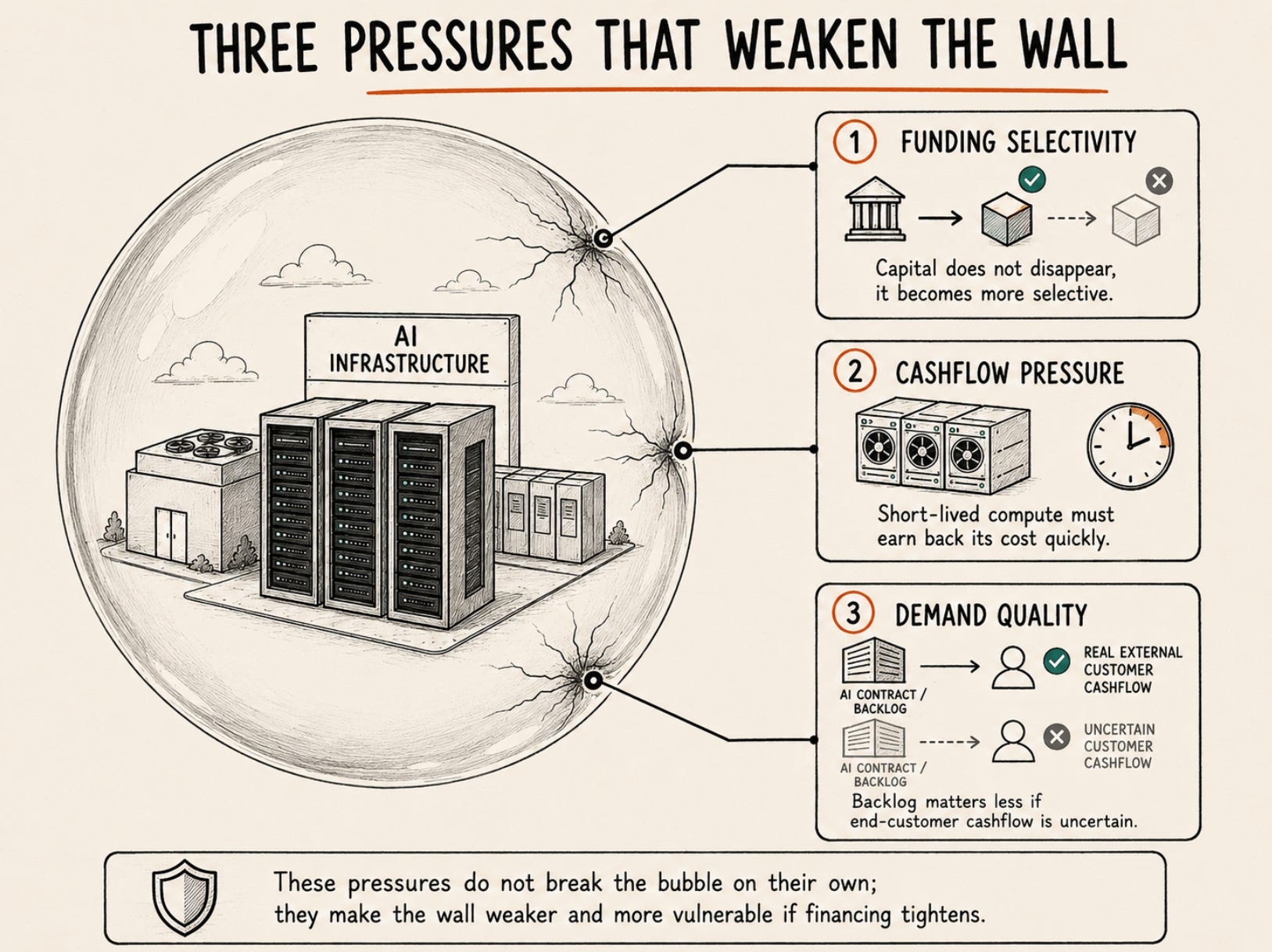

The three leaks

The first leak is funding selectivity. Capital does not vanish everywhere. It moves toward the strongest borrowers. Microsoft, Alphabet, Amazon and Meta can still finance. High-quality datacenter projects with strong hyperscaler tenants can still attract capital. But weaker projects, less transparent structures and more speculative AI infrastructure vehicles face a higher bar.

The second leak is cashflow pressure. A meaningful part of AI capex goes into assets that age quickly. GPUs and servers need utilization while they are still competitive. If utilization is high, the system can absorb the cost. If utilization is lower, or if customers resist pricing, depreciation starts to eat into returns before the promised AI economics fully arrive.

The third leak is demand quality. Circular financing can support the build-out for a while, but it cannot replace external customer cashflow forever. If AI labs continue to sign huge compute commitments while relying heavily on strategic capital and future funding rounds, the market will eventually ask whether the contracts are supported by real end-user economics or by another turn of the financing wheel.

This is already the concern around parts of the datacenter market. Reuters warned that shaky datacenter tenants could choke off the AI boom, especially where developers build for neoclouds and other less financially robust customers. The risk is not only whether the building is useful. It is whether the tenant behind the long-term lease is strong enough for lenders to finance the project on attractive terms.

