Heineken, Brewed for Returns

The hidden shareholder value behind the iconic green bottle.

HEINEKEN N.V. is at a fascinating strategic crossroads. As one of the most iconic and widely distributed brewers in the world, the company has taken several heavy blows in recent years. Stagnating beer volumes in Western markets, persistent inflationary pressure and geopolitical headaches have put sustained pressure on the share price. The market currently seems to be heavily penalizing the company for these macroeconomic headwinds and remains skeptical. However, anyone who looks critically under the hood will discover a materially different story.

Dutch newsletter

Disclaimer

Do you appreciate our publication? Then you help us enormously with a like, comment, share and/or restack.

Chapter 1: The History and DNA of HEINEKEN

The company’s history begins in 1864, when its founder, Gerard Adriaan Heineken, acquired the “De Hooiberg” brewery in Amsterdam. His strategy was focused on brewing beer at scale that could be exported globally without sacrificing quality or its distinctive taste. This technical and commercial step formed the foundation for the company’s later expansion. The company itself describes this early period as the origin of a pioneering spirit that still plays a role in the organization’s core values today.

Over the course of its 160-year history, the originally local nineteenth-century brewery in Amsterdam has transformed into one of the largest international players in the beverage industry. The most recent data from early 2026 shows that HEINEKEN is now operational in more than seventy countries. The company operates a broad network of breweries, malt houses, cider plants and other production facilities. Its total workforce has steadily grown over this period and currently exceeds 88,000 employees. The company follows a strategy focused on both developed markets and emerging economies, resulting in a geographically diversified sales base. Its brand portfolio, consisting of more than 340 international, regional and local specialty beers and ciders, is sold worldwide in more than 190 countries.

A crucial part of the current business is the specific legal and governance structure that has been used for decades. Since 1952, Heineken Holding N.V. has functioned as the primary entity through which the management and supervision of the HEINEKEN Group are structured. The explicit objective of this overarching holding company is to safeguard the continuity, stability and independence of the brewing group. This structure facilitates a focus on sustainable long-term value creation and protects the company against external influences in a highly consolidating market.

The shareholding structure within this framework is tightly defined. Heineken Holding N.V. owns exactly 50.005% of the issued shares in the operating company Heineken N.V. Within Heineken Holding N.V., a majority stake of 53.171% is held by L’Arche Green N.V., an entity of which the Heineken family owns 88.98% and the Hoyer family owns the remaining 11.02%. The influence of the founding family is also reflected in the governance structure: through representation on the Supervisory Board, it helps safeguard the company’s strategic direction and continuity. To this end, the company operates with a traditional system consisting of an independently operating Executive Board and a supervisory Supervisory Board. This structure forms the administrative foundation that allows HEINEKEN to continue operating as an independent company after more than a century and a half.

Chapter 2: Brand Portfolio and Geographic Revenue

A Streamlined Global Portfolio

The core of the company’s operations is its extensive beverage portfolio. HEINEKEN produces and sells more than 340 international, regional, local and specialty beers and ciders worldwide. These beverages are produced in more than 70 countries and reach consumers in over 190 markets. In the full financial year 2025, HEINEKEN generated total net revenue of €28.89 billion and consolidated beer volume of 234 million hectoliters.

To keep this broad offering manageable and profitable, the company follows a strategy of strict segmentation. The focus is on streamlining the portfolio around five global brands: Heineken, Amstel, Birra Moretti, Tiger and Desperados and 25 strategic local brands, the so-called “power brands.” This approach allows the company to build brand equity through targeted investments and economies of scale, while also remaining locally relevant.

