Ericsson: The Hidden Infrastructure Behind 5G

An investment analysis of Ericsson’s cash flow, moat, India strategy, and whether this overlooked telecom supplier is worth more than the market thinks.

Ericsson is a company almost everyone uses, but almost no one sees.

You do not buy an Ericsson phone. You do not wear its logo. You do not open an Ericsson app. Yet a large part of the digital world runs through infrastructure that this Swedish company helps build: mobile networks, antennas, base stations, 5G software and the technical standards behind modern connectivity.

That makes Ericsson interesting in a world where infrastructure is becoming geopolitical again. Countries want to become less dependent on China, operators are looking for ways to finally monetize 5G more effectively, and digital networks are increasingly seen as strategic assets rather than ordinary telecom equipment.

In this deep dive, we therefore examine the central question:

Is Ericsson a boring telecom supplier in a flat market, or an underestimated geopolitical infrastructure play with attractive cash flow?

Dutch newsletter

Disclaimer

Do you appreciate our publication? Then you help us enormously with a like, comment, share and/or restack.

Chapter 1: History

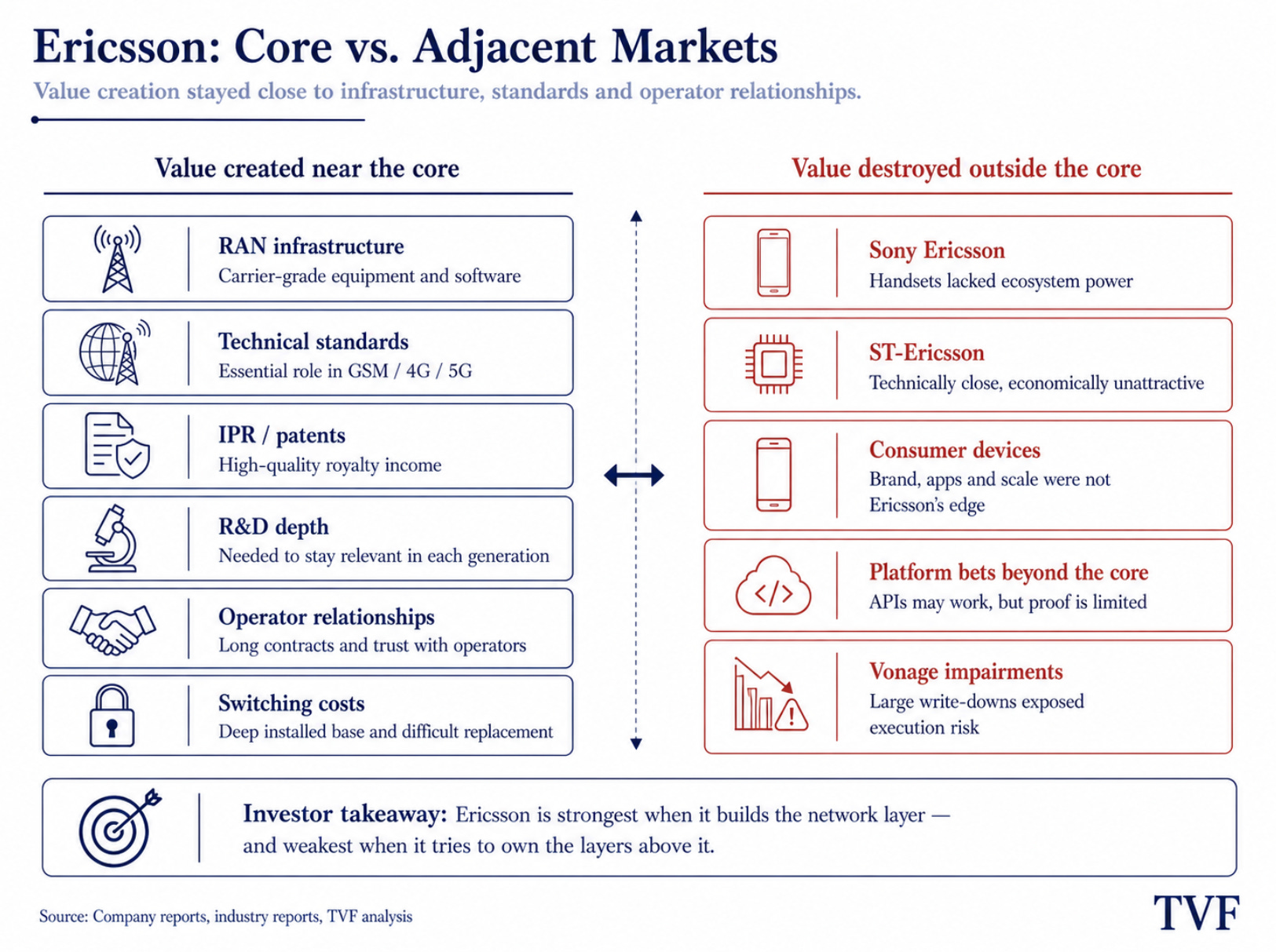

Ericsson is not a company that became large by trying to be everywhere at once. It became large by repeatedly learning where it should not compete.

That is the most important lesson from almost 150 years of corporate history. Ericsson created value when it stayed close to its core: telecom infrastructure, technical standards, R&D, operator relationships and long network cycles. Whenever the company moved too far into consumer products, modems or software ecosystems outside its natural zone of power, capital destruction usually followed.

That history is relevant again today. Ericsson’s core remains strong: radio equipment, antennas, base stations and software for mobile networks. This layer is often called RAN: Radio Access Network, the part of the network that connects your phone to the cell tower.

But the strategic dream now lies with Vonage and network APIs. Through these, Ericsson is trying to make telecom infrastructure programmable: developers would gain software-based access to network functions such as fraud prevention, location verification or guaranteed video quality.

That could become valuable. But Ericsson’s history also says something else: in adjacent markets, the burden of proof should be high.

From workshop to infrastructure company

Ericsson began in 1876 as a small repair workshop in Stockholm. Lars Magnus Ericsson worked from a space of around 13 square meters and initially repaired telegraph equipment and telephones. He did not invent the telephone, but he improved existing designs. He was able to do so because Alexander Graham Bell had not protected his telephone patents in Sweden. Ericsson could analyze Bell’s designs, adapt them and produce them more cheaply.

That early DNA matters: Ericsson did not win through glamour or brand value, but through engineering at a lower total cost. That is still the commercial promise today. Operators do not buy Ericsson because the logo is attractive, but because the network needs to function for years under extreme load.

That became visible early on in the lifespan of its infrastructure. In 1923, Ericsson launched the 500-switch, a mechanical switching system for 500 lines. One 500-switch in Stockholm remained operational for 62 years and was only taken out of service in 1985.

That data point says a lot about the sector. Telecom equipment is not a product with a short replacement cycle. Once a supplier is deeply embedded in a network, switching costs become enormous. An operator is not simply replacing a box; it is touching the core of a communication system on which consumers, companies, emergency services and governments rely.

At the same time, this early international expansion also showed that telecom is never fully neutral. The Russian market once accounted for almost half of Ericsson’s revenue, but was nationalized after the October Revolution. That pattern is still recognizable today: in the West, Ericsson benefits from restrictions on Huawei and ZTE, while geopolitics limits its access to China.

AXE and the birth of platform control

The real strategic breakthrough came in 1976 with AXE, the digital switching platform that Ericsson developed together with the Swedish PTT.

A switching platform routes calls and data traffic through a network. AXE was important because it separated hardware and software in a modular way. New functions could be added without replacing the entire system.

For operators, this lowered upgrade costs and migration risk. For Ericsson, it meant something even more important: platform control.

That logic is still visible today. Hardware is often the entry point, but the value lies in software, upgrades, standards and long-term network control. The later Ericsson Radio System, which from 2015 onward could be upgraded from 4G to 5G through software, follows the same logic.

Ericsson therefore does not simply sell equipment. It tries to control a technology layer that can be expanded, maintained and monetized for years.

The patent machine

In the 1980s and 1990s, telecom shifted from national systems to global mobile standards. GSM harmonized mobile communication. 3G made data more important. 4G/LTE made mobile internet scalable.

In those phases, Ericsson was not just a supplier, but also a co-architect of the technical standards. That is where today’s IPR moat emerged: patent income from technology that other parties need in order to make phones and networks work according to the standard.

Ericsson now has more than 60,000 granted patents and generates approximately SEK 13 to 14 billion in annual IPR revenue.

That is not ordinary revenue. It is a high-quality royalty layer, because direct costs are limited. For investors, this is one of the most valuable parts of Ericsson: an earnings floor that is less dependent on the telecom operator investment cycle.

Ericsson was barely visible to consumers, but it was deeply embedded in the infrastructure on which the digital economy began to run.

The R&D red line

The dot-com crisis of 2001 was an existential test. Operators abruptly pulled back their investments, and Ericsson had to reduce its workforce from around 107,000 to 85,000 employees in a single year.

Yet the most important lesson was not just cost reduction. The real lesson was that Ericsson had to protect its R&D machine.

In telecom infrastructure, R&D is not a luxury. It is the entry ticket to remain relevant in the next standard. Whoever stops investing loses the next generation of technology. Whoever loses that also loses patent income, operator trust and future installed base.

With annual R&D spending of around USD 5 billion, roughly 20% of revenue, Ericsson buys its right to remain in the game. That discipline explains why Ericsson survived while sector peers disappeared, merged or were absorbed. What remains in the West is effectively a Nordic duopoly: Ericsson and Nokia.

The warning: adjacent markets

Sony Ericsson seemed logical. Ericsson understood mobile networks. Sony understood consumer products. But after the iPhone, smartphones were no longer mainly about radio technology. They were about software ecosystems, app stores, design, brand, scale and consumer behavior. Those were not Ericsson’s natural advantages. In 2012, Ericsson sold its stake to Sony for €1.05 billion.

ST-Ericsson was a similar lesson. Modems and mobile platforms were technically close to Ericsson’s core, but economically the market was dominated by players such as Qualcomm, with enormous scale and deep integration into smartphone platforms.

The lesson is simple: Ericsson is strong when it helps determine how mobile networks should technically function. It is much weaker when it competes in markets where others control the standard, scale and margins.

Vonage: the same question again

Ericsson acquired Vonage in 2022 for USD 6.2 billion. The idea is that developers gain access to mobile network functions through APIs. Think of fraud prevention, location verification or guaranteed network quality.

Technologically, that makes sense. Operators have been looking for years for ways to better monetize 5G. But historically, this is exactly the kind of adjacent market where Ericsson has struggled before.

The financial reset was substantial. In 2023 and 2024, Ericsson recognized a total of approximately SEK 43.3 billion in impairments on Vonage-related assets. That does not mean the API thesis is dead, but it does mean the original expectations were too high.

Ericsson’s core is proven. The API thesis is not.

The investor lesson

Ericsson’s history is ultimately a capital allocation story.

Ericsson created value when it stayed close to standards, infrastructure and operator relationships. That is where it built scale, switching costs, R&D depth and patent income.

It destroyed value when it tried to win markets where consumer behavior, platform power or component scale mattered more than carrier-grade engineering.

That is the key lesson for today. Ericsson does not need to prove that it can build telecom infrastructure. It has been doing that for almost 150 years. It needs to prove that, through Vonage and network APIs, it can build a software ecosystem without once again drifting too far from the layer where it truly has power.

Chapter 2: The business model

At first glance, Ericsson looks like a hardware company. It sells radios, antennas, basebands and network equipment to telecom operators. But economically, it is better understood as a layered infrastructure machine.

Hardware builds the installed base. Software and services monetize it. IPR forms the earnings floor. Enterprise is the unproven option outside the traditional telecom cycle.

In 2025, Ericsson generated SEK 236.7 billion in revenue, compared with SEK 247.9 billion in 2024 and SEK 263.4 billion in 2023. The topline therefore does not grow like a software compounder. But with Ericsson, the question is not only how much revenue is booked. It is mainly about the quality of that revenue.