What we think happens first

The more likely near-term scenario is a leak, not a pop.

Capital remains available, but more selectively. The strongest companies continue to build, while weaker projects are delayed. Investors begin to separate companies that fund AI from cashflow, companies that fund it from debt, and companies that depend on someone else’s funding to pay their own commitments.

That would not kill AI. It would probably make the cycle healthier. A leaking bubble can force discipline without destroying the infrastructure. It can push hyperscalers to disclose returns more clearly, force AI labs to prove unit economics, make lenders price tenant risk properly, and move capital away from speculative capacity toward projects with real utilization.

The real risk is that the leak is ignored until the wall is too thin. If investors continue treating all AI backlog as equal, all datacenter capacity as durable, and all compute demand as externally funded, the system may keep expanding into weaker material. Then a small credit shock can do more damage than expected because the market suddenly realizes that parts of the wall were thinner than they looked.

Our current read is not “AI is about to pop.” The better conclusion is that the bubble is already being stress tested at the edges. Private credit is slowing. Corporate bond markets are absorbing more AI-related debt. Datacenter financing is becoming more dependent on tenant quality. Big Tech remains strong, but the wider ecosystem is more exposed to funding conditions than it was when the story was mostly about operating cashflow and chip shortages.

The question is therefore not simply whether the AI bubble pops. It is how much pressure it can lose before investors start caring. If outside cashflows keep growing, the leak can be managed. If financing slows faster than profitable demand arrives, the bubble does not need to explode. It can deflate first, and only pop later if the market discovers that the contracts, tenants and cashflows underneath the build-out were weaker than expected.

Conclusion: Where We Want to Stand

TVF cannot pop the AI bubble.

But we can decide where we do and do not want to stand if the wall starts leaking.

Our conclusion is that the AI bubble is real, but not equally fragile everywhere. The core still looks strong. Microsoft, Alphabet, Amazon, Meta and Nvidia have real businesses, real cashflows, real customers and strategic reasons to keep investing. They are not the weakest part of the bubble.

The weaker parts sit further out in the financing chain. That means names like CoreWeave, where the investment case is more directly tied to external financing, customer contracts and continued demand for AI compute. It means Oracle, where the AI story has become increasingly linked to huge cloud commitments and the quality of OpenAI-related backlog. It means private AI labs like OpenAI and Anthropic, where the technology may be important, but the compute commitments still require enormous amounts of capital. It also means datacenter projects financed through structures like Meta’s Blue Owl deal, which may be smart, but show how much external capital is now being pulled into the AI build-out.

These are not automatically bad investments or broken businesses. They are the places where the wall is easiest to test.

If financing becomes more selective, if private credit slows, if AI labs need fresh capital to pay for compute, or if large cloud commitments are renegotiated, these weaker layers are likely to show stress first. That makes them important even if we do not want to own them. They are the early-warning indicators for the whole AI cycle.

For TVF, that changes the required return.

We are not against AI exposure. But we would rather own companies with strong financing, real free cashflow, durable demand, pricing power and enough margin of safety to survive a leaking bubble. That makes the strongest hyperscalers, selected infrastructure suppliers and AI-enabled software/data businesses more interesting than highly leveraged neoclouds or AI labs that still depend on the next funding round.

The key is price. A structurally strong AI company can still be a poor investment if the valuation already prices in perfect execution. But structurally, companies with internal funding capacity, mature customers and durable cashflow sit on a much stronger part of the wall than companies whose growth depends on debt, short-lived compute assets, concentrated customers or circular financing.

So our view is sharp, but not blindly bearish.

AI is real. The bubble is also real. The core still looks strong, but the edges are leaking. Financing is no longer something investors can take for granted in a world with higher cost of debt, macro risk and stricter return requirements.

We would avoid the companies that need the bubble to stay inflated. We would monitor them as the first dominoes. And if we invest in AI, we want to be paid for the risk: a higher expected return, a larger margin of safety and clear evidence that the business can turn AI demand into durable free cashflow.

The AI bubble does not need to pop tomorrow to become dangerous. It only needs the weakest parts of the wall to start leaking faster than external cashflows can refill them.

If macro-economics is your thing, check out our other newsletters and subscribe. We recommend:

Author: Jeffrey Kieboom

The Valuation Framework (TVF) turns market and sector news into clear economic models and links those themes to company notes that translate insights into valuation.

This publication is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. It does not take into account your personal financial situation, objectives, or risk tolerance. Investing involves risk, including the risk of loss. Any scenarios, estimates, and forward-looking statements reflect judgment at the time of writing and may change without notice; outcomes may differ materially. The analysis is based on publicly available sources believed to be reliable, but accuracy, completeness, and timeliness are not guaranteed. References to companies, commodities, and markets are illustrative and not endorsements. I may hold positions in securities mentioned, and those positions may change at any time. Nothing in this publication is intended to encourage or facilitate the circumvention of sanctions or other applicable laws and regulations.

Note: I wrote this piece and conducted the research myself. AI was used for feedback/editing support and to generate some of the images.