The Dominance and Growth of the Heineken Brand

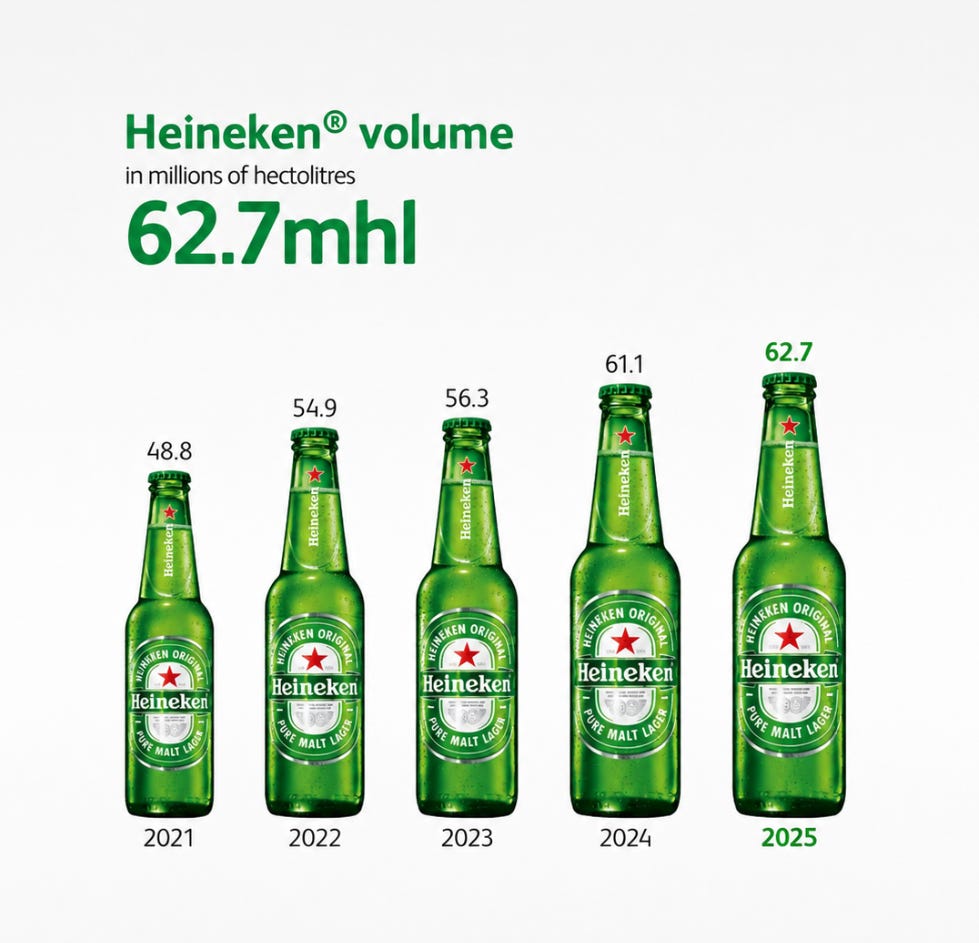

Within the overall beer market, which has been under pressure over the past five years due to macroeconomic shocks, inflation and shifting consumer behavior, the Heineken brand occupies an exceptional position. While the broader beer market has at times shown stagnation or decline, the company’s flagship brand continues to grow structurally. The data shows that Heineken’s sales volume has grown organically by 51% since 2020. In 2025 alone, the brand reached a volume of 62.7 million hectoliters.

As a result, Heineken has gained the global number one position in terms of sales value within the beer category and has been recognized as the world’s most powerful beer brand. The brand’s continued growth, despite a sometimes shrinking overall market, is the direct result of the company’s premiumization strategy. Even in the first quarter of 2026, when the group’s total consolidated beer volume declined marginally by 0.2%, the brand portfolio and especially the premium segment, still showed strong resilience.

Local Brands and the Power of Diversification

Alongside its global brands, the company’s strategy relies heavily on strong local “power brands.” These are brands specifically tailored to regional taste preferences. Examples include Tecate in Mexico, Kingfisher in India, Bintang in Indonesia, Cruzcampo in Spain and Harar in Ethiopia.