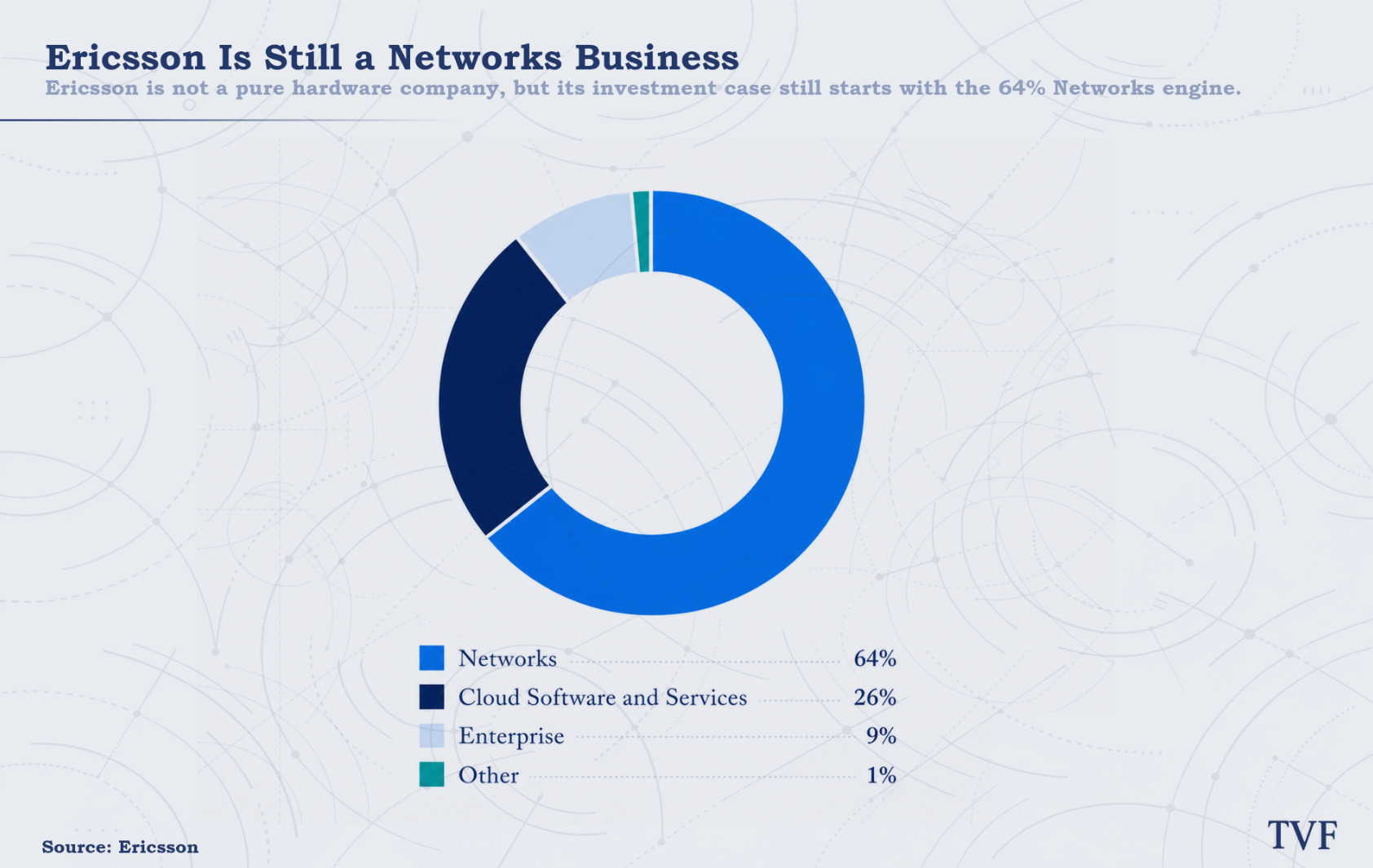

The mix shows this clearly. In 2025, revenue consisted of approximately SEK 88.6 billion in hardware, SEK 55.1 billion in software and SEK 92.9 billion in services. On top of that came SEK 14.5 billion in IPR/licensing revenue.

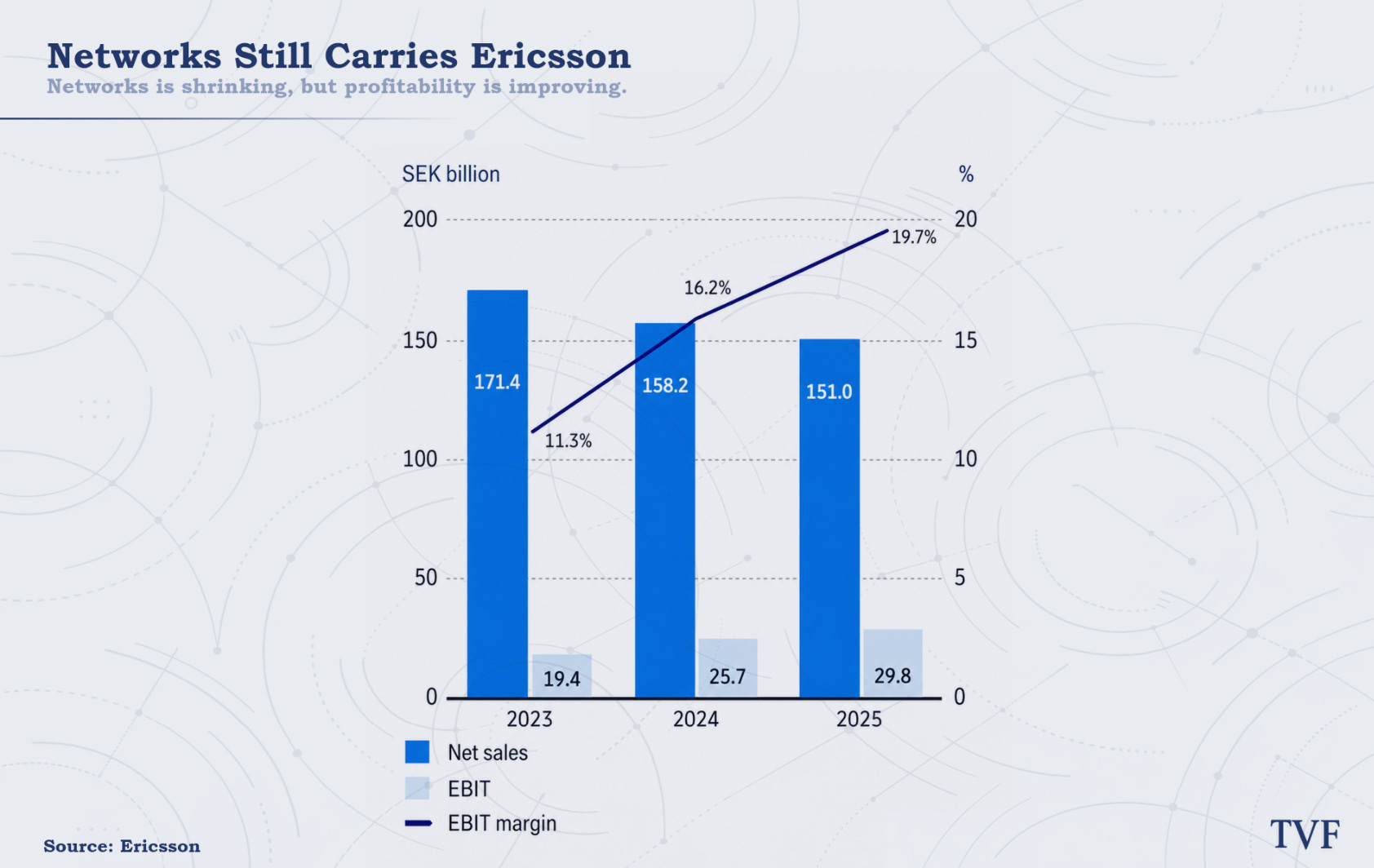

Networks: the core

Networks is by far the largest segment. In 2025, it generated SEK 151.0 billion in revenue, approximately 64% of the group. This is the division that supplies the physical and software layer of mobile networks: radios, antennas, basebands, RAN compute, transport solutions and software.

The economic logic is simple: hardware opens the door, but the higher margin comes later through software, capacity licenses, spectrum activation and optimization. That is why the installed base matters more than the initial sale.

An important advantage within Networks is Ericsson Silicon: proprietary chips for radios and basebands. That sounds technical, but the investor point is simple. Lighter and more energy-efficient equipment can be cheaper for operators over its lifetime, even if the initial price is higher. Ericsson therefore derives pricing power not from brand value, but from lower operating costs for the customer.

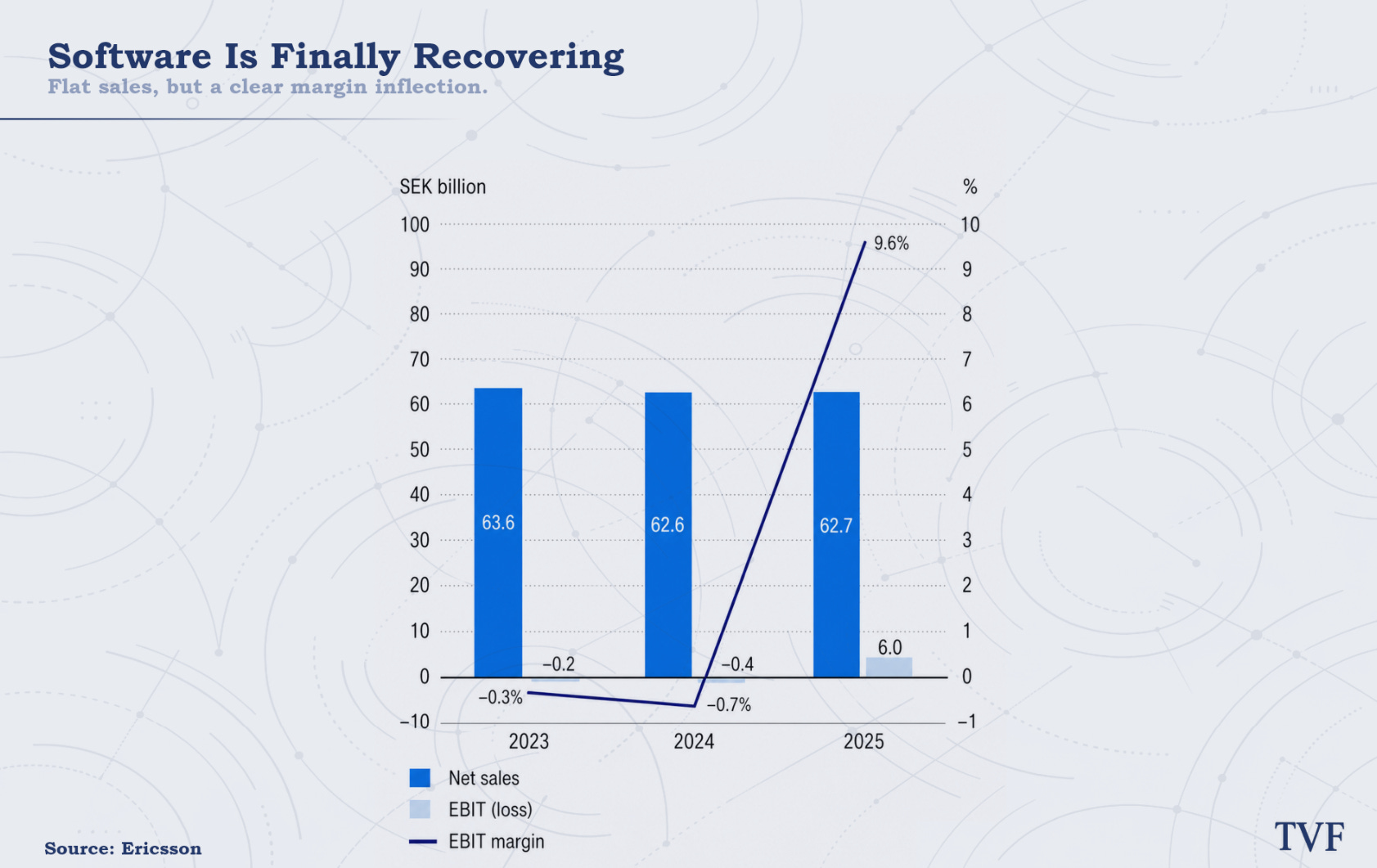

Cloud Software & Services: recovery, not yet a growth engine

Cloud Software & Services provides the software layer of the network: 5G Core, OSS/BSS, charging, policy management, orchestration and managed network operations.

