Fiscal Dominance: When public debt starts to dictate interest rates

When debt determines the terms.

Over the past few years, investors have mainly focused on central banks. Every inflation print, interest rate decision, and statement from the Fed or the ECB was viewed through one simple lens: when will rates come down?

But perhaps that is the wrong question.

The bigger macro risk is that governments become too large, too dependent on debt, and too politically constrained to bear higher interest rates without consequences. In such a world, monetary policy is no longer only about inflation, but also about the sustainability of public debt.

That is the core of fiscal dominance: a regime in which government debt increasingly determines what central banks can do, how bond markets react, and which assets still deserve a premium.

Dutch newsletter

Disclaimer

Do you appreciate our publication? Then you help us enormously with a like, comment, share and/or restack.

1. Identifying the Problem

The exceptional period after 2008

To understand fiscal dominance, we need to start with the macro environment in which many investors came of age. After the financial crisis of 2008, an exceptional regime emerged: low inflation, low interest rates, and abundant liquidity. Central banks kept policy rates close to zero and bought government bonds on a large scale. As a result, risk premiums fell, debt became cheap, and governments could finance large deficits without being immediately punished by the market.

For many investors, that period started to feel normal, but historically it was exceptional. Governments were able to borrow for years at extremely low interest rates. Companies could refinance cheaply. Households could take out mortgages at rates that seem almost unimaginable today. At the same time, investors could pay higher valuations for future growth because the discount rate remained low. Growth stocks in particular benefited from this, because profits far in the future are worth much more when interest rates are low.

Why the old portfolio logic worked

That regime also had major consequences for portfolio construction. The classic 60/40 portfolio worked well because government bonds often rose when equities fell. When recession fears increased, central banks could lower interest rates, causing bond prices to rise and eventually giving equities support through cheaper money. Duration was therefore not only a source of return, but also a form of protection.

Inflation made debt visible again

Inflation changed that picture. When inflation returned after the pandemic, central banks had to raise interest rates sharply. This brought back an old reality: interest rates are not only a monetary instrument, but also a fiscal factor. When public debt is high, every rate hike eventually means higher interest expenses.

This does not happen immediately across the entire debt stock, because governments only refinance existing bonds gradually. But as old debt matures and new debt is issued at higher interest rates, the effect becomes increasingly visible.

This creates the problem at the heart of this analysis. In the zero-rate world, debt seemed less urgent because the cost of debt remained low. But in a world of positive interest rates, debt becomes visible again. Not only as an abstract percentage of GDP, but as a concrete annual expense in the government budget. Money that goes toward interest payments cannot be spent on defense, healthcare, infrastructure, pensions, or tax cuts.