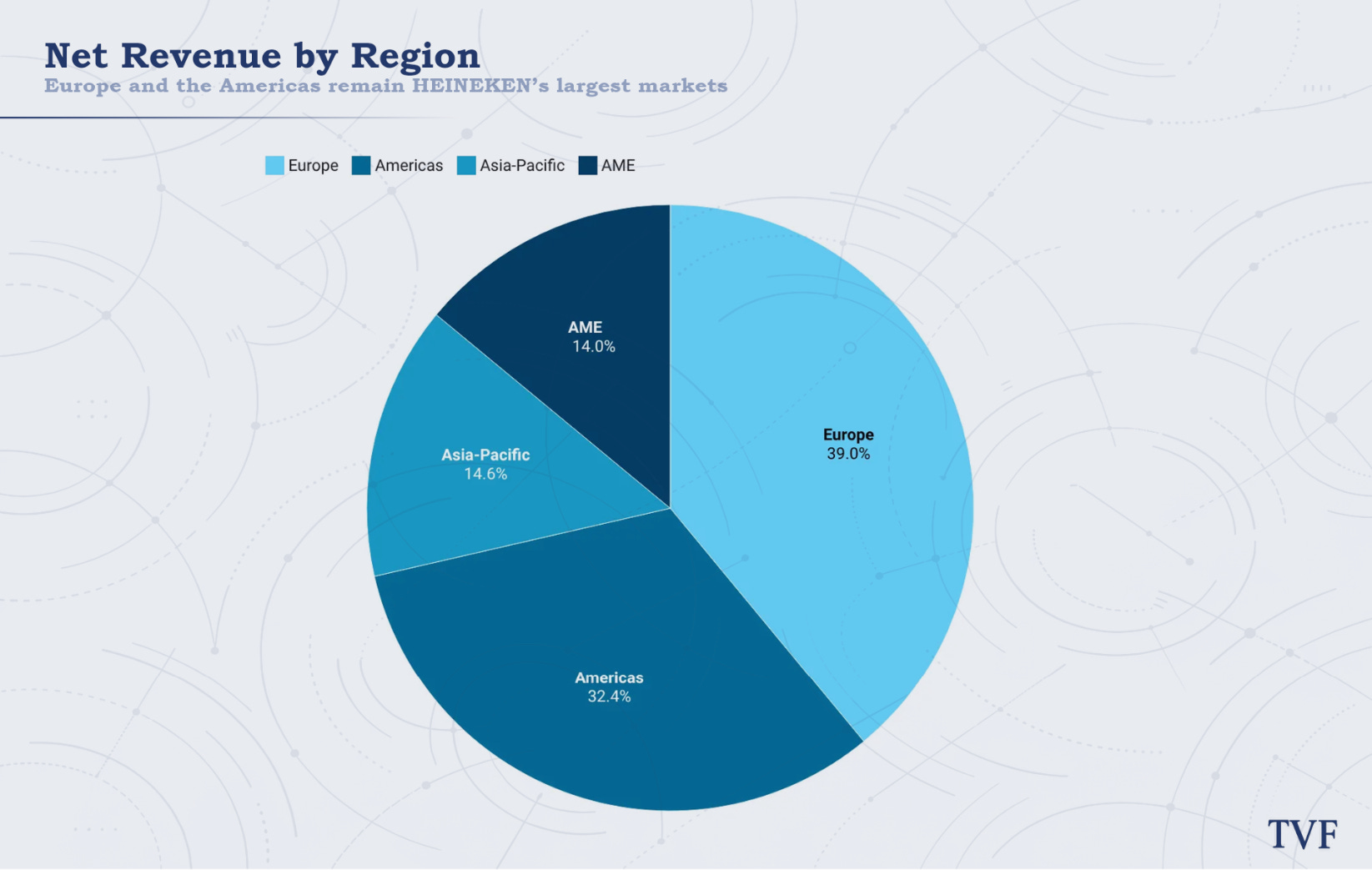

This combination of global and local brands is supported by a well-balanced geographic spread. That spread functions as a risk buffer: contraction in mature markets can be offset by growth in emerging markets. The operational and financial contribution by region in 2025 illustrates this balance:

Europe: Europe is the most financially significant region. In 2025, it generated net revenue of €11.46 billion, representing 39.0% of group revenue, with consolidated beer volume of 73.5 million hectoliters, or 31.4% of the total. Although Europe is a mature market with challenges such as complex regulation, the company managed to hold its ground strongly.