In 2025, this segment generated SEK 62.7 billion in revenue, approximately 26% of the group. Historically, this was a difficult business due to loss-making legacy contracts and too much customization. The current strategy is therefore standardization: more cloud-native software, more automation and less project-specific complexity.

That is starting to show. Gross margin improved from 34.7% in 2023 to 41.7% in 2025. But revenue is not growing rapidly yet. For now, CSS is therefore primarily a margin recovery story, not a proven software growth engine.

The real accelerator should come from 5G Standalone. Only with a modern 5G core can operators offer functions such as network slicing, ultra-low latency and performance-based services. By the end of 2025, however, only around 24% of operators with 5G services had actually launched 5G Standalone.

The software opportunity is therefore logical, but not yet fully visible in the numbers.

IPR: the best revenue

The highest-quality revenue within Ericsson comes from IPR: income from patents.

Ericsson owns more than 60,000 granted patents and has a strong position in standard-essential patents for mobile networks. In 2025, IPR generated SEK 14.5 billion in revenue. In Q1 2026, the run-rate was around SEK 13 billion.

This is the cleanest economic layer of the company. There are hardly any direct costs attached to it, which means the margin is much higher than in hardware or services. IPR therefore forms an earnings floor that is less dependent on the volatility of operator capex.

There is an important nuance, however. IPR is not reported as a separate segment. Around 82% of this revenue falls within Networks and around 18% within Cloud Software & Services. As a result, segment margins look stronger than they would without this royalty layer.

Services: recurring, but not automatically high-quality

Services generated SEK 92.9 billion in revenue in 2025. This includes support, lifecycle management, deployment, managed services and network operations.

These revenues increase customer stickiness. An operator that uses Ericsson not only for hardware, but also for support and network management, is less likely to switch supplier.

But not all recurring revenue is equally attractive. Rollout services can pressure margins. Managed services can be predictable, but remain labor-intensive. The upside therefore lies mainly in automation and AI-driven network management.

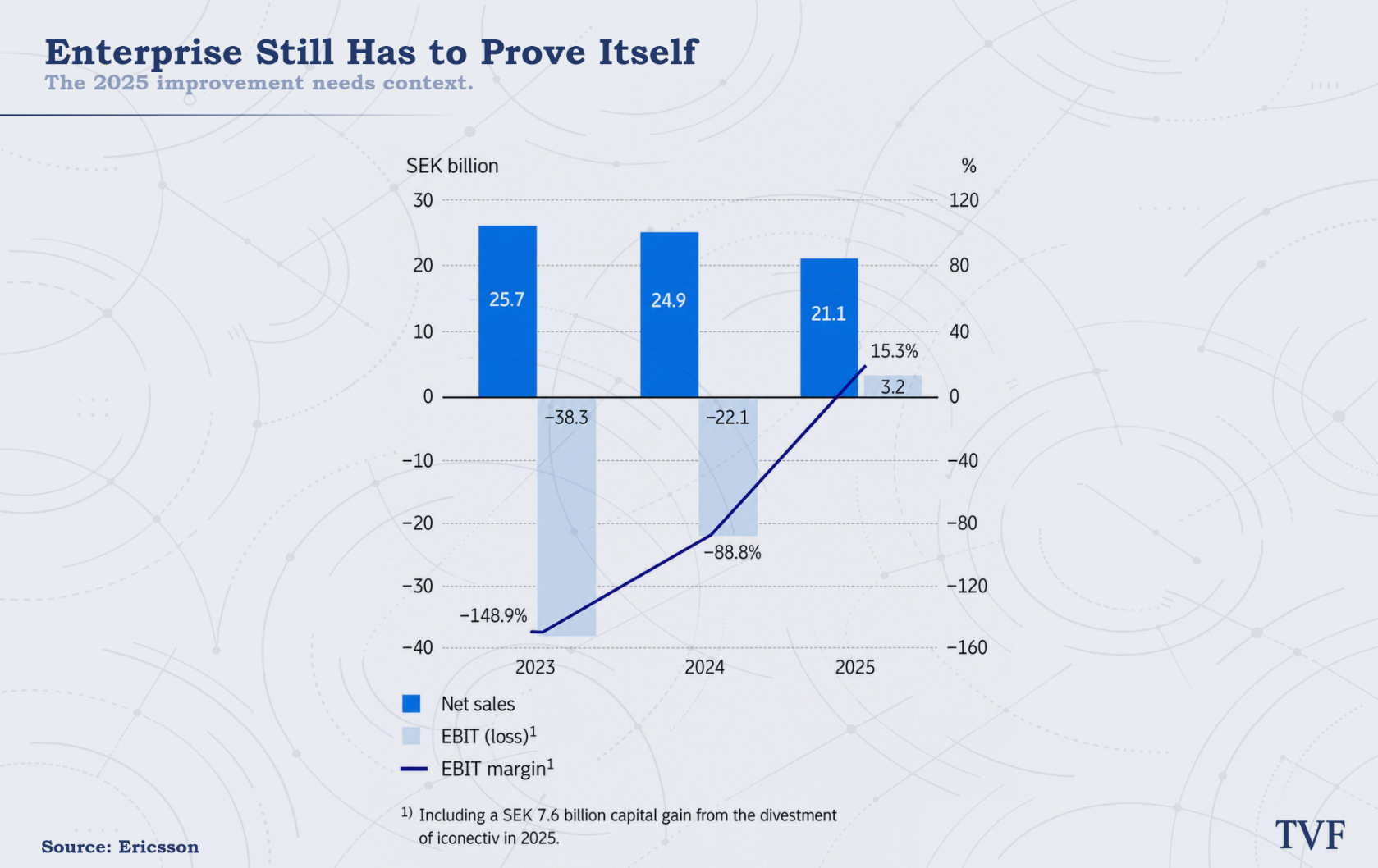

Enterprise: option value, not proof

Enterprise is Ericsson’s attempt to become less dependent on telecom operator capex. In 2025, Enterprise generated SEK 21.1 billion in revenue, approximately 9% of the group.

The tangible part is Cradlepoint: Wireless WAN, private networks and enterprise connectivity. That is real, but not yet a major growth engine.

The more ambitious part is Vonage, Aduna and network APIs. Ericsson wants to make network functions programmable for developers. If this works, Ericsson could partly shift from being a cyclical infrastructure vendor to becoming a platform company.

But for now, this is mainly option value. Ericsson had to take approximately SEK 43.3 billion in impairments on Vonage-related assets in 2023 and 2024. That means the original expectations were far too high.

Chapter 3: The infrastructure cycle

Ericsson does not simply grow along with data traffic.

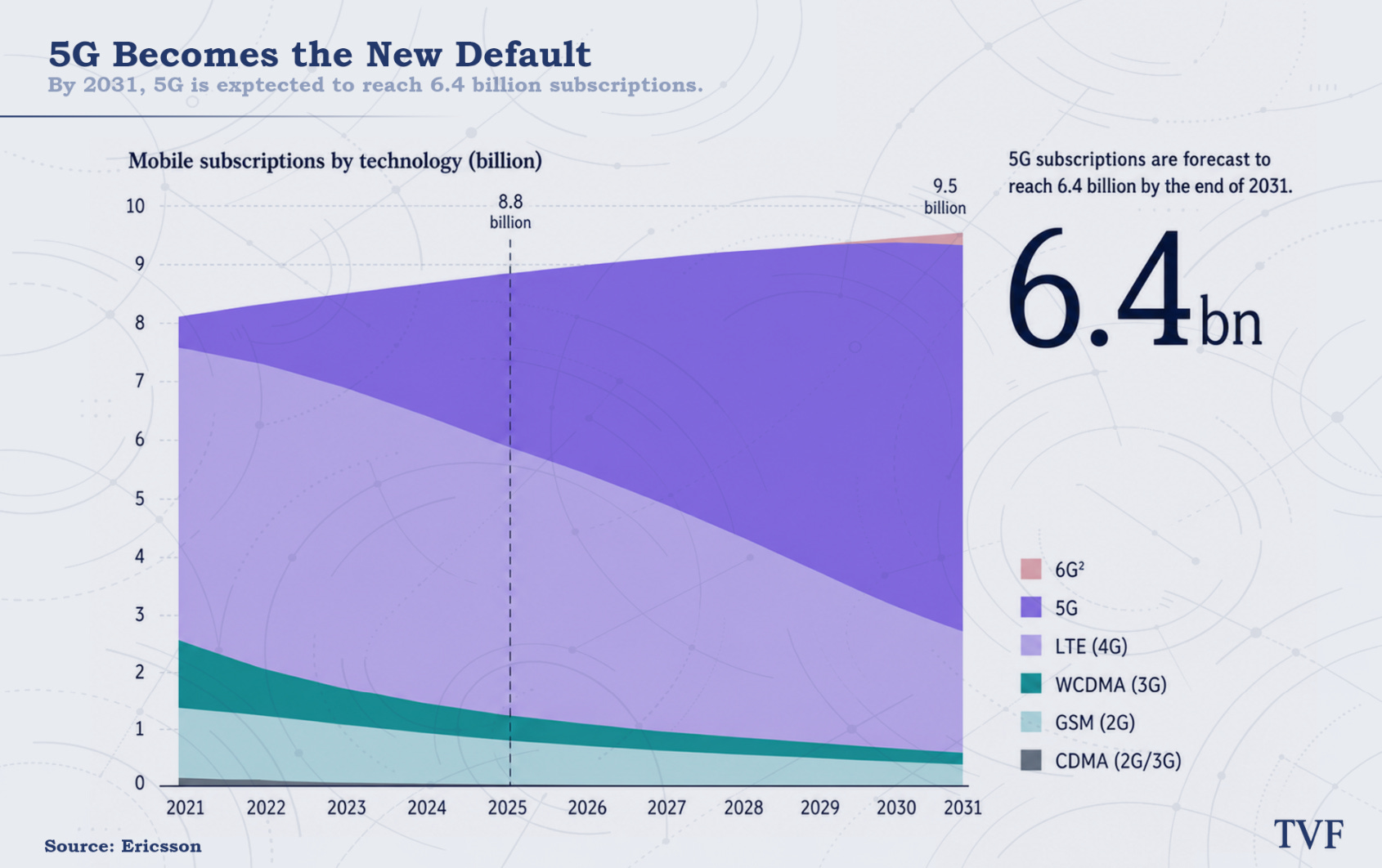

That is the most important lesson from the telecom infrastructure cycle. Every ten years, a new mobile generation arrives: 2G, 3G, 4G, 5G and soon 6G. On paper, that looks like a perfect growth machine: more data, more devices, more connections, and therefore more demand for network equipment.

In reality, it is more difficult. Data traffic grows rapidly, but operator revenue does not automatically grow with it. Consumers use more video, cloud, messaging and AI applications, but they do not always pay more for their subscription.

That means Ericsson is not a pure play on data growth. It is mainly a play on operator capex.

And operators invest only when they see a return.

Coverage first, capacity later

Each mobile generation broadly has two phases.

The first phase is coverage. Operators build coverage as quickly as possible. For this, they buy radios, antennas, basebands and installation capacity. For Ericsson, this generates a lot of revenue, but not always the best margin. Coverage projects are physical, logistically heavy and competitive.

The second phase is capacity. Once coverage is in place and data traffic keeps growing, operators need to densify and upgrade their existing networks. Demand then shifts toward software, Massive MIMO, spectrum activation, 5G Standalone and network optimization.

That phase is more attractive for Ericsson. A software upgrade has much lower marginal costs than installing new hardware. The investor case is therefore not about whether the world uses more data. It is about whether operators can earn enough money to finance the capacity phase.

The RAN market barely grows

The hard paradox: the market for Radio Access Network equipment barely grows, despite explosive growth in data traffic.

For 2025–2030, sector analysts expect only around 1% annual growth in the RAN market. That means Ericsson operates in an oligopoly, but not in a structurally growing market.

The sector can temporarily peak when a new generation is rolled out. We saw that with 5G in the US and India. But then normalization follows. North America slowed sharply after operators reached their initial 5G coverage targets. India temporarily compensated for that with a massive rollout, but there too a decline followed afterward.