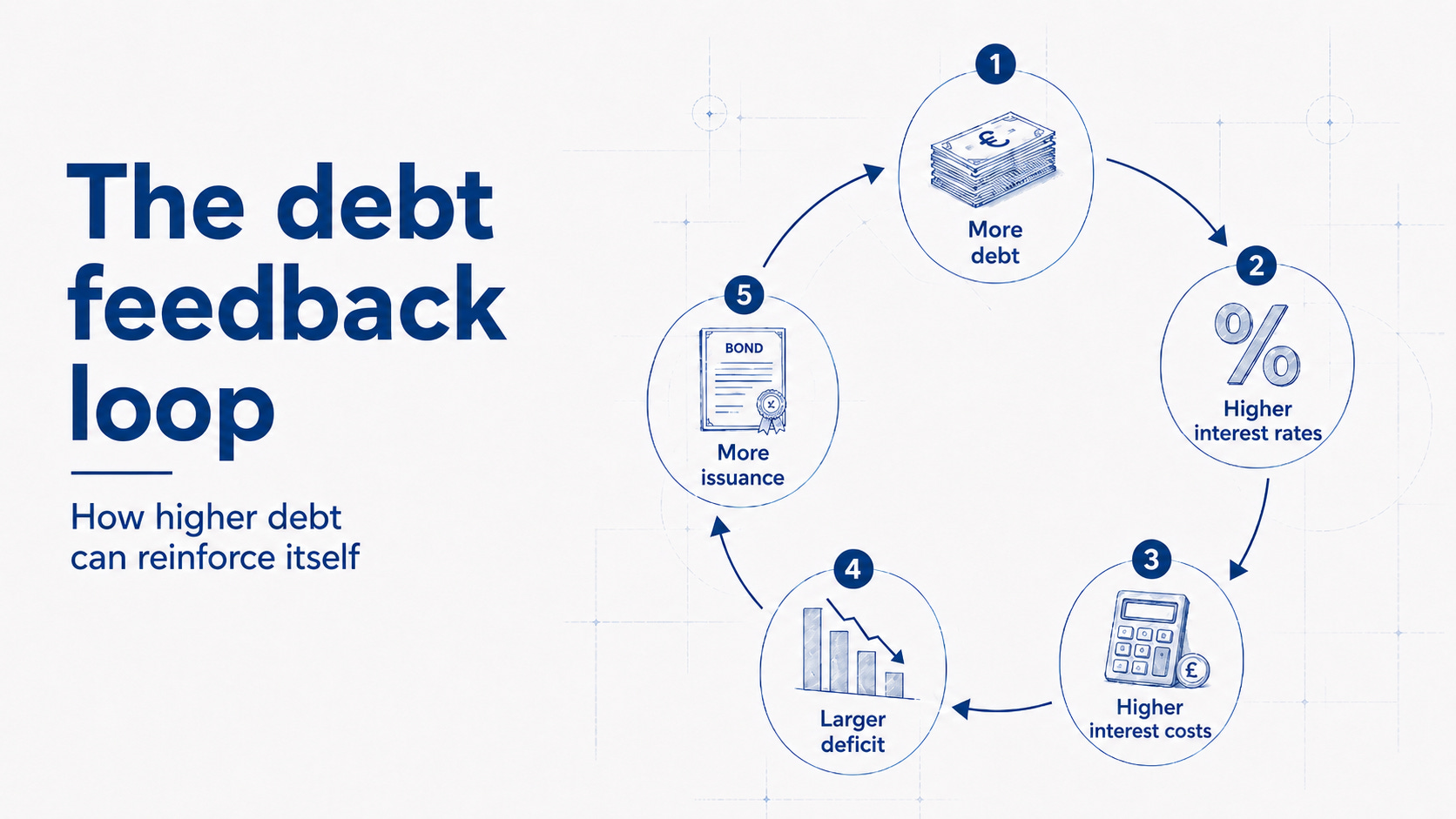

The dangerous feedback loop

The danger is that a self-reinforcing process emerges. Higher debt leads to higher interest payments. Higher interest payments increase the deficit. Larger deficits require more government bond issuance. More bond supply can lead investors to demand a higher yield. In that way, interest rates become not only a consequence of fiscal pressure, but also a new cause of fiscal pressure.

This does not mean that governments will go bankrupt tomorrow. It mainly means that policy space is shrinking. In the old environment, central banks could respond relatively aggressively to inflation or recession. In the new environment, they have to take greater account of a financial system that has become much more sensitive to interest rates.

The question, therefore, is not only whether inflation falls, but also how much interest the system can handle. And above all, how much interest the government can handle.

2. What Fiscal Dominance Means

An economic constraint, not a legal one

Fiscal dominance sounds technical, but the idea is relatively simple. It means that government fiscal policy becomes so dominant that the central bank can no longer conduct policy with complete freedom. This does not have to happen legally. A central bank can remain formally independent while, economically, it has to take increasing account of the consequences of its interest rate policy for public debt, the bond market, and the financial system.

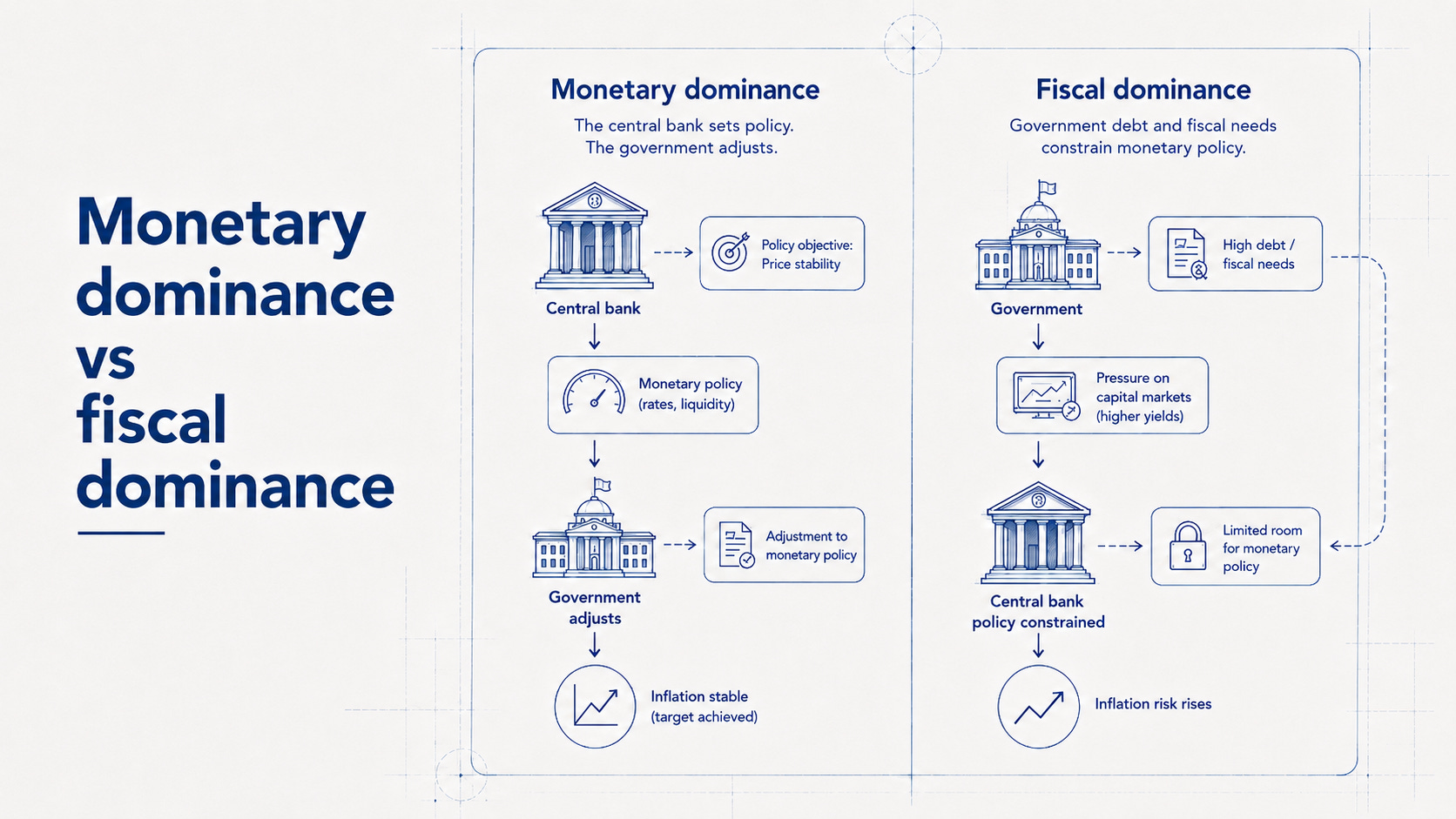

Monetary dominance versus fiscal dominance

In a world of monetary dominance, price stability comes first. If inflation is too high, the central bank raises interest rates. This cools the economy, makes credit more expensive, and reduces inflationary pressure. The government may find this painful, but it has to adjust. Deficits have to be reduced, spending has to be limited, or taxes have to rise. In that regime, the central bank ultimately disciplines the government.