Americas: In terms of physical volume, this is HEINEKEN’s largest region. In 2025, consolidated beer volume amounted to 86.1 million hectoliters, representing 36.8% of the total, resulting in net revenue of €9.54 billion, or 32.4% of group revenue. Key markets in this region include Brazil and Mexico.

Africa and Middle East (AME): This region contributed net revenue of €4.28 billion, or 14.6%, and beer volume of 28.9 million hectoliters, or 12.4%. Despite significant macroeconomic volatility, the region delivered strong performance, driven by price-mix improvements and robust growth in countries such as Ethiopia and South Africa.

Asia-Pacific: The region accounted for net revenue of €4.12 billion, or 14.0%, and volume of 45.5 million hectoliters, or 19.4%. The recent results from the first quarter of 2026 show a striking volume increase of 10.1%, strongly driven by recovery and growth in Vietnam, India and China.

When we compare these four regions financially, a fascinating dynamic emerges between revenue per hectoliter (HL) and actual margin quality. The high revenue per HL in Europe, averaging more than €155 per HL in 2025, undeniably demonstrates the immense pricing power and successful premiumization in this mature Western market. Yet this high revenue per beer by no means tells the full story for investors. The true operating leverage and profitability are not found in the West, but rather in the “growth” regions.

Contrary to what lower absolute revenue per HL in emerging markets might suggest, operating margins in Africa and Asia are structurally higher and more robust than in Europe and the Americas. Asia-Pacific is the absolute crown jewel in this respect: on revenue of €4.1 billion, the region generated more than €904 million in operating profit (beia) in 2025. This translates into an operating margin of as much as 21.9%, more than double the margin in Europe, which was only 11.1%. At the same time, Africa & Middle East achieved a major efficiency gain, with the profit margin expanding by no less than 410 basis points in 2025.

This high profitability demonstrates that volume growth in Eastern and African markets is by no means unprofitable growth. Thanks to a significantly lower cost base, enormous economies of scale in emerging urban areas and successful premiumization, HEINEKEN manages to convert every euro earned in these regions into hard profit far more efficiently.