Ericsson’s revenue therefore does not directly follow the growth of mobile data traffic. Ericsson’s revenue follows the investment decisions of operators.

Operator economics are the bottleneck

Ericsson’s real customer is not the smartphone user, but the telecom operator.

That changes everything. Ericsson may be technologically ready for 5G Standalone, network slicing and AI-native networks, but if operators want to protect their balance sheets, the order comes later.

Many operators are in a difficult position. They need to keep investing in spectrum, mobile networks, fiber, cybersecurity and maintenance, while revenue is often under pressure from regulation and competition.

Spectrum costs make this even heavier. In eight representative countries, operators spent approximately USD 32 billion on 5G spectrum licenses between 2018 and 2024. That money goes to governments, not to Ericsson. It does create the need to roll out networks, but it first burdens the balance sheet.

That is why 5G was commercially disappointing for many operators. The first rollout delivered faster networks, but not automatically higher ARPU. Many consumers did not want to pay extra for “faster internet” if their existing connection was already good enough.

The second phase of 5G therefore needs to be different. Operators need to earn money from concrete use cases, not from the 5G label.

Regional differences

Regionally, the cycle is uneven.

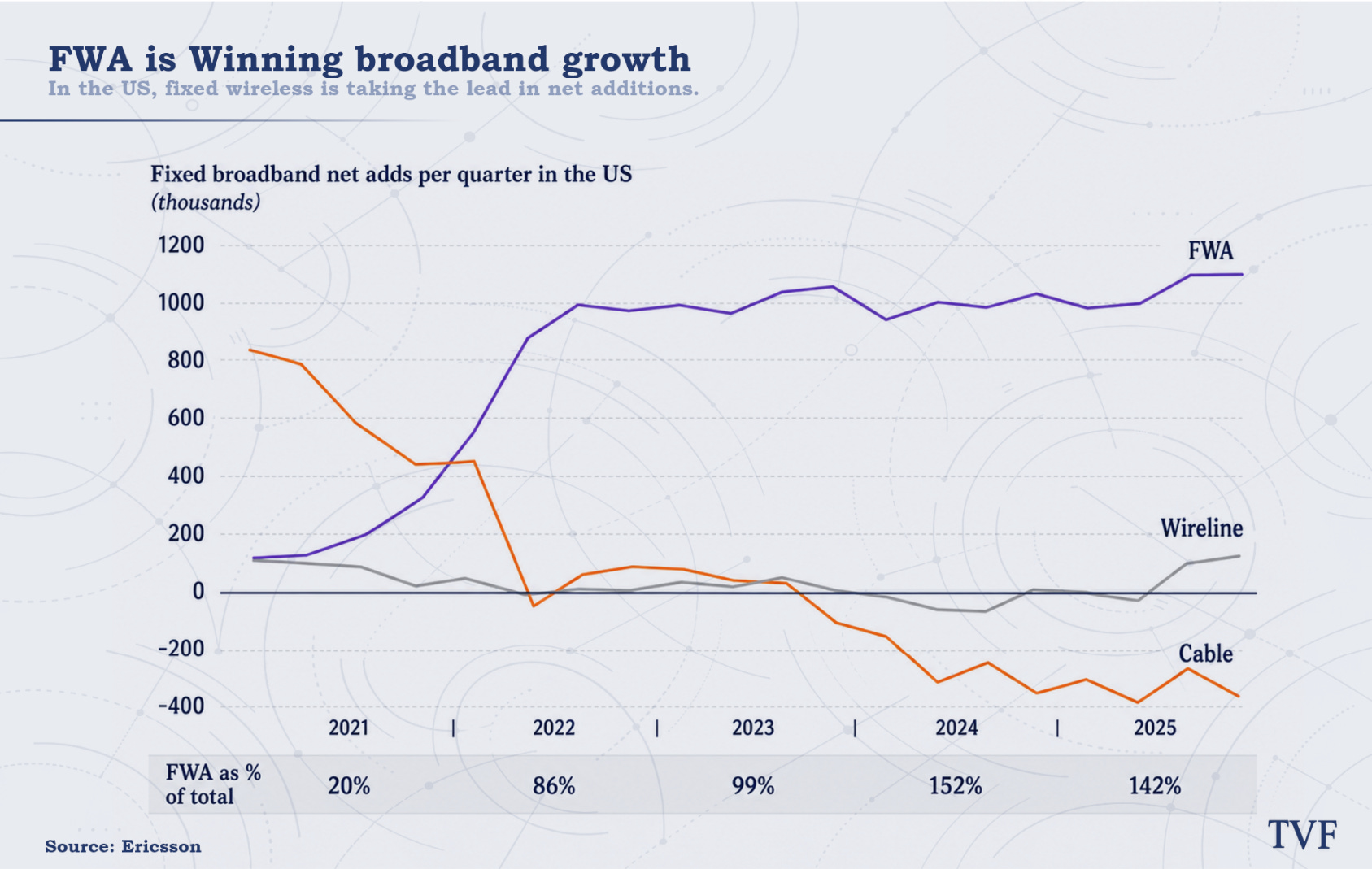

The US remains the most attractive region for Ericsson: high ARPUs, strong bundles and concrete 5G monetization through Fixed Wireless Access. The first coverage phase is largely complete, but the next phase revolves around capacity, FWA, 5G Standalone, software upgrades and the AT&T Open RAN deal. That is less explosive for revenue than a national rollout, but more attractive for margins.

Europe, by contrast, has technical necessity but weak operator economics. Mid-band 5G coverage stood at around 50% at the end of 2024, much lower than in the US and India. Yet capex remains weak because of fragmentation, regulation and low pricing power. Europe therefore has necessity, but necessity is not an order book.

India offset the US slowdown in 2023 with 82% organic growth in Ericsson’s region South East Asia, Oceania and India. By the end of 2024, mid-band coverage was around 95%. But this was primarily coverage revenue: lots of hardware, lots of volume, not necessarily the highest margin. In 2024, revenue therefore fell by approximately 39%.

China is technologically ahead in 5G Standalone, industrial 5G and AI integration, but for Ericsson it is mainly a benchmark, not a growth engine. Huawei and ZTE dominate the market, and Ericsson’s share has fallen to around 4%.

What actually works in 5G monetization?

The first 5G round was commercially disappointing because consumers did not massively pay extra for faster mobile internet. The second round needs to revolve around concrete monetization.

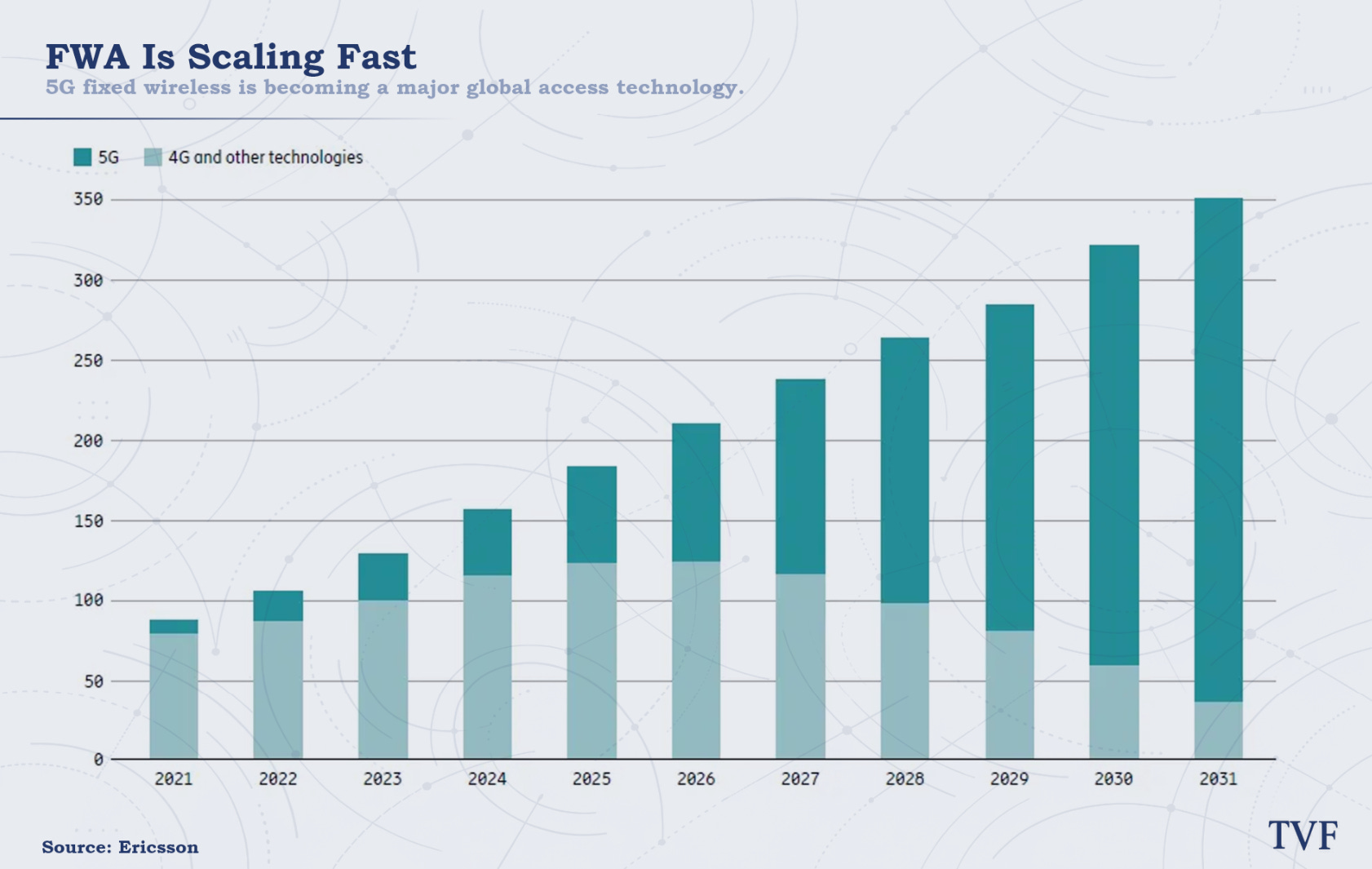

Fixed Wireless Access is the most tangible. Globally, there were already more than 100 million FWA connections, with expectations moving toward 350 million by 2030/2031. For Ericsson, this is interesting because FWA requires a lot of capacity and can therefore stimulate additional radios, software and optimization.

Private networks are strategically interesting, for example for factories, ports, hospitals and logistics, but for now they remain small relative to public mobile networks.

Network slicing can divide one network into virtual layers with different quality levels, for example for emergency services, industry or premium video. But slicing requires 5G Standalone, and adoption remains slow.

Network APIs through Vonage and Aduna can give developers access to network functions such as location verification, fraud prevention or Quality on Demand. Strategically interesting, but financially still unproven.

In short: FWA already works, private networks are small, slicing is waiting for 5G SA, and APIs remain option value.

The AI paradox

AI makes the cycle more complicated.

On the one hand, AI increases demand for network capacity. AI agents, wearables, AR glasses and cloud applications can especially increase uplink demand. More complexity and more data traffic require better networks.

On the other hand, AI helps operators use existing networks more efficiently. AI can reduce energy consumption, predict outages and allocate capacity more intelligently. If operators can push more traffic through the same infrastructure with AI, that may delay physical capex.

For Ericsson, the net effect is probably positive, but not automatically through more hardware. Value may shift toward software, automation, network optimization and AI-native operations.

AI makes networks more important, but also more efficient.

6G: cost today, patent position tomorrow

6G will probably only become commercially relevant around 2030/2031.

Until then, for Ericsson, it is mainly an R&D cost item. But that investment is necessary. Whoever helps shape the standard builds the future patent position. And that patent position later determines royalty income again.

That is why Ericsson cannot simply reduce its annual R&D spending of around USD 5 billion without damaging its future IPR moat.

The core

The telecom cycle has therefore shifted from rollout to monetization.

The old logic was simple: new generation, new hardware, new capex wave. The new logic is harder. Operators invest only if they can better monetize their network or reduce their costs sufficiently.