Under fiscal dominance, that relationship slowly reverses. The government then has such large financing needs that the central bank must take the sustainability of public debt into account. Higher interest rates help fight inflation, but they also increase interest expenses. If debt and deficits are high enough, strict monetary policy can create financial stress. The central bank can still pursue its mandate, but the price of doing so becomes higher.

A gradual regime shift

The important point is that fiscal dominance usually does not begin with an official announcement. No central banker will say that, starting today, the inflation mandate is subordinate to public debt. The process unfolds gradually. Markets notice that central banks communicate more cautiously. Governments continue to run large deficits. Bond investors demand more compensation. Political pressure on central banks increases. Slowly, attention shifts from pure inflation fighting to the broader question of whether the financial system can withstand higher interest rates.

Fiscal dominance is therefore not a single moment, but a regime shift. It does not mean that hyperinflation is inevitable. It also does not mean that central banks are powerless. And it does not mean that every high level of public debt immediately becomes problematic. Japan has shown for decades that very high debt can remain sustainable for longer than many investors expect. Institutional factors, domestic savings, inflation expectations, central bank credibility, and who owns the debt all matter.

The price of policy becomes higher

The core issue is that the trade-off changes. When debt is low, a central bank can respond relatively aggressively to inflation. When debt is high, the same rate hike becomes more burdensome because it affects interest expenses, bank balance sheets, housing markets, corporate financing, and political pressure. The central bank can still intervene, but the price of that intervention becomes higher.

For investors, fiscal dominance is therefore not only a macroeconomic concept. It directly affects the discount rate used to value financial assets. If interest rates are determined not only by inflation and growth, but also by how much debt markets are willing to finance, then the valuation of equities, bonds, real estate, gold, and currencies changes.

Ultimately, fiscal dominance is about the question of who disciplines whom. Does the central bank discipline the government, or does the government’s financial position force the central bank to become more cautious? That difference may sound theoretical, but for financial markets it is enormous. In the first regime, government bonds are usually the safe haven. In the second regime, government bonds themselves can become the source of stress.

3. Why This Problem Is Becoming More Relevant

Not only high debt, but structural deficits

The risk of fiscal dominance does not arise only from high debt levels. High debt matters, but the real question is why deficits continue to exist. If large deficits are temporary, for example because of a pandemic or recession, they can later be reversed. But if deficits are caused by structural forces, the problem becomes more persistent.

Today, several structural forces are coming together at the same time.