Chapter 3: Challenges, Reputational Damage and Leadership Transition

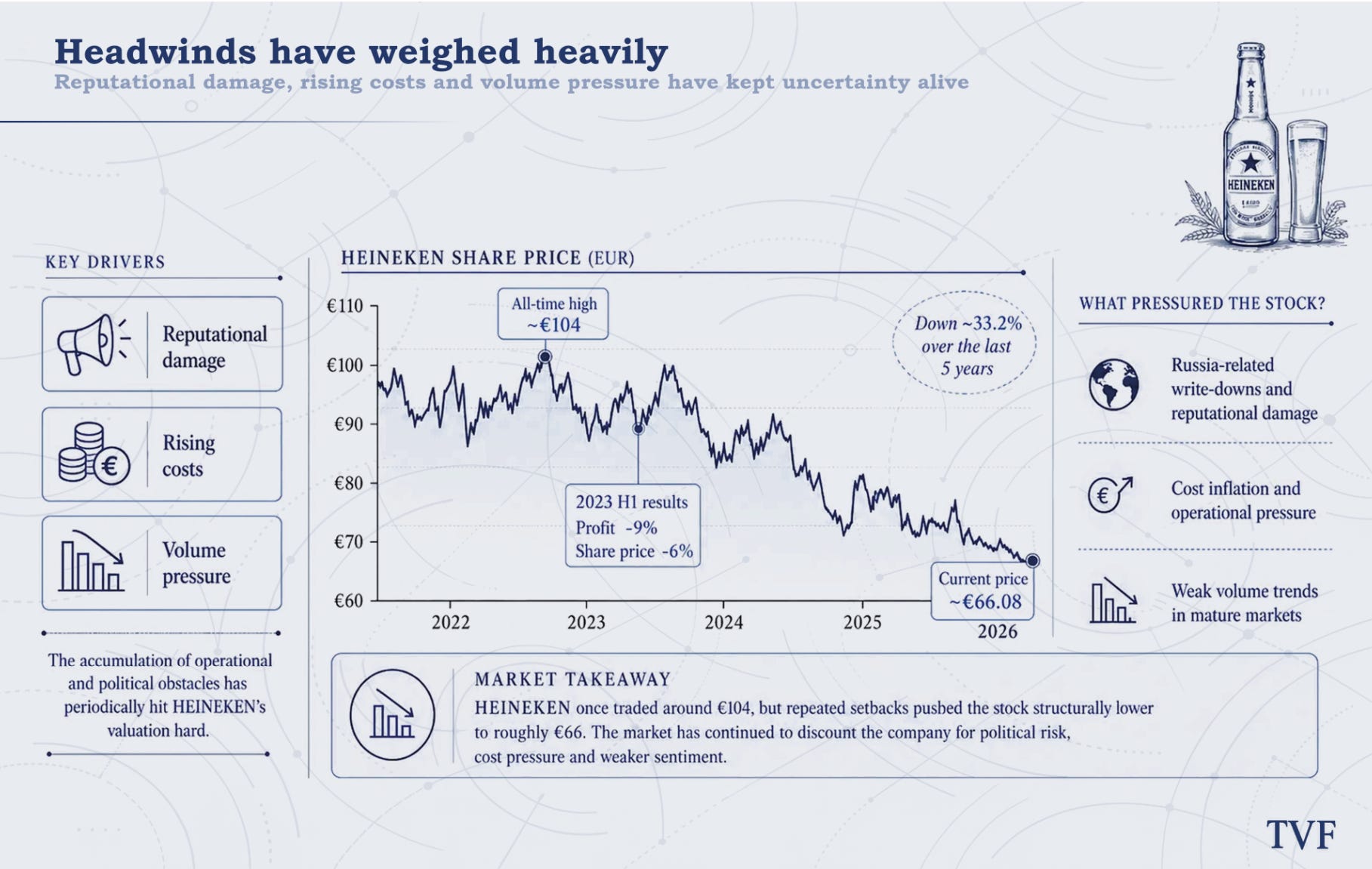

The global diversification highlighted in the previous chapter functions as a strategic buffer, but at the same time increasingly exposes the company to geopolitical and macroeconomic risks. The most striking low point in the brewer’s recent history is the handling of its operations in Russia following the invasion of Ukraine. A country that had been labeled the “cornerstone” of future growth in the early 2000s through acquisitions worth more than €1.2 billion quickly turned into an extremely complex headache.

Reputational Damage

Although HEINEKEN stated its intention to leave the Russian market after the invasion, the exit took considerably longer than it did for some industry peers. The Dutch Association of Shareholders, the VEB, sharply criticized this delay. According to VEB director Gerben Everts, the brewer should have left immediately, even if that meant “setting it on fire” and abandoning all assets. The slow withdrawal caused significant reputational damage, which according to the VEB weighed more heavily in financial and commercial terms than the accounting losses on abandoned equipment. Ultimately, the company fully wrote down its Russian subsidiary to zero in its accounts, resulting in a total impairment of more than €201 million. The final transfer also proved highly cumbersome, partly because authorization was in the hands of the Russian government, which during the same period expropriated assets of Western sector peers such as Danone and Carlsberg and placed them under the control of Putin loyalists.

A Pile-Up of Setbacks

In addition to these severe geopolitical frictions in Eastern Europe, the company is struggling globally with trade barriers and market pressure. For example, HEINEKEN is involved in a lawsuit in the United States to recover import duties imposed on Mexican beer, a direct consequence of international tensions under the Trump administration. Although the company is not dependent on the U.S. market with a market share of around 1.8% for the Heineken brand, the U.S., including the volume of major Mexican brands such as Dos Equis and Tecate, is still an important market. These tariffs therefore directly affected the brewer and cost it a significant amount of money.

Global trade also remains unpredictable more broadly; in the first quarter of 2026, the company’s leadership still pointed to ongoing supply-chain volatility and rising energy costs. Within Europe, lengthy and difficult negotiations with major retail partners in countries such as France, Spain and the Netherlands caused temporary sales disruptions. On top of that, stricter environmental regulations, including the introduction of new deposit-return systems in countries such as Poland and Austria, are forcing the company to make costly and complex operational adjustments.