Ericsson has the technology, installed base and R&D scale to benefit from that second phase. But it cannot control operator economics.

The technology is not the problem. The question is whether customers can earn enough money from it to pay Ericsson again.

Chapter 4: Competition and moat

Ericsson operates in a strange market. Mobile networks are critical infrastructure, but the market for Radio Access Network equipment barely grows. For 2025–2030, analysts expect around 1% annual growth. Ericsson is therefore not a classic growth compounder, but a high-quality survivor in a concentrated market.

The moat is real, but limited. It mainly protects relevance, contract opportunities, installed base and IPR revenue. It does not provide unlimited pricing power, because the customers are large telecom operators: professional buyers who use tenders to push hard on price.

A market almost no one can enter anymore

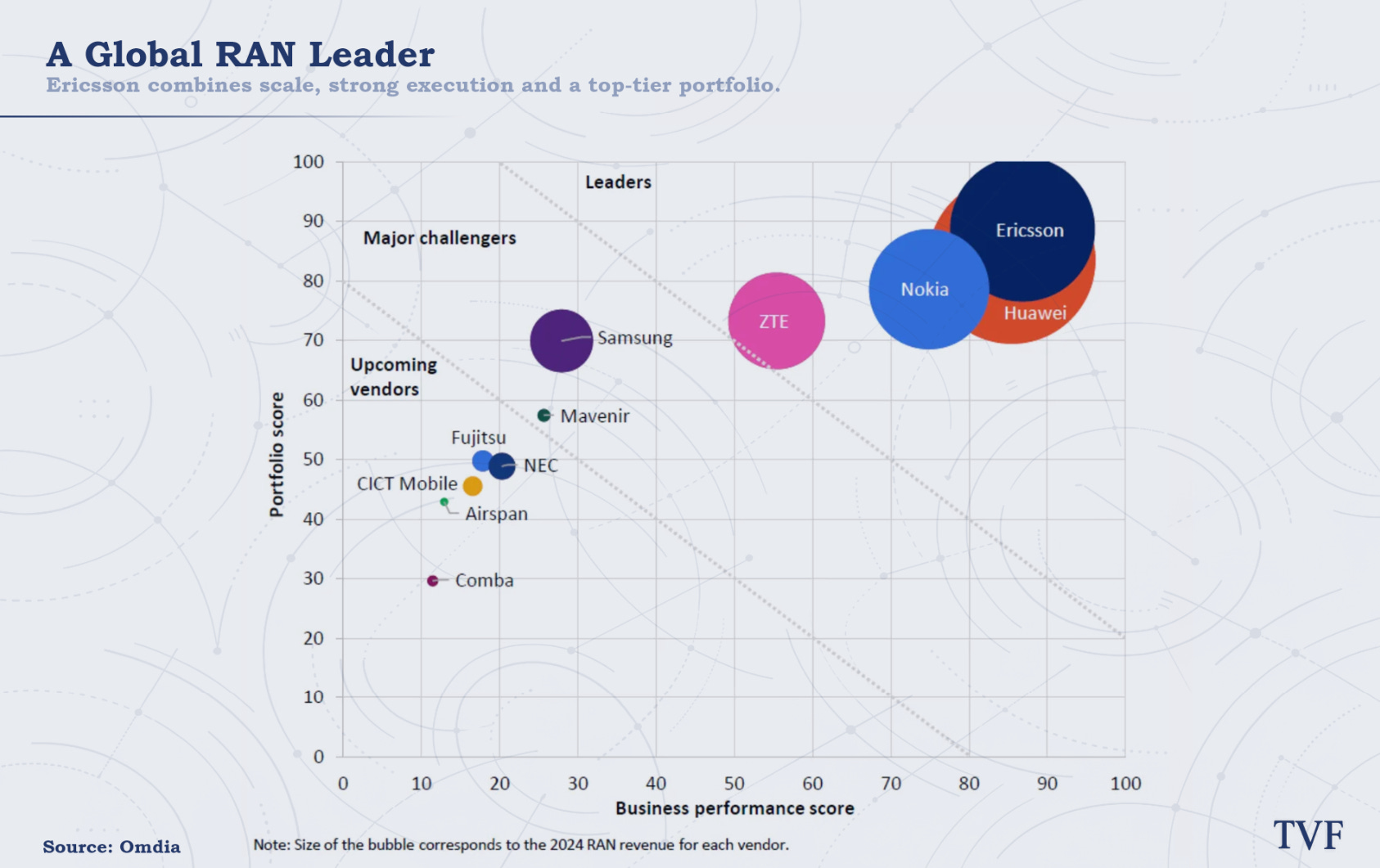

The global RAN market is dominated by five players: Huawei, Ericsson, Nokia, ZTE and Samsung. Together, they control around 93.6% of the market. The top three: Huawei, Ericsson and Nokia, account for approximately 77.4% of revenue.

That concentration does not come from spectacular market growth, but from extreme barriers to entry. A new player would need to invest billions in R&D, build a patent portfolio, support multiple generations of telecom technology, obtain security certifications and provide global support.

That is almost impossible.

Ericsson’s moat is therefore partly the result of industrial exhaustion. Nortel disappeared, Alcatel-Lucent was acquired by Nokia, and Siemens withdrew from mobile infrastructure. What remains in the West is effectively a Nordic duopoly: Ericsson and Nokia.

That is favorable, but not enough for unlimited margins. Operators remain powerful customers.

Ericsson versus Nokia

The most important comparison is Ericsson versus Nokia. Both companies are the main Western alternatives to Huawei, but their strategies differ.

Ericsson is today the purer mobile RAN/IPR player. Nokia is positioned more broadly, with more exposure to fixed networks, IP routing, optical transport and AI/cloud networking after the acquisition of Infinera. That broader strategy may be valuable, but Ericsson currently has the sharper mobile RAN and margin profile.

That is visible in the numbers. Ericsson achieved an adjusted EBITA margin of around 17.1% in 2025. Nokia remained clearly behind in mobile networks, with margins around 9%. Ericsson therefore extracts more profit from the same difficult market.

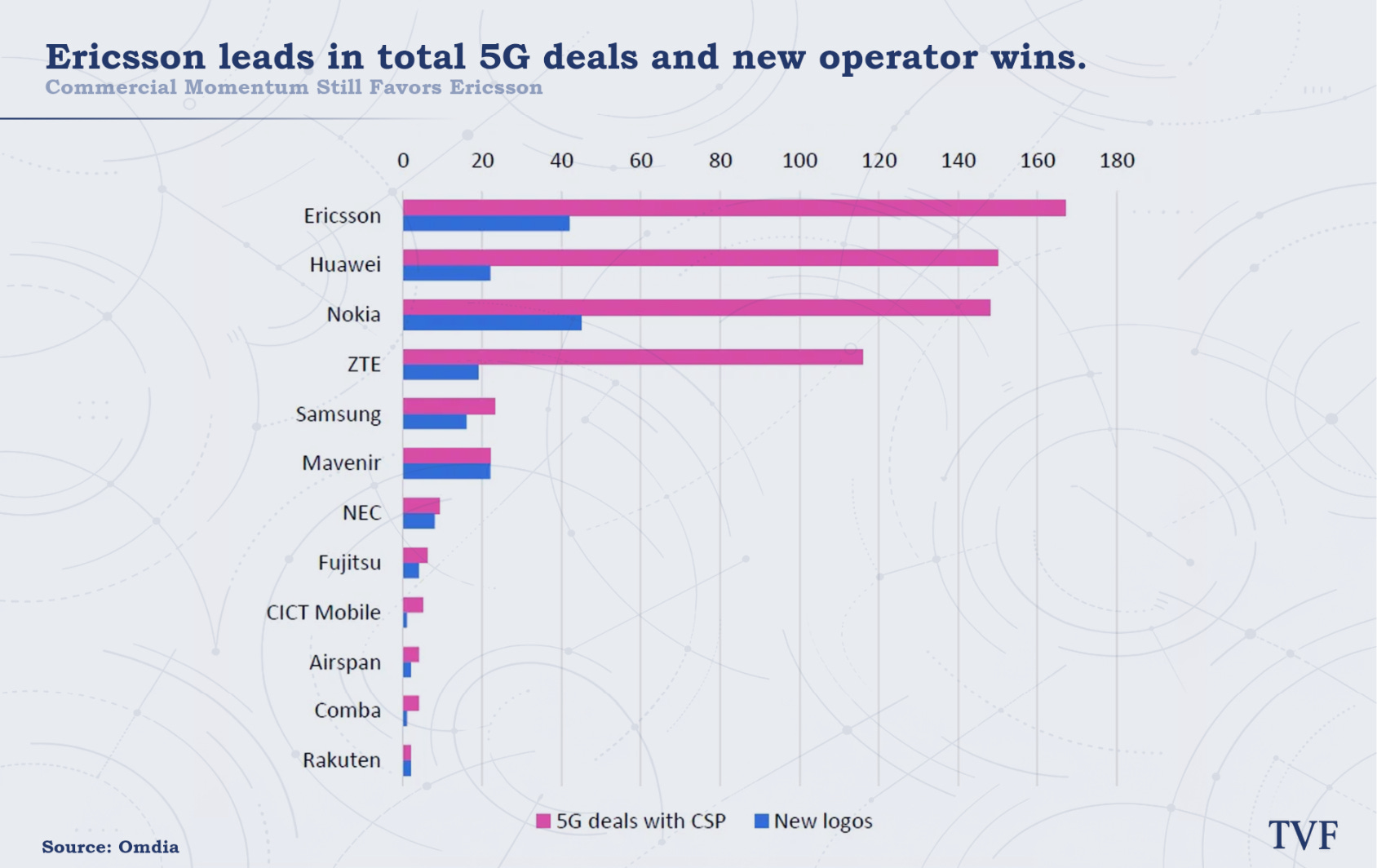

The AT&T deal made that difference even more visible. In 2023, Ericsson won an Open RAN contract with AT&T worth around USD 14 billion over five years. Ericsson is replacing Nokia equipment across a significant part of AT&T’s network, sharply increasing its position in North America, with RAN market share above 50% and, in some estimates, moving toward 70%.

The paradox is interesting: AT&T wanted a more open network, but did not choose a small Open RAN challenger. It chose Ericsson. Operators want openness, but not integration chaos. Ericsson was able to offer that middle ground: open interfaces, but with its own silicon, software, integration strength and global support.

Strategically, AT&T shows that Ericsson can not only defend against Open RAN, but also use it as an offensive weapon against Nokia. Financially, it remains to be seen whether Ericsson sacrificed margin to do so.

Huawei, Samsung and ZTE

Huawei remains the real global benchmark. With approximately 31% market share, it is the largest player in RAN. The company has an enormous home market, large R&D scale, strong vertical integration and a cost base that Western players struggle to match.

In the US, UK, Australia and parts of Europe, Ericsson is helped by restrictions on Huawei and ZTE. But outside those markets, Huawei remains a tough competitor. In Latin America, Africa, the Middle East and parts of Asia, Ericsson has to compete on price, performance, energy consumption, reliability and lifecycle cost.

Ericsson’s moat is therefore geographically uneven. In the West, Ericsson is often the trusted-vendor choice. In markets where Huawei is allowed to compete freely, hardware margins remain vulnerable.

Samsung is technologically relevant, especially in vRAN and Open RAN. It previously won important deals with Verizon and Jio. Still, Samsung is not yet a broad replacement for Ericsson or Nokia. It lacks the deep multi-generation installed base, legacy support and global accountability that large operators need.

ZTE mainly plays the role of price disruptor in China and certain emerging markets. Outside China, it has the same geopolitical handicap as Huawei, but with less global scale.

Switching costs: the hidden moat

Changing supplier in telecom is not a simple IT migration. It means replacing radios at thousands or tens of thousands of sites, integrating with core and software systems, arranging permits, deploying installation teams and preventing network disruption.

Downtime is extremely expensive. It affects consumers, companies, payment systems, emergency services and critical communication. Operators avoid that risk wherever possible.

On top of that, Ericsson often supplies not only radios, but also lifecycle support, OSS/BSS integration, software and managed services. The deeper Ericsson is embedded in operations, the higher the switching costs.

That is the “one throat to choke” logic. Operators want one major party they can hold accountable when the network does not perform. A multi-vendor network sounds attractive, but in practice it can lead to complexity and unclear responsibility.

Switching costs are therefore technical, financial, operational and reputational. That is a real moat.

Open RAN: threat and opportunity

Open RAN was long seen as a threat to Ericsson and Nokia. Open interfaces would make it easier to combine radios, software and basebands from different suppliers. Less lock-in, more competition, lower costs.

In theory, that sounds dangerous. In practice, it is more nuanced. Operators want openness, but not integration chaos. Smaller Open RAN players struggled with scale, performance, financing and global support. Meanwhile, Ericsson and Nokia themselves began supporting Open RAN.

As a result, the incumbents were not swept away. They became “open-ready.”

Ericsson’s strategy is clear: industrialize Open RAN before Open RAN commoditizes Ericsson. The AT&T deal is the best example. AT&T gets a more open architecture, but Ericsson retains a central role through software, integration, silicon, orchestration and accountability.

Open RAN therefore does not destroy Ericsson’s moat. It shifts where that moat needs to sit: less in closed hardware, more in software, integration and system responsibility.

The core

Ericsson therefore has a real moat, but no monopoly pricing power.

The strongest layers are IPR, switching costs, R&D scale, Ericsson Silicon and geopolitical tailwinds in the West. That combination makes Ericsson difficult to replace and keeps the company almost always relevant in critical telecom networks.

But hardware remains sensitive to tenders, operator concentration, Huawei price pressure and Open RAN. Moreover, the RAN moat does not automatically translate to Enterprise, Vonage or network APIs.

Ericsson is therefore not a classic compounder, but a high-quality survivor in an exhausted industry. Value creation does not come from growth alone, but from discipline: R&D, cost control, IPR, software mix and smart capital allocation.

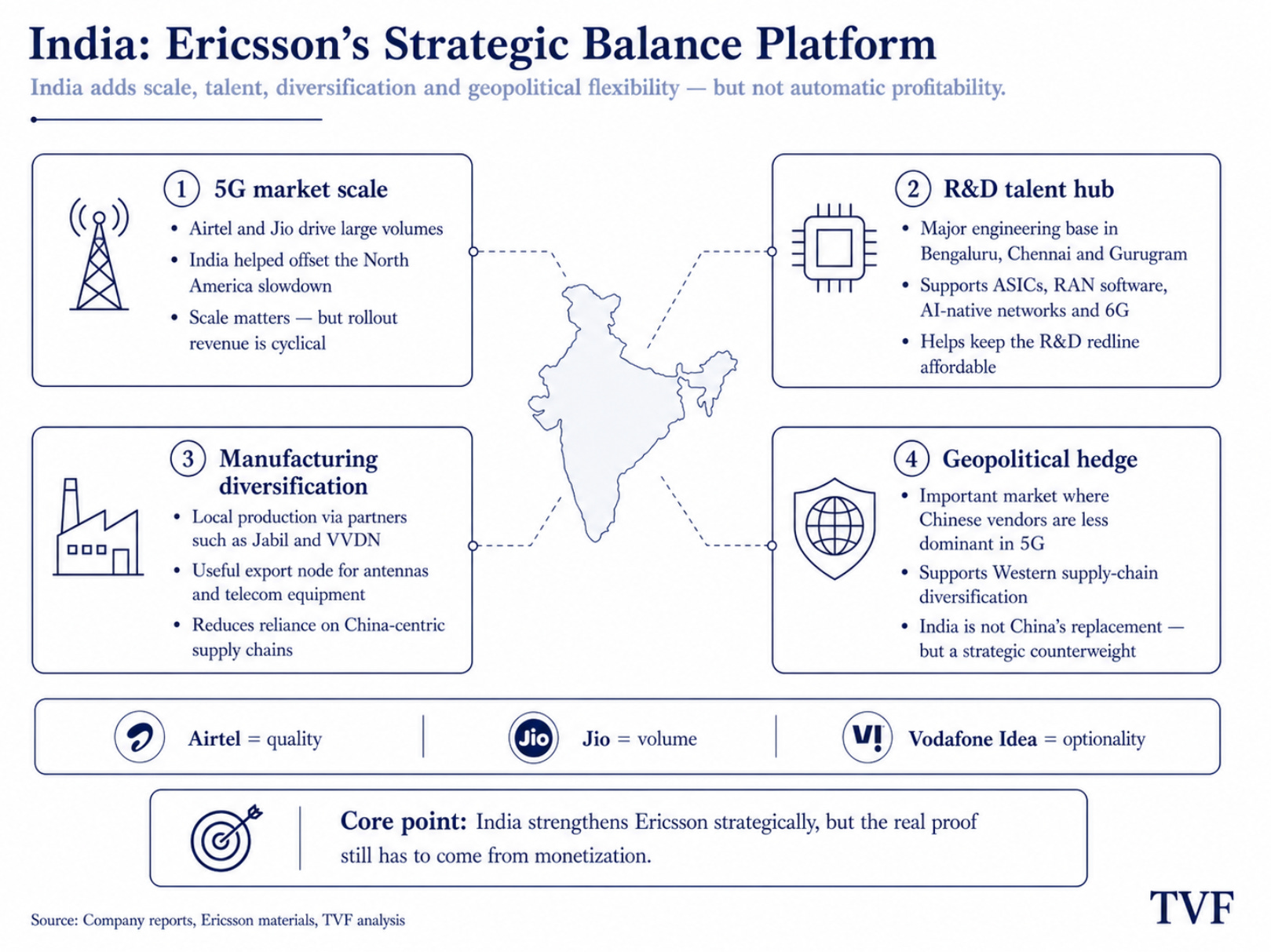

Chapter 5: India

India is no longer a side issue for Ericsson. But it is also not a simple replacement for China or the United States.

The better formulation is this: India is Ericsson’s strategic balancing platform. The country offers scale in 5G, a growing manufacturing footprint, a large R&D talent pool and a geopolitical hedge against China risk. That makes India strategically important, but not automatically high-quality from a margin perspective.

From rollout peak to monetization test

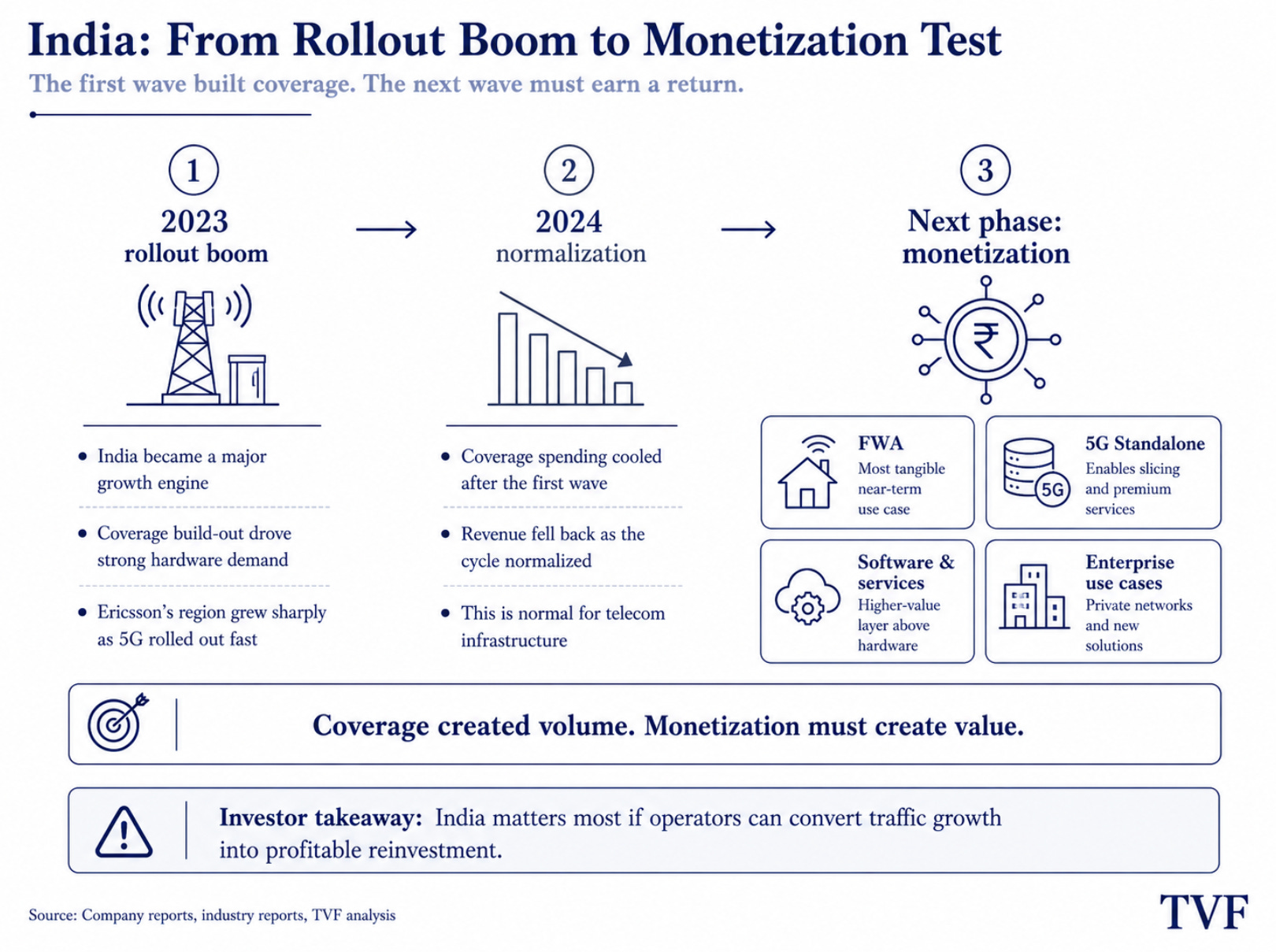

In 2023, India became crucial for Ericsson. While North America slowed after the first 5G coverage wave, India rolled out 5G at an exceptional pace. Ericsson’s region South East Asia, Oceania and India grew organically by 82% that year, largely driven by India.

That was impressive, but also cyclical. The growth mainly came from coverage: lots of radios, antennas, Massive MIMO, RAN Compute and installations. That generates revenue, but not automatically the highest margin. When the first rollout wave normalized, revenue in India fell by approximately 39% in 2024.

That is not proof that India is failing. It is how telecom cycles work. First, operators build coverage. Then they have to prove that they can monetize those networks.

For Ericsson, the India thesis therefore shifts from hardware volume to capacity, software and services. The real question is not whether India is large, but whether operators such as Airtel and Jio can earn enough return from FWA, 5G Standalone and enterprise services to invest again.

Airtel, Jio and Vodafone Idea

Not all Indian revenue has the same quality.

Airtel appears to be the quality anchor for Ericsson. Airtel does not only buy radio equipment, but also uses Ericsson deeper in the software layer, including through 5G Core and Fixed Wireless Access. That is more important than pure hardware sales, because core software can create more switching costs and recurring upgrade revenue.

Jio is mainly the volume engine. The breakthrough with Jio was important for Ericsson’s 2023 growth, especially because Jio had historically been strongly linked to Samsung. But Jio is also a tough buyer with significant scale and its own technological ambitions. That makes the revenue attractive, but not automatically high-quality.

Vodafone Idea is option value with balance sheet risk. Ericsson can benefit if Vi starts investing again, but Vi’s financial position makes that question less predictable.

In short: Airtel is quality, Jio is volume, Vi is optionality.

Scale is valuable, but margins are harder

India could have more than 1 billion 5G subscriptions by 2031. That scale matters. A large installed base creates years of potential revenue from maintenance, software upgrades, capacity expansion and lifecycle services.

But scale is not the same as earnings quality. ARPU is much lower than in the US, while operators need to deliver enormous amounts of data. That means every network upgrade is assessed sharply on cost, capacity and return.

The structural opportunity therefore does not lie in the first mast, but in FWA and 5G Standalone. FWA can deliver broadband without laying fiber everywhere and requires a lot of network capacity. 5G Standalone opens the software layer: slicing, charging, policy, orchestration and enterprise SLAs.

That is where the better revenue lies. Not in the initial rollout, but in everything that can later be sold on top of that installed base.

India as an R&D and production base

The strongest India thesis may not lie in sales, but in R&D.

Ericsson has around 24,000 employees in India. The centers in Bengaluru, Chennai and Gurugram now work on high-end engineering: ASIC development, RAN software, 5G Advanced, AI-native networks and 6G. In 2025, Ericsson expanded its ASIC team in Bengaluru with more than 150 new roles.

That is financially relevant. Ericsson needs to keep investing around USD 5 billion annually in R&D to maintain its technological edge and patent position. If more of that high-quality R&D can take place in India at a lower cost per engineer, that supports long-term margins.

India has also become a production hub. Ericsson has long produced through Jabil in Pune and expanded local production of passive antennas in 2025 through VVDN Technologies in Gurgaon. India is therefore demonstrably an export node for antennas, but not yet a proven full replacement for China’s broader telecom manufacturing ecosystem.

The safe conclusion: India helps Ericsson diversify its supply chain and keep the R&D red line affordable.

The EU-India FTA: protective layer, not growth engine

The EU-India FTA fits well into this story, but should not be overstated.

For Ericsson, source-code protection is especially relevant. Article 9.9 limits the ability to require source-code transfer as a condition for market access. For a company that increasingly derives value from 5G Core, RAN software, AI-native networks and automation, that matters.

Tariff reductions and agreements around digital trade can reduce trade friction, but the exact financial impact depends on implementation, product classifications, local content rules and how much of the cost advantage ultimately stays with Ericsson.

The FTA therefore does not create the India thesis. It reduces friction around a thesis that already exists.

The core

India does not replace China one-for-one, and it does not need to.

For Ericsson, India offers scale, R&D capacity, production diversification and a market where Chinese suppliers are less dominant in 5G. That makes India not a simple growth engine, but a strategic balancing platform.

The EU-India FTA strengthens that position mainly as a protective layer: less friction, better digital trade rules and more certainty around source code. But the financial burden of proof remains the same.

India must evolve from a rollout market into a monetization market. Only then will the strategic value truly become visible in margins and free cash flow.

Chapter 6: Financial health

Ericsson’s financial case is not about strong revenue growth. Revenue declined from SEK 263.4 billion in 2023 to SEK 236.7 billion in 2025. In our base model, revenue falls slightly again by -1.0% to SEK 234.3 billion in 2026, after which only a gradual recovery of +2.0% per year follows toward SEK 258.7 billion in 2031.

That is deliberately cautious. Ericsson operates in a flat RAN market, where growth does not automatically follow from more data traffic. Operators invest only when they see sufficient return. The investment case therefore should not rely on a sudden revenue acceleration, but on margin recovery, IPR, software mix, cost control and buybacks.

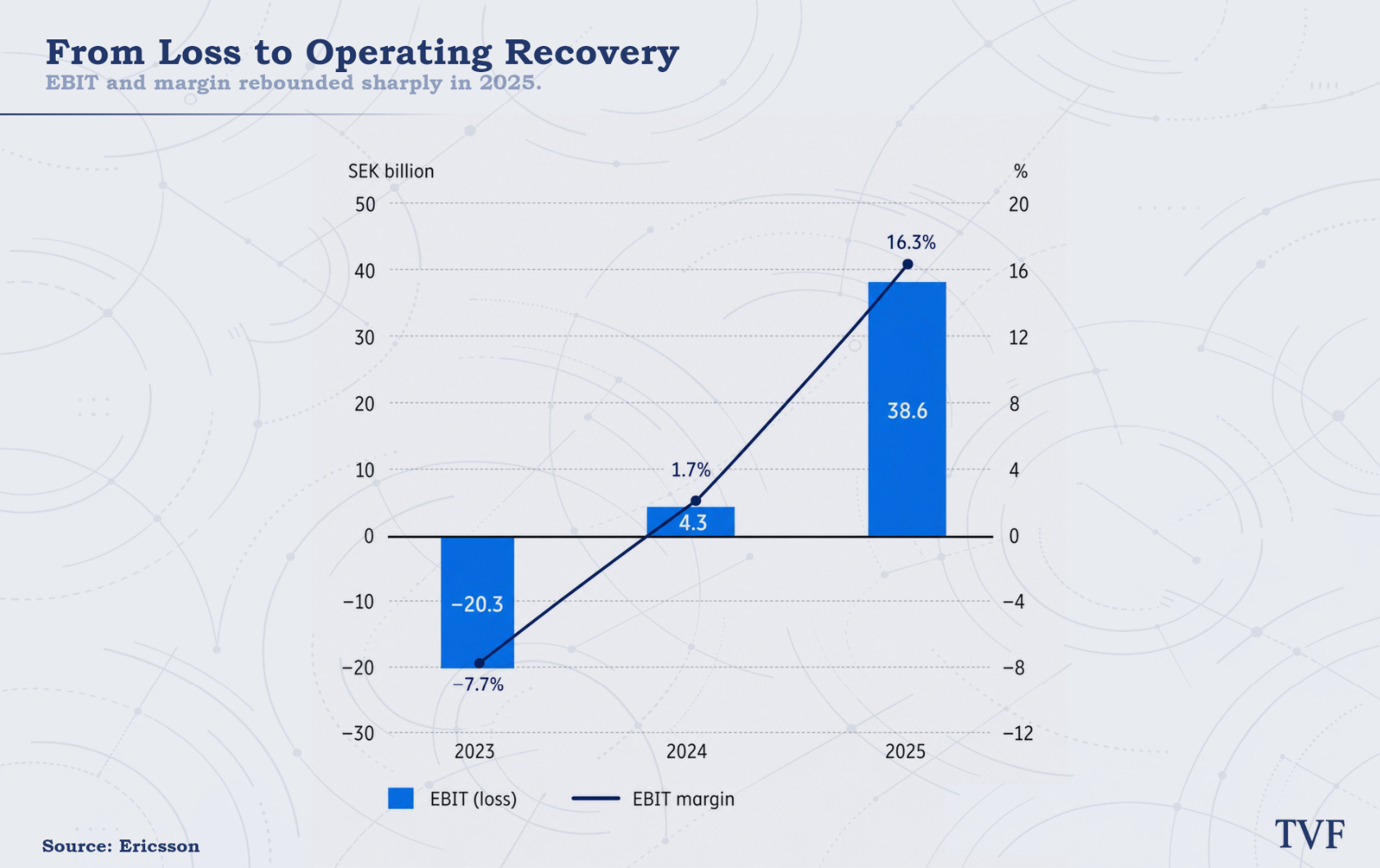

That shift is visible in the model. In 2025, EBIT came in at SEK 38.6 billion, but that year also included favorable effects and should not be treated as the new base. We therefore normalize EBIT to SEK 28.1 billion in 2026. After that, EBIT gradually rises to SEK 34.9 billion in 2031, while the EBIT margin increases from around 12.0% to 13.5%.

That is not an aggressive assumption. It remains below the 2025 peak and assumes no major breakthrough from Vonage or network APIs. The improvement mainly comes from the proven core: Networks, IPR, software upgrades and discipline in costs and working capital.

Free cash flow: the key financial anchor

For Ericsson, free cash flow is the key financial anchor. The company needs to keep investing heavily in R&D every year, pay the dividend, fund buybacks and still maintain enough flexibility for a cyclical market.

In 2025, Ericsson generated SEK 34.3 billion in free cash flow. In our model, this falls back to SEK 24.2 billion in 2026, mainly due to normalization after a strong 2025, higher capex and a less favorable working capital contribution. After that, FCF gradually rises to SEK 29.2 billion in 2031.

That is not spectacular growth, but it is healthy. If Ericsson can continue generating around SEK 25–30 billion in annual free cash flow, there is enough room to support the key priorities at the same time: R&D, dividend, moderate buybacks and balance sheet flexibility.

On a per-share basis, the picture looks stronger. Due to share buybacks, the share count declines from approximately 3,333 million in 2025 to 2,775 million in 2031. As a result, FCF per share rises from SEK 7.70 in 2026 to SEK 10.51 in 2031. That is exactly where a significant part of the upside lies: limited revenue growth, but rising cash flow per share.

Buybacks are useful, but must remain disciplined

Ericsson has enough balance sheet room to return capital to shareholders, but timing matters.

In 2026, we model SEK 15 billion in buybacks, on top of SEK 9.9 billion in dividends. That temporarily brings total shareholder distributions to 102.9% of FCF. That is high, but not immediately problematic as long as it remains temporary and the balance sheet is strong enough.

After that, we normalize buybacks to SEK 10 billion in 2027, SEK 8 billion in 2028 and SEK 6 billion per year from 2029 onward. From that point, coverage becomes more comfortable: coverage rises from 97.2% in 2026 to 122.5% in 2027 and toward 170% in 2030/2031.

That makes the capital allocation more credible. Ericsson uses the balance sheet for a large buyback in 2026, but then shifts back to a more sustainable rhythm. In a flat RAN market, that is sensible. Buybacks are valuable when valuation is low, but dangerous when they come at the expense of R&D or financial flexibility.

R&D remains the hard floor

The main reason Ericsson cannot distribute capital too aggressively is R&D.

Ericsson needs to keep investing around USD 5 billion annually to remain relevant in 5G Advanced, 6G, Ericsson Silicon and standardization. Those expenses pressure short-term profit, but protect the future patent position and installed base.

This makes Ericsson different from a company that can simply cut costs to temporarily boost margins. Cutting too much from R&D may look attractive in the short term, but would damage the moat in the long term. Ericsson’s financial health should therefore not only be assessed on dividend coverage or buybacks, but especially on whether the company can keep funding its R&D red line without weakening the balance sheet.

In our base case, it can. Capex remains relatively low, FCF stays positive and shareholder returns are better covered after 2026. But it requires discipline. The room for error is smaller than for a true growth compounder.

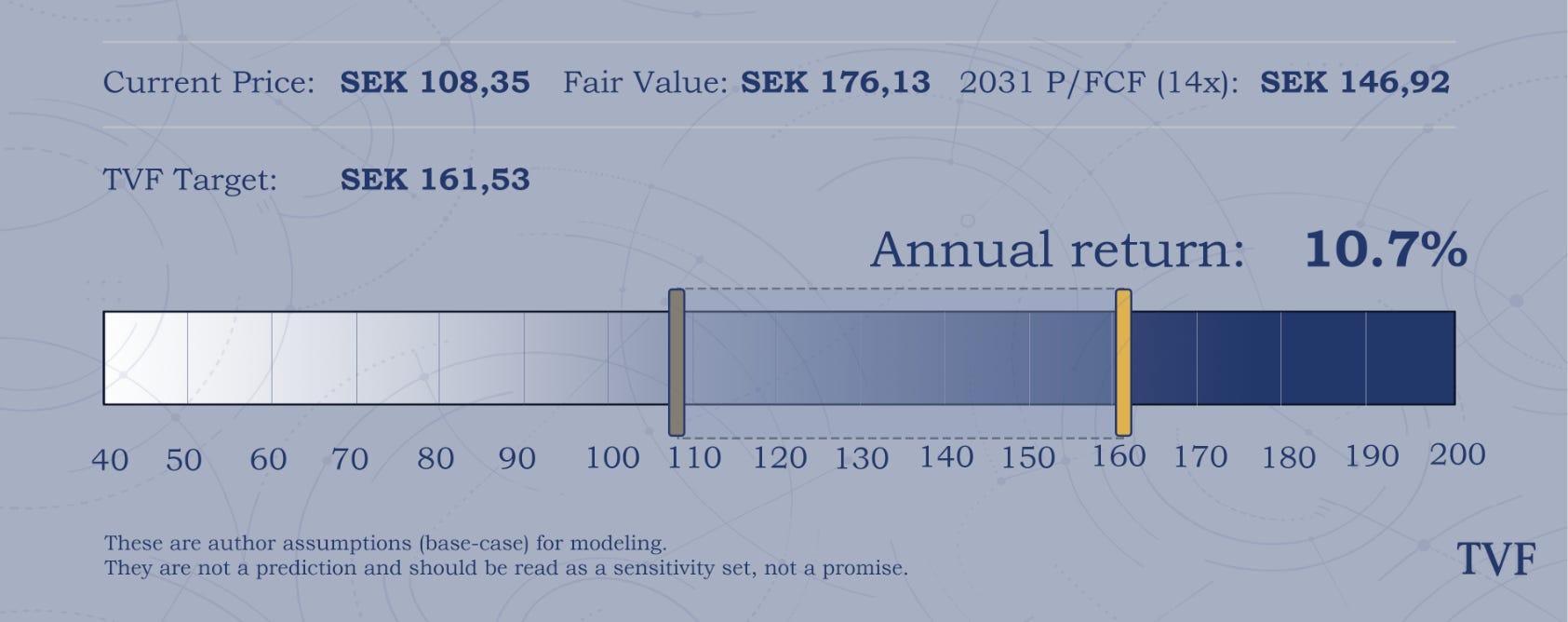

Valuation summary

Today: SEK 108.35

DCF fair value: SEK 176.13

Based on 6.9% WACC and 1.0% terminal growth

2031 P/FCF target: SEK 146.92

Based on 14x P/FCF

TVF Target: SEK 161.53

Expected total return: 10.7% per year, composed of:

6.9% price return

3.8% dividend yield

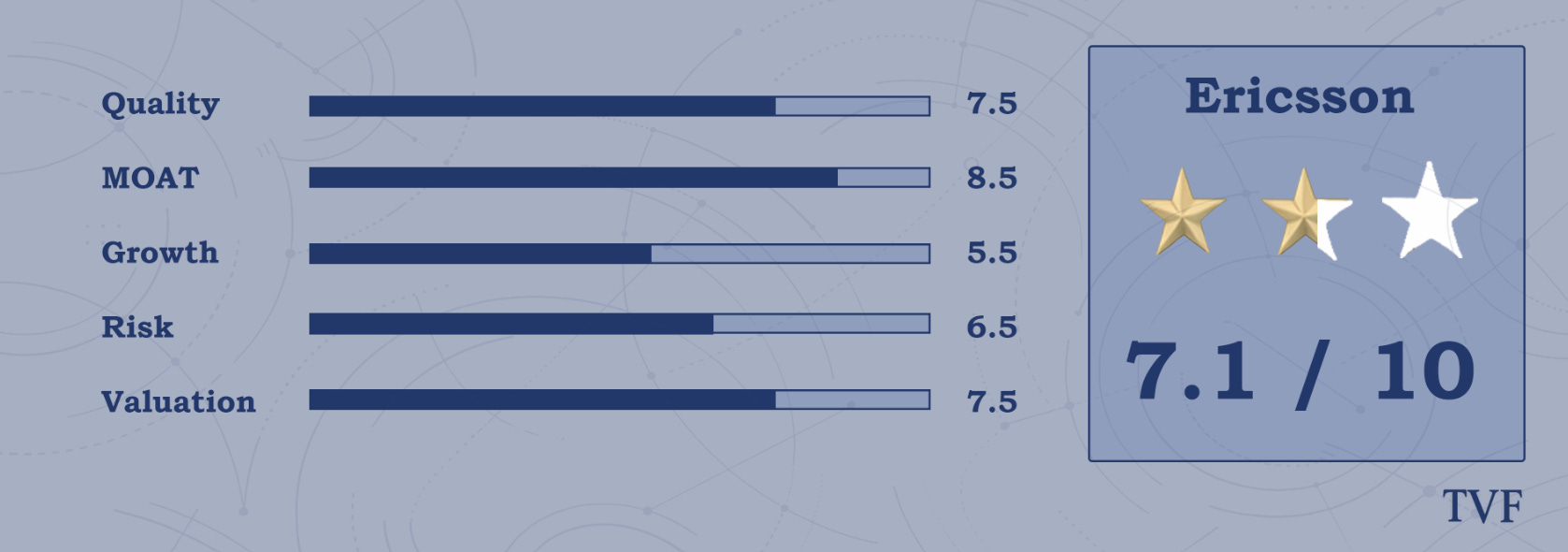

Chapter 7: Rating

Quality — 7.5/10

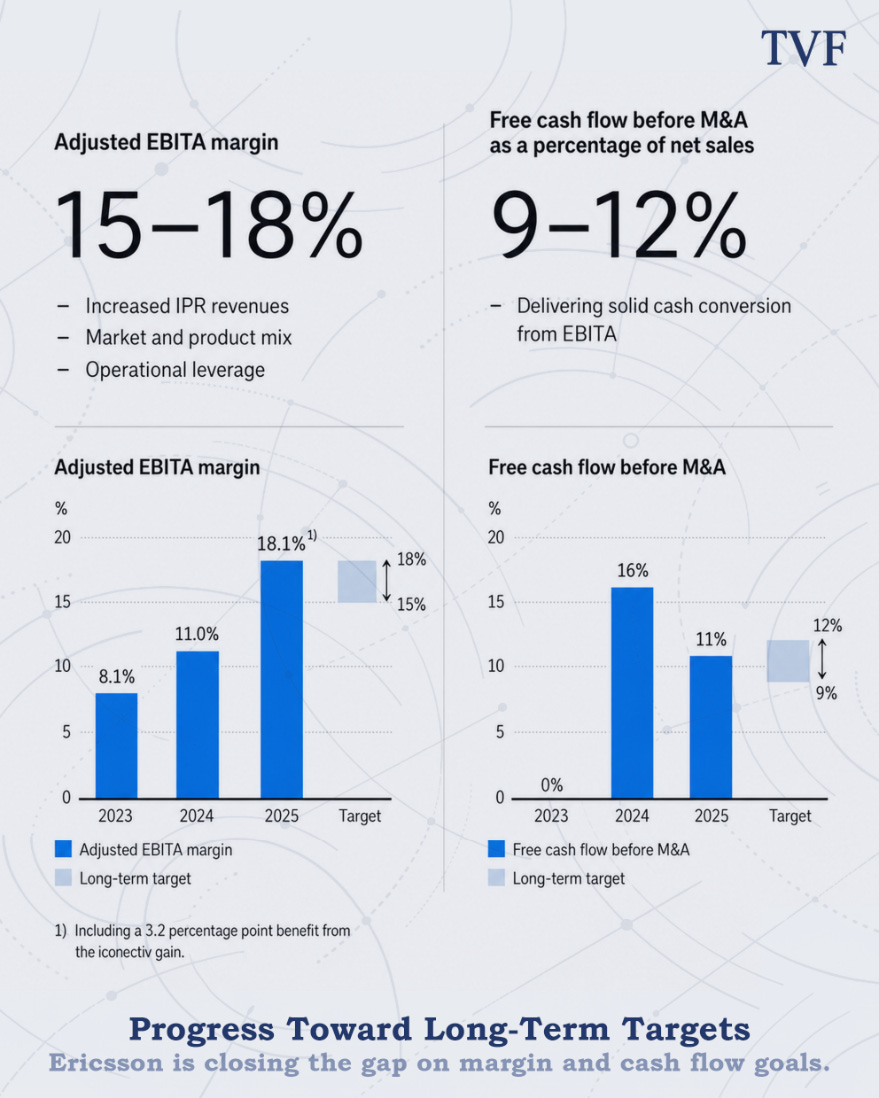

Ericsson is higher quality than the revenue trend suggests. The company has a robust balance sheet, low capital intensity, strong R&D discipline and a valuable IPR layer that generates approximately SEK 13–14 billion in annual patent income. Gross margin has also improved significantly, and the company is proving that it can remain profitable even in a difficult RAN market.

Still, Ericsson is not top-tier quality in the sense of being a stable compounder. Revenue remains dependent on operator capex, large contract cycles and regional investment waves. In addition, the Vonage acquisition destroyed a lot of capital, with approximately SEK 43.3 billion in impairments in 2023 and 2024. The core quality is therefore high, but management’s track record outside the core remains a clear stain.

MOAT — 8.5/10

Ericsson has a strong and layered moat. The most important layer is its IPR position: more than 60,000 patents and a structural royalty base that is less cyclical than hardware sales. In addition, Ericsson benefits from high switching costs, deep operator relationships, proprietary Ericsson Silicon, R&D scale advantages and geopolitical tailwinds in Western markets where Huawei and ZTE are restricted.

The moat is not perfect, however. Telecom operators remain powerful customers who apply price pressure through tenders. Huawei remains the global technology and cost benchmark, while Open RAN could pressure hardware margins over the long term. Ericsson’s moat mainly protects relevance, installed base and software/IPR revenue, but does not provide unlimited pricing power.

Growth — 5.5/10

Growth is the weakest part of the investment case. The RAN market barely grows structurally; for 2025–2030, analysts expect around 1% annual growth. Ericsson’s revenue declined from SEK 263.4 billion in 2023 to SEK 236.7 billion in 2025, and in our model revenue only gradually rises to SEK 258.7 billion in 2031.

The growth opportunities exist, but they are not automatic. 5G Standalone, Fixed Wireless Access, software upgrades, India, AI-native networks and network APIs can all contribute. But many of these drivers depend on operator ROI. Vonage and API monetization in particular remain option value for now, not proven growth engines. Ericsson is therefore more of a cash flow and margin recovery story than a true growth case.

Risks — 6.5/10

The risks are average to elevated. Ericsson is exposed to cyclical operator capex, weak European telecom economics, hardware price pressure, geopolitical restrictions in China and execution risk around Enterprise. Dependence on large customers also makes revenue sensitive to contract timing and investment pauses.

At the same time, the risks are not extreme. Mobile networks are critical infrastructure, Ericsson has a strong balance sheet, low leverage, a high-quality IPR earnings floor and long customer relationships. The biggest risks therefore do not lie in financial survival, but in value destruction from poor capital allocation, persistently weak RAN growth or a failed Enterprise/API strategy.

Valuation — 7.5/10

The valuation looks attractive, but not extremely cheap. Ericsson trades around SEK 108.35, while our combined price target is SEK 161.53 per share. That is based on a DCF fair value of SEK 176.13 and a more conservative 2031 P/FCF target of SEK 146.92 at 14x FCF.

This results in an expected total return of approximately 10.7% per year, consisting of 6.9% price return and 3.8% dividend yield. That is attractive for a company with a strong balance sheet, an IPR floor and buyback capacity. Ericsson does not receive a higher score because structural growth remains limited and Vonage/APIs are not yet proven.

Conclusion

Ericsson is not a classic safe haven against macro stress such as an oil price shock around Hormuz. If energy prices, inflation and interest rates rise again, operators may become even more cautious with capex. In that scenario, Ericsson would still feel pressure through delayed network orders, currency effects and higher costs.

But Ericsson does fit remarkably well into today’s geopolitical economy. In a world where energy, trade routes, chips, telecom and data are becoming increasingly strategic, mobile infrastructure is no longer an ordinary commercial market. Countries want control over who builds their networks, what software is inside them and how dependent they are on China.

That is where Ericsson’s value lies. The company is one of the few remaining Western trusted vendors for critical telecom infrastructure. The EU-India FTA reinforces that picture: India will not become a simple replacement for China, but it is becoming a more important balancing platform for Ericsson — as a 5G market, R&D hub, manufacturing alternative and geopolitical hedge.

For investors, that does not make Ericsson a spectacular growth case, but it does make it an interesting cash flow and infrastructure play. The market still values the company mostly as a flat telecom supplier, while the combination of IPR revenue, buybacks, a strong balance sheet and geopolitical relevance may support more value than the share price currently implies.

Our conclusion therefore remains positive, but not blindly bullish: Ericsson is attractive as long as the core remains healthy, R&D is protected and management does not once again waste too much capital outside its natural zone of power.

If macro-economics is your thing, check out our other newsletters and subscribe. We recommend:

Author: Jeffrey Kieboom

Disclaimer & disclosures: This analysis reflects the author’s opinion at the time of writing and is not investment advice. Investing involves risks, including the possible loss of (part of) the invested capital. All valuation outputs (including DCF, price targets, and expected returns) are model-based estimates and highly sensitive to assumptions (such as cash flows, leverage, capex, discount rate, and terminal growth). Facts may be sourced from public materials considered reliable, but their accuracy cannot be guaranteed.

Position / conflict of interest: The author holds no position in Ericsson. This can change at any time and without prior notice.

Note: I wrote this piece and conducted the research myself. AI was used for feedback/editing support and to generate some of the images.

Wow great article, well done 🏆