Aging populations: higher spending and a smaller tax base

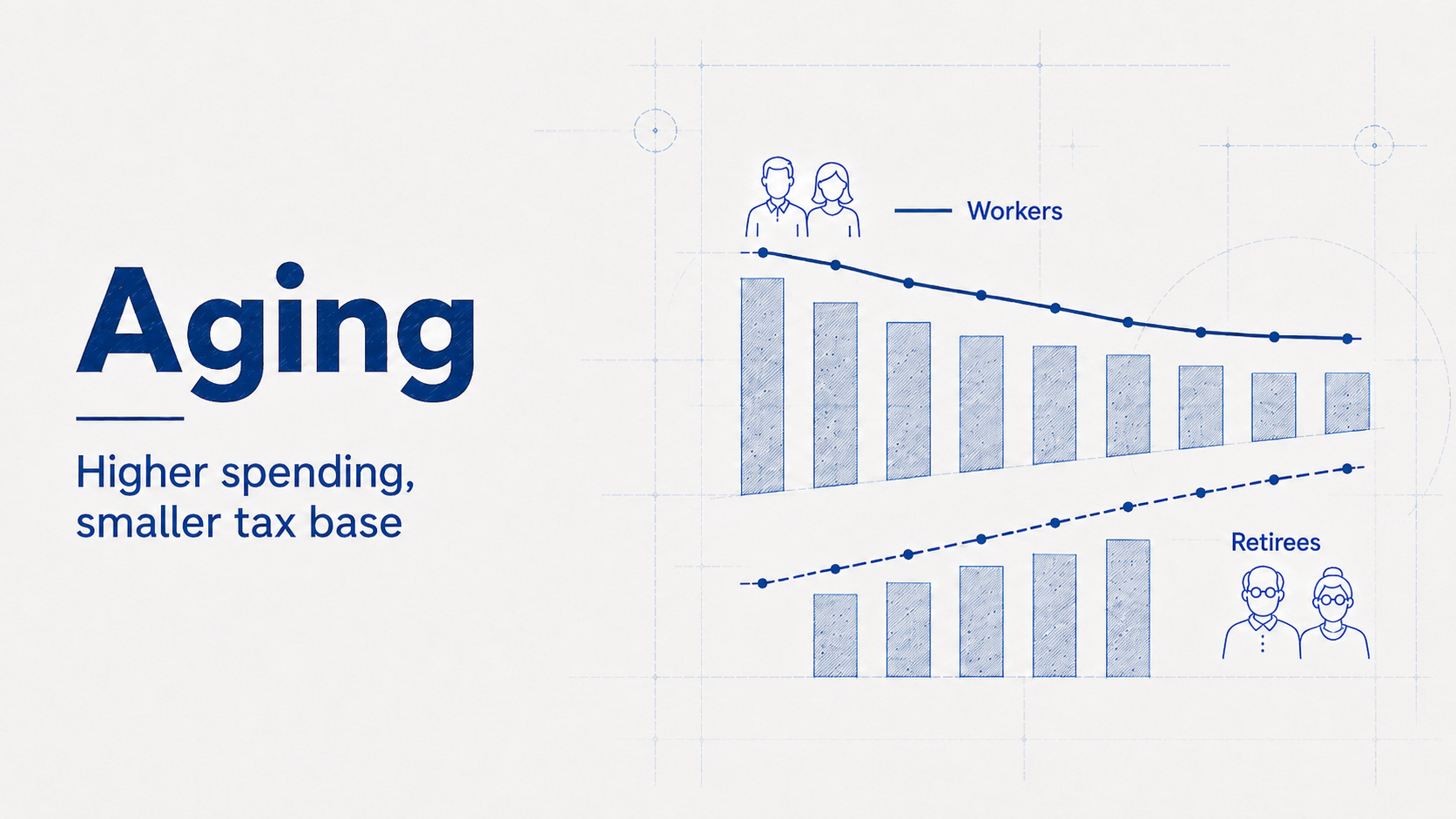

The first is aging. In many developed economies, the share of elderly people is rising relative to the working-age population. This means higher spending on pensions, healthcare, and long-term care, while the growth of the tax base slows. People who retire pay less income tax and fewer social contributions, while they tend to use public services more often. Aging therefore puts double pressure on public finances: spending rises, while revenue grows more slowly.

Politically, this is difficult to solve. Cutting pensions, raising retirement ages, or limiting healthcare spending may be economically defensible, but socially they are sensitive issues. Older voters are also politically influential. As a result, adjustments are often postponed, causing budgetary pressure to increase gradually.

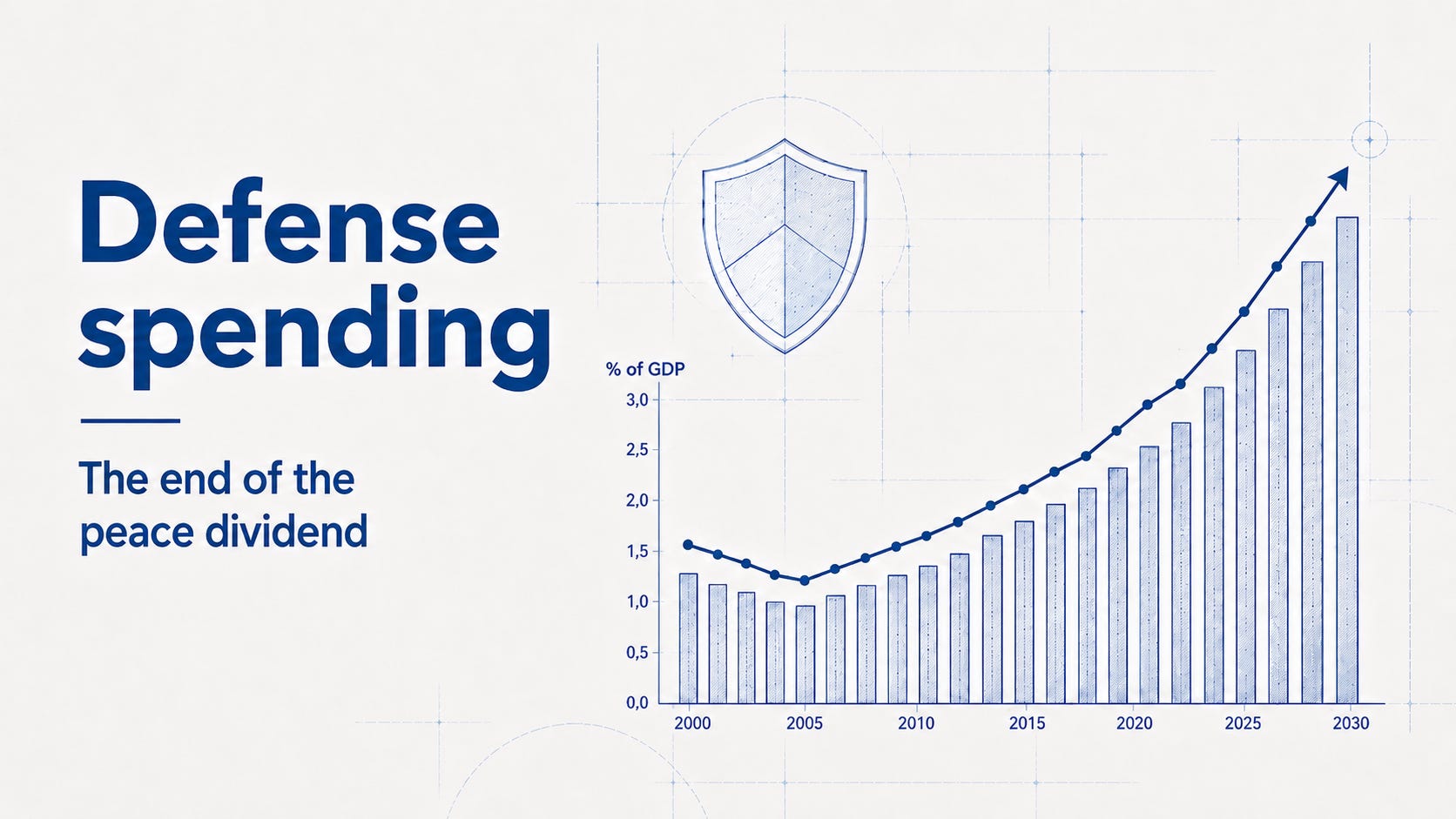

Defense: the end of the peace dividend

The second structural force is defense. After decades of enjoying the peace dividend, European countries in particular have to reinvest in military capacity. This is not a small cyclical expense, but a structural reprioritization. Armies have to be modernized, ammunition stocks have to be replenished, production capacity has to be built up, and technologies such as drones, cyber capabilities, and air defense are becoming more important. For many NATO countries, this means that defense spending does not need to rise temporarily, but permanently.