At the same time, the company is dealing with a general decline in global beer demand. This volume decline is structurally driven by changing consumer preferences; due to a growing societal focus on health and wellbeing, consumers are drinking alcoholic beverages less frequently and the market is increasingly shifting toward alcohol-free beers or other alternatives.

This accumulation of operational and political obstacles naturally did not occur without financial consequences. The combination of reputational damage, rising costs and volume pressure has periodically hit the company’s market value hard. When the company presented disappointing half-year results and a 9% decline in profit in 2023, partly due to the Russian impairments, the stock was hit almost immediately with a 6% drop. This uncertainty has remained characteristic of the stock market perception of the company. Whereas the share price previously reached an absolute all-time high of around €104, it has since structurally declined under this ongoing pressure to a current price of approximately €64.50.

A New Era

This turbulent and demanding phase for the company is now being closed with a major transition in the boardroom. In the spring of 2026, it was announced that CEO Dolf van den Brink will step down from his position on May 31, 2026. Van den Brink led the company for nearly six years through a succession of crises. To steer the company through these difficult years, he introduced the EverGreen strategy, strongly focused on premiumization, LONO beers (low and no-alcohol) and substantial structural cost savings. This provides the incoming successor with a solid foundation, but also with a complex task: to excel in a shrinking beer market, protect margins against inflation and regain investor confidence.

Chapter 4: Strategy and the Growth Engine of Emerging Markets

EverGreen 2030

The operational obstacles and volume decline in traditional Western beer markets, as described in the previous chapter, force HEINEKEN to make strict strategic choices. To address these macroeconomic challenges and successfully facilitate the upcoming leadership transition in 2026, the brewer is leaning heavily on the recently launched “EverGreen 2030” strategy. This management plan forms the company’s fundamental response to a rapidly changing global playing field and builds directly on the now-completed EverGreen 2025 program. Over the years, that previous program delivered more than €3.5 billion in gross savings for the company and digitized more than €13 billion in trade value. Whereas the previous cycle was initially strongly focused on cost control and adaptability during the pandemic, the new 2030 phase is unmistakably focused on offensive and renewed value creation.

Within this EverGreen 2030 strategy, the organization has moved from five priorities back to three clear core priorities, with “Accelerate Growth” explicitly and unequivocally taking the top position on the agenda. At its core, this growth strategy is about rigorously simplifying and strengthening the brand portfolio. Instead of spreading marketing investments thinly across the full spectrum of more than 340 beers and ciders, the brewer is now focusing its capital primarily on five global pillars: Heineken, Amstel, Birra Moretti, Tiger and Desperados. This is supported locally by a strict selection of 25 so-called “power brands.” This strategy of “fewer, but bigger brands” should drive superior brand strength and sharper execution at the point of sale. To fund this commercial growth in an inflationary environment, the productivity program “Fund the growth, fuel the profit” remains an essential component. By using global scale advantages more intelligently, achieving structural cost savings and steering more tightly on cash flow, the brewer generates the required capital for reinvestment in the market.

Sustainability

Sustainability is also an important pillar within the EverGreen strategy. From an ecological perspective, reducing CO2 emissions is the key objective. For its own production and logistics - Scope 1 and 2 - the hard target is to operate at “net zero,” meaning fully climate-neutral, by 2030. Between 2022 and 2025, these absolute emissions were already reduced by 38%, mainly through the transition to renewable electricity and sustainable thermal solutions such as electric boilers and solar parks.

Water management is also essential, since without water there can be no beer production, and water scarcity can directly lead to production outages. HEINEKEN aims to reduce water consumption by 2030 to a global average of 2.9 hectoliters of water per hectoliter of beer, and to 2.6 hl/hl in so-called water-stressed areas. In addition, the company wants to be fully “water balanced” in these scarcer regions, meaning that for every liter of water consumed, 1.5 liters are returned to local watersheds.

Finally, circularity is an important means of containing material costs and external supply-chain risks, or Scope 3 risks. The company’s targets state that by 2030, nearly 99% of packaging should be designed to be recyclable and 43% of total volume sold should be offered in reusable packaging, such as deposit-return systems. By seamlessly integrating this sustainability strategy into its efficiency and growth objectives, HEINEKEN is attempting to make its growth ambitions financially and operationally sustainable for the coming decade.