That makes defense different from a normal cyclical expense. A temporary crisis measure can later be phased out. But geopolitical uncertainty and military shortfalls require years of investment. For Europe, this comes on top of existing pressure from aging populations, energy, and weaker growth. As a result, the fiscal puzzle becomes more difficult.

Energy: climate policy becomes security policy

The third force is energy. The energy transition requires major investments in grids, storage, electrification, renewable energy, nuclear power, and industrial adaptation. At the same time, energy security has become more important since the geopolitical shocks of recent years. Governments want to be less dependent on hostile or unstable suppliers. This requires subsidies, guarantees, strategic reserves, and infrastructure investments.

The energy transition is therefore not only a climate project, but also a national security project. Governments need to invest in cleaner energy, but also in reliable energy. They need to expand grids, support industry, protect households from price shocks, and reduce strategic dependencies. All of these are policy goals that cost money, and many of these expenses will not disappear by themselves.

Industrial policy: the state returns

The fourth force is industrial policy. The state is back as an active player in the economy. Chips, batteries, artificial intelligence, defense, pharmaceuticals, critical raw materials, and energy infrastructure are increasingly seen as strategic sectors. Governments no longer want to be fully dependent on global markets, especially when geopolitical tensions are rising.

This means more subsidies, tax incentives, public guarantees, and sometimes direct investment. This shift fits into a broader trend in which efficiency becomes less dominant and resilience, security, and control become more important. But that shift has a price. Less dependence often means less efficiency, and less efficiency means higher costs.

Interest expenses: debt feeding on itself

The fifth force is interest expenses themselves. This may be the most dangerous one, because debt can start feeding on itself. Higher debt leads to higher interest payments, higher interest payments increase the deficit, and larger deficits require more bond issuance. If investors then demand a higher yield to absorb that additional debt, the problem grows.

The problem is therefore not one isolated crisis. The problem is that many structural expenses are arriving at the same time. A government may be able to increase defense spending without immediately running into trouble. Or absorb pension expenses. Or invest in energy. Or pay higher interest. But when all of these forces are present at once, fiscal space becomes scarce.

Who pays the bill?

Once fiscal space becomes scarce, the political question becomes who has to bear the adjustment. It can be taxpayers through higher taxes. It can be citizens through lower public spending. It can be bondholders through inflation or negative real interest rates. It can be future generations through higher debt. It can be central banks through looser policy than would strictly be desirable. In practice, it will often be a combination.

In a more extreme scenario, even a monetary reset could become part of the debate, as Ray Dalio regularly describes. This means that debt is ultimately not resolved only through normal fiscal discipline, but through a broader adjustment of the monetary system, financial repression, inflation, or redistribution between savers, debtors, and governments. This is not the base case, but it is a scenario that investors cannot fully ignore.

4. How Fiscal Dominance Becomes Visible in Markets

Not a single indicator, but a pattern

Fiscal dominance does not suddenly appear as one clear indicator on a screen. It becomes visible through market prices. Not in one data point, but in a combination of signals: higher long-term interest rates, rising term premiums, steeper yield curves, weaker currencies, higher inflation risk premiums, and more volatility in government bonds.

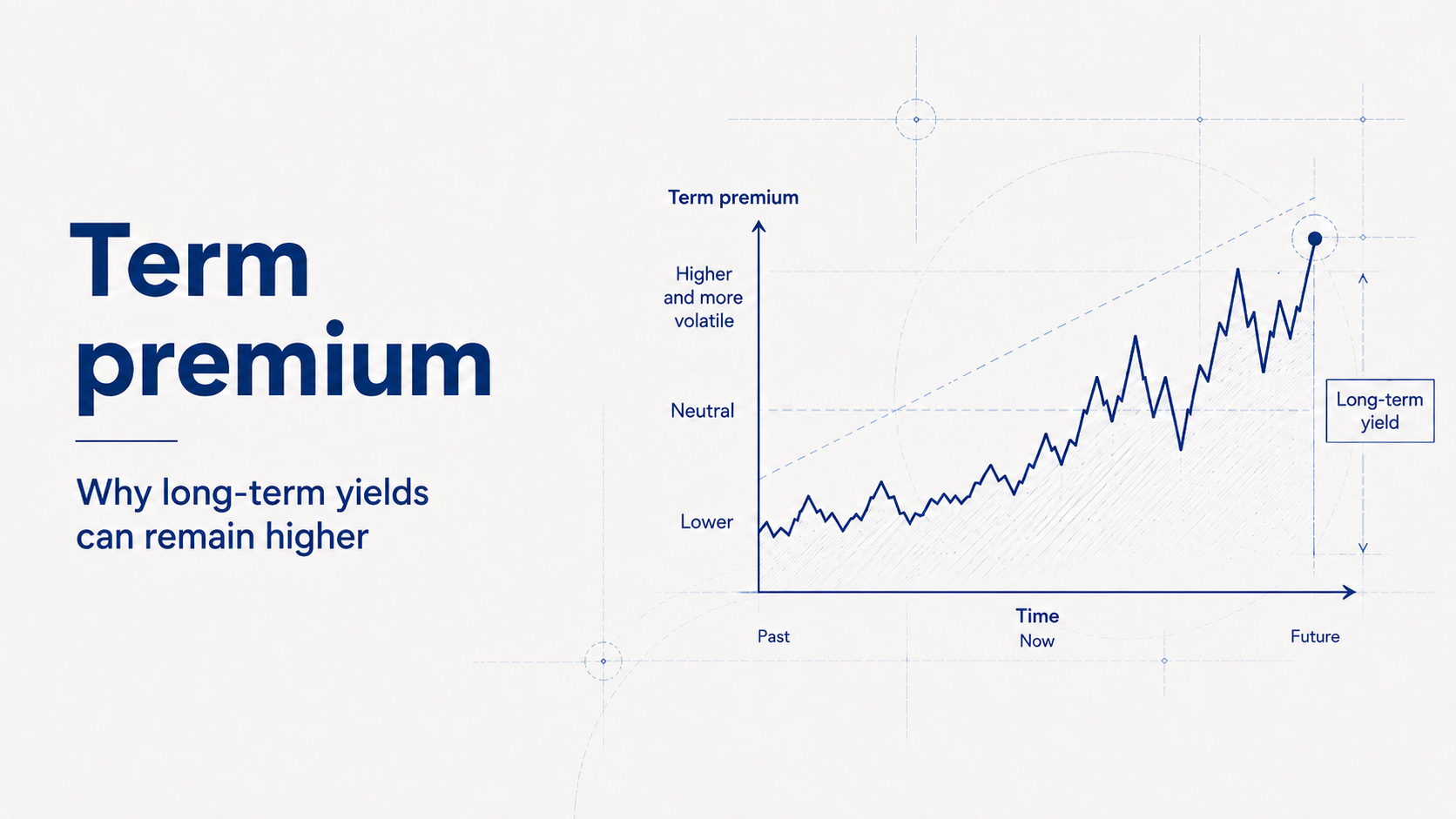

Signal 1: a higher term premium

The first signal is a higher term premium. The yield on long-term government bonds does not only reflect expectations about future short-term interest rates. Investors also demand compensation for uncertainty. That uncertainty can relate to inflation, debt sustainability, bond supply, or volatility. If governments structurally issue more debt, markets have to absorb those additional bonds. That usually becomes easier when investors receive higher compensation for doing so.

A rising term premium can therefore be a sign that investors are less willing to hold long-term government bonds at low yields. For equities, this matters because many valuations are sensitive to long-term interest rates. Even if central banks lower short-term rates or keep them stable, a higher term premium can keep the discount rate elevated.

Signal 2: a steeper yield curve

A second signal is a steeper yield curve. In a classic recession scenario, central banks lower short-term interest rates and long-term rates often fall as well. But in a fiscal dominance environment, things can unfold differently. The central bank may cut short-term rates because the economy is slowing, while markets remain concerned about budget deficits, bond supply, and inflation risk. In that case, long-term rates remain high or fall much less.

That would be an important difference from the old regime. In the past, weaker growth often meant falling interest rates across the entire curve. In a world with fiscal pressure, short-term rates can fall while long-term rates remain relatively high. For investors, this means that central bank cuts do not automatically lead to sharply lower financing costs for governments, companies, and households.

Signal 3: currency pressure

A third signal is currency pressure. If investors doubt a country’s fiscal credibility, they may demand a higher risk premium or move capital into other currencies. For countries with a reserve currency, this process usually unfolds slowly. For emerging markets, it can happen much faster and more violently.

A weaker currency can then increase inflation through import prices. This puts the central bank in a difficult position again. If it raises interest rates to defend the currency and fight inflation, interest expenses rise and pressure on the economy increases. If it lowers rates to support the economy and the government, the currency may weaken further and inflation may rise again. These kinds of dilemmas are exactly what fiscal dominance is about.

Signal 4: a higher inflation risk premium

A fourth signal is a higher inflation risk premium. Fiscal dominance does not have to lead to extreme inflation. It can also mean that inflation becomes somewhat higher and more volatile than investors had become used to. Not necessarily a world of 10% inflation, but perhaps a world in which 2% is no longer automatically the anchor.

For valuations, that makes a major difference. A small increase in expected inflation or inflation volatility can have large consequences for bonds and growth stocks. Investors then demand more compensation for uncertainty, making future cash flows less valuable. In such an environment, inflation also becomes a distribution mechanism. The bill for high debt can partly fall on savers and bondholders through a loss of purchasing power.

Signal 5: more volatility in government bonds

A fifth signal is more volatility in government bonds. In the old regime, government bonds were often the safe asset. When equities fell because of recession fears, bonds rose because interest rates declined. But if stress comes from inflation, deficits, or debt sustainability, bonds can fall at the same time as equities. Investors already saw this in 2022, when inflation and rate hikes hit both sides of the portfolio.

In a fiscal dominance regime, duration therefore becomes an active choice rather than an automatic hedge. Government bonds remain important. They are liquid, they provide income, and they can offer protection in a classic recession. But they are not always the safe haven investors became used to. The relevant question is not only how much yield a bond offers, but also which macroeconomic shock it is vulnerable to.

The bond market as a disciplining force

The market often focuses on the next interest rate decision. Fiscal dominance forces investors to look further ahead. Not only at what the central bank does next month, but at who has to buy the growing stock of government debt, at what interest rate, and with how much confidence. In a monetary dominance regime, the central bank is the anchor. In a fiscal dominance regime, the bond market becomes more important as a disciplining force.

5. What Does This Mean for Investors?

A regime question, not a simple asset call

Fiscal dominance is not a simple buy-this-sell-that analysis. It is primarily a regime question. If the relationship between central banks, governments, and markets changes, then the way investors should think about assets also changes. The most important implication is that old correlations become less reliable. Government bonds are not automatically safe havens, growth is not automatically valuable if the discount rate rises, and nominal revenue growth is not the same as real value creation.

Equities: higher revenue is not automatically value creation

For equities, fiscal dominance is not automatically negative. A world with higher budget deficits, more government spending, and higher nominal growth can even appear positive for corporate profits in the short term. If governments continue to spend money on defense, energy, infrastructure, and industrial policy, clear winners will emerge. Companies that supply strategic sectors can benefit from structural public demand.

But the valuation picture becomes more complex. Equities are claims on future cash flows. The value of those cash flows depends on growth, margins, and the discount rate. Fiscal dominance can support the first factor, but put pressure on the third. Higher nominal growth can increase revenue, but higher long-term interest rates reduce the present value of future profits.

That is why the difference between nominal growth and real value creation becomes crucial. A company can report 8% revenue growth in a world with 4% inflation and rising costs, but shareholders do not automatically become richer as a result. If margins are under pressure and the multiple contracts, nominal growth can be misleading.

Duration equities and valuation pressure

The greatest vulnerability lies with duration equities. These are companies whose valuations depend mainly on cash flows far in the future. Think of growth companies with high multiples, low current profits, or heavy investment needs. When the discount rate rises, distant cash flows become less valuable. That does not mean such companies are bad, but it does mean that the price investors pay for them becomes more sensitive.

Quality, pricing power, and political risks

Quality therefore becomes more important. Companies with pricing power can pass on higher costs without immediately losing demand. Companies with strong balance sheets are less dependent on expensive refinancing. Companies with real assets, regulated income, or structural government demand may be better suited to an environment in which the state plays a larger role. Think of defense, energy infrastructure, grid operators, certain banks, insurers, quality industrials, and companies with dominant market positions.

At the same time, political analysis becomes more important. Governments that spend more will eventually also look for more revenue. Higher taxes, price regulation, windfall taxes, and political pressure on profits may become more common. In a world in which the state becomes more important, it is not enough to look only at revenue growth and margins. Investors also need to think about political vulnerability.

Bonds: the safe haven is less self-evident

For bonds, fiscal dominance may be even more important. The classic portfolio logic is built on the idea that government bonds provide stability. If the economy slows, interest rates fall and bond prices rise. This allows bonds to partially offset equity declines. But that logic mainly works when recession risk is the dominant shock. If inflation or debt sustainability becomes the dominant shock, the picture changes. Then equities and bonds can fall at the same time.

The first lesson is that the risk-free rate is not free of all risks. Government bonds from countries with their own currency often carry little nominal default risk. The government can, in theory, pay in its own currency. But that does not mean investors are protected. They still bear inflation risk, duration risk, and repricing risk. You may get your money back in nominal terms, but purchasing power can decline.

Duration, inflation-linked bonds, and cash

The second lesson is that duration becomes an active choice. Long-term bonds can be attractive if the economy slows sharply and interest rates fall. But they are vulnerable if term premiums rise or inflation remains sticky. Inflation-linked bonds can be useful, but they are not a perfect solution. They protect against realized inflation, but they remain sensitive to real interest rates. If real rates rise, inflation-linked bonds can also fall.

Cash, by contrast, has regained a role. In the zero-rate world, cash was almost a cost. Now that positive interest rates have returned, cash has option value. It does not provide perfect protection against inflation, but it does provide flexibility. In a volatile market, flexibility can be valuable.

Gold, bitcoin, and real assets

When investors worry about fiscal dominance, attention often shifts toward assets outside the traditional government money system. Gold, bitcoin, commodities, real estate, and infrastructure are then seen as protection against inflation, monetary debasement, or a loss of confidence in governments.

Gold is the classic hedge. It has no cash flow, no management team, and no earnings growth. That makes it unattractive to many investors. But precisely this absence of obligations makes gold interesting in a world in which government money becomes more political. Gold is not someone else’s promise. It can become attractive when confidence in currencies, real interest rates, or fiscal credibility declines. Still, gold is not magical protection. It can underperform for years, it is sensitive to real interest rates, and it produces nothing. Gold is more like insurance than a productive investment.

Bitcoin is often presented as digital protection against monetary debasement. The argument is understandable: a fixed maximum supply, no central bank, and no government that can increase the supply. But bitcoin is much more volatile than gold and does not yet have a long history as a stable crisis hedge. It can work as a speculative hedge against distrust in fiat money, but it often also behaves like a risky technology asset.

Real assets form a third category. Real estate, infrastructure, energy, commodities, and land can provide protection against inflation because they are linked to physical scarcity. But nuance is also needed here. Real estate is sensitive to financing costs. Infrastructure can be regulated. Commodities are cyclical. Energy companies can face political pressure or windfall taxes.

No hedge protects against everything

The biggest mistake is thinking that every inflation hedge is automatically a good investment. Price still matters. An asset can make macroeconomic sense and still be too expensive. Fiscal dominance makes alternative stores of value more relevant, but not simpler. It forces investors to distinguish between insurance, speculation, and productive assets.

The right portfolio therefore does not have to consist of one asset that protects against everything. That asset does not exist. Robustness is more likely to come from a combination of assets that respond differently to inflation, interest rates, growth, and confidence.

6. Why Fiscal Dominance May Be Overestimated

Not a certainty, but a risk

A good analysis should not only explain the risk, but also show why the risk may be overestimated. Fiscal dominance is a serious theme, but it is not a certainty. There are strong counterarguments that prevent the story from becoming too much of a doom scenario.

Central banks have proven their independence

The first counterargument is that central banks have already proven their independence. After the inflation shock of 2021 and 2022, the Fed, the ECB, and other central banks raised interest rates sharply despite high debt, falling markets, and political pressure. This suggests that central banks are still willing to accept economic pain in order to fight inflation. Fiscal dominance is therefore not a fait accompli. The risk is not that central banks suddenly abandon their mandate, but that the cost of carrying out that mandate gradually increases.

Debt sustainability depends on both interest rates and growth

The second counterargument is that debt sustainability does not depend only on debt. A debt-to-GDP ratio says little without looking at the relationship between interest rates and nominal growth. If an economy grows fast enough in nominal terms, a high debt ratio can stabilize or even decline. Inflation also increases nominal tax revenues. That can temporarily help governments, as long as interest expenses do not rise too quickly. High debt is therefore not automatically a crisis. The crucial question is whether the interest rate on the debt becomes structurally higher than the nominal growth rate of the economy.

There remains structural demand for government bonds

The third counterargument is that financial systems have a lot of absorption capacity. Pension funds, insurers, banks, central banks, and foreign investors continue to need government bonds. Regulation also creates structural demand. Banks have to hold liquid assets. Pension funds and insurers have to match liabilities. Institutional investors need safe and liquid instruments. As a result, demand for government bonds can remain strong for longer than skeptics expect.

Japan as a warning against simplistic debt analysis

The fourth counterargument is Japan. Japan has had very high public debt for decades. Yet this did not automatically lead to a classic debt crisis, hyperinflation, or default. This was due to a combination of domestic savings, low inflation expectations, institutional demand for government bonds, and a central bank that pursued very accommodative policy. Japan shows that simple debt ratios are insufficient. Anyone who looks only at debt as a percentage of GDP misses the institutional context.

At the same time, Japan also shows the other side of the story. The longer a financial system becomes accustomed to low interest rates and central bank support, the harder normalization becomes. High debt therefore does not have to lead to an immediate crisis, but it can reduce policy freedom. That is exactly why fiscal dominance is a subtle risk. It is not always about a sudden breaking point, but often about a slow restriction of policy space.

The timing problem

The fifth counterargument is that markets are often too early with debt panic. Investors have warned about debt crises in developed markets for decades. Many of those warnings came too early. Anyone who positions for years around a debt crisis that does not arrive can miss a lot of returns. Fiscal dominance is therefore not a timing model. It does not provide an exact date when bond markets break, inflation rises, or central banks pivot. It is a regime risk whose probability increases as debt, deficits, and political spending promises grow.

The base case is not an apocalypse

These counterarguments matter. They make clear that fiscal dominance does not have to end in a dramatic scenario. The base case could also be that interest rates simply remain structurally higher than they were in the years after 2008, that bonds become more volatile, that inflation becomes less predictable, and that governments play a larger role in the economy. That is less spectacular than a debt crisis, but still highly important for investors.

The biggest mistake is therefore not to see fiscal dominance as a certainty. The biggest mistake is to ignore it completely because it was not visible for many years.

Conclusion: The End of the Old Automatic Logic

Central banks remain important, but not almighty

Fiscal dominance does not mean that central banks disappear. It also does not mean that inflation becomes uncontrollable or that government bonds become worthless. It means something more subtle, but perhaps more important for investors: the room for monetary policy narrows as budgets grow larger, debt rises, and political promises become more expensive.

The old world worked because of low interest rates

Over the past decades, investors lived in a world in which central banks could dominate the cycle. In periods of stress, interest rates fell. When recession fears rose, bonds increased in value. When inflation was low, governments could borrow cheaply. That regime made high valuations, long duration, and the classic 60/40 portfolio attractive.

The coming years require a different framework

The coming years may be different. Governments need to spend more on defense, aging populations, energy, industrial policy, and interest expenses. At the same time, the political willingness to make painful choices is limited. Raising taxes is unpopular. Cutting spending is unpopular. Fighting inflation is painful. Letting debt rise is often the path of least resistance, until markets demand a higher price.

That is the essence of fiscal dominance. Not a sudden crisis, but a slowly shifting balance of power between central banks, governments, and markets.

The new investment question

For investors, the central question therefore changes. It is no longer only about when interest rates will fall. It is also about why interest rates may remain structurally higher. It is about who absorbs the growing stock of public debt. It is about which assets preserve their value when inflation becomes more volatile. And it is about which companies can survive in a world where capital is no longer free.

The most important investment implication is not that you should sell everything or flee into gold. The implication is that the old automatic logic becomes less reliable. Government bonds are not always safe havens. Growth is not always valuable when the discount rate rises. Nominal revenue growth is not the same as real value creation. And central banks cannot be seen as endlessly separate from the government balance sheet.

For the coming decade, one macro question is therefore becoming increasingly difficult to avoid: will the central bank continue to discipline the government, or will public debt eventually discipline the central bank?

That is the question investors need to take into account.

If macro-economics is your thing, check out our other newsletters and subscribe. We recommend:

Author: Ayden van Loon

The Valuation Framework (TVF) turns market and sector news into clear economic models and links those themes to company notes that translate insights into valuation.

This publication is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. It does not take into account your personal financial situation, objectives, or risk tolerance. Investing involves risk, including the risk of loss. Any scenarios, estimates, and forward-looking statements reflect judgment at the time of writing and may change without notice; outcomes may differ materially. The analysis is based on publicly available sources believed to be reliable, but accuracy, completeness, and timeliness are not guaranteed. References to companies, commodities, and markets are illustrative and not endorsements. I may hold positions in securities mentioned, and those positions may change at any time. Nothing in this publication is intended to encourage or facilitate the circumvention of sanctions or other applicable laws and regulations.

Note: I wrote this piece and conducted the research myself. AI was used for feedback/editing support and to generate some of the images.

In a world where governments keep spending and inflation stays sticky, a company can report 8% revenue growth while shareholders get poorer in real terms. That changes how you have to think about valuation. A business with genuine pricing power and low debt looks very different from one that just benefits from inflation temporarily inflating its numbers.