The Focus on Emerging Markets

While beer consumption in mature markets is stagnating or slightly declining, HEINEKEN sees a crucial and long-term foundation in so-called emerging markets. Management explicitly states in the annual reports that the growth potential and the so-called “runway” in these emerging economies remain enormous. Continued expansion in these regions is structurally driven by a predominantly young population, increasing urbanization and a growing local middle class that gains the financial room to trade up to more expensive premium beers.

The company’s figures from the first quarter of 2026 clearly illustrate the weight of these emerging markets. While beer volume in Europe (-1.8%) and the Americas (-2.6%) declined, the Asia-Pacific (+10.1%) and Africa & Middle East (+2.3%) regions acted as such strong offsets that the company still managed to record total group-level volume growth of 1.2%. This increase was driven to a significant extent by strong organic growth in countries such as Vietnam, Indonesia, South Africa and Ethiopia. Operations in India also performed strongly; the locally positioned premium segment grew in the mid-teens, or around fifteen percent, driven in part by the Kingfisher Ultra brand. In China, the company is also reaping the strategic benefits of its focus: through an alliance with local player China Resources Beer (CRB), HEINEKEN has delivered growth there for the eighth consecutive year that has structurally outperformed the market average, while the Amstel brand’s volume even doubled in the first quarter of 2026.

In addition to this organic growth, the brewer makes highly targeted use of strategic acquisitions (M&A) to rapidly capture market position in emerging regions. In Central America, the company recently completed the acquisition of the beverage and retail operations of the large conglomerate FIFCO. The consolidation of these operations, primarily in Costa Rica where the activities were formally integrated at the end of January 2026, significantly expands HEINEKEN’s physical footprint and distribution strength. Through such targeted acquisitions, the company also gains direct access to popular local products, such as the hard seltzer brand Adan y Eva in this case. This buy-and-build tactic in emerging economies follows the successful example of the earlier multibillion-euro acquisition of Distell in Southern Africa, which added the Savanna and Bernini brands while maintaining strong volumes. Through this continued focus on scale and brand strength in emerging markets, HEINEKEN creates a robust flywheel that effectively absorbs pressure in Western markets.

Chapter 5: Pioneer in Innovation: The Operational Moat

A fundamental, structural shift in consumer behavior is taking place within the global beverage industry. Internal HEINEKEN research, the Moderation Pulse Tracker 2024 shows that 79% of consumers now actively moderate their own alcohol consumption. For traditional brewers, this changing demand represents an existential threat. HEINEKEN, however, has adopted this development as a core element of its future growth by investing heavily in new taste profiles such as Heineken Silver, the LONO segment (low and no-alcohol) and innovations beyond the traditional beer market, or “Beyond Beer.” Strategically, this innovation portfolio functions as an extremely effective economic moat.

The Rise of Heineken Silver

To continue growing within the traditional alcoholic market, the brewer has innovated in a targeted way with the introduction of Heineken Silver. This variant was specifically developed to respond to consumer demand for accessible, easy-to-drink beers with a significantly less bitter flavor profile. Silver now represents a substantial and rapidly growing part of global Heineken volume. The strategic value of this brand is especially visible in the Asia-Pacific region, where it acts as a crucial driver of premiumization. The operational strength of this innovation was clearly visible in the first quarter of 2026: Heineken Silver recorded global volume growth in the thirties, partly driven by exceptional performance in China and Vietnam, where sales volume in the latter market even increased in the forties. In doing so, Silver creates an effective defensive line against the outflow of new, younger consumers toward other beverage categories.

The 0.0 Success Story: Distribution and Scale

The foundation of the LONO moat is the global success of Heineken 0.0. The flagship is currently available in 117 countries and serves as the driving force within the alcohol-free beer category. Its operational dominance was also visible in the first quarter of 2026, when the group’s total LONO volume grew by double digits, in the low teens, heavily supported locally by regional power brands such as Maltina in Nigeria and Fayrouz in Egypt.

The real barrier for competitors, however, lies in physical distribution infrastructure. A key milestone was the large-scale rollout of Heineken 0.0 on draft. By the end of 2025, the draft installation in Europe had been successfully rolled out to more than 10,000 hospitality locations, with an average of fourteen new taps being installed daily in core markets. Securing a physical tap is competitive and creates significant customer lock-in. Smaller brewers simply lack the logistical muscle to distribute alcohol-free beer at scale in kegs, allowing HEINEKEN to lock in its market dominance through these taps. In retail environments, the company applies a similar tactic, such as in Slovenia, where the introduction of “zero zones” led alcohol-free beer to reach almost 20% of local beer revenue.

Technological Edge: The Introduction of 0.0 Ultimate

Preserving taste without alcohol requires complex technology and high research and development budgets, for which HEINEKEN recently opened a new global R&D center in the Netherlands, representing an investment of €45 million. This facility enables the company to further open up the market, leading to the launch of Heineken 0.0 Ultimate in the United States. This is a premium alcohol-free beer that taps into the broader wellness trend by combining zero alcohol, zero sugar and zero calories. After a successful test phase, distribution will be further scaled up in 2026 in markets such as the U.S., the Netherlands and Poland. This offering not only retains the health-conscious consumer, but also creates entirely new consumption moments, such as during the day or after exercise, when traditional beer would not typically be consumed.

Beyond Beer: Protecting the Demographic Flanks

While 0.0 and Silver protect the core beer business, the expansion into “Beyond Beer” serves as the defense against changing demographic preferences, including Generation Z, where taste is the main driver. In the first quarter of 2026, global Beyond Beer volume grew in the mid-single digits, strongly driven by Desperados and the strong performance of the Bernini brand within HEINEKEN Beverages, which originated from the acquisition of Distell in South Africa. In major European markets, the company is also investing selectively in winning local formulas, such as a minority stake in Tenzing, a natural energy drink in the United Kingdom, and hard seltzers and ciders such as Stëlz, SERVED, Bandida and Inch’s.

By combining superior production knowledge with massive distribution scale, HEINEKEN has created a high barrier to entry. Shifting consumer preferences therefore do not represent a weakness, but are effectively exploited as a meaningful part of the company’s structural moat.

Chapter 6: Marketing Strategy and Global Partnerships

HEINEKEN’s marketing strategy has historically been a crucial pillar beneath the company’s global volume growth and brand value. The company uses marketing not merely for brand awareness, but explicitly deploys “premium platforms” to emotionally anchor the brand within the consumer’s lifestyle. Within this strategy, however, a sharp business decision has recently been made regarding capital allocation. After an iconic partnership lasting no less than thirty years, HEINEKEN announced that its sponsorship of the UEFA Men’s Champions League will end in August 2027. This decision stems from a stricter, data-driven marketing strategy: the company wants to deploy its sponsorship budgets only on platforms where spending is in direct, proportionate relation to the value created and the expected return on investment (ROI). For the investment thesis, this is an extremely strong signal: by ruthlessly cutting historical but increasingly inefficient vanity spending, management demonstrates capital discipline. This saving fits seamlessly into the “Fund the Growth, Fuel the Profit” strategy, where more efficient marketing directly contributes to projected margin expansion (EBIT) and the creation of free cash flow for shareholders.

Despite the upcoming exit from European club football, the group remains dominantly visible through other global sports. Its decades-long partnership with Formula 1 was recently extended and expanded for multiple years. In addition, the brewer is proactively responding to new, fast-growing demographic trends through a global sponsorship of Premier Padel, the official professional padel tour. Padel is the fastest-growing sport worldwide and, with its strongly social character, where people often share a drink after a match, aligns seamlessly with the brewer’s marketing objectives. To strengthen this move, tennis legend Serena Williams has been brought in as a global ambassador for the brand. These targeted sports partnerships are financially invaluable because they serve as the primary driver of the high-margin premium and alcohol-free (LONO) categories. Data shows that 56% of F1 fans now regularly choose an alcohol-free alternative. By exclusively positioning brands such as Heineken 0.0, which dominates the global market, through these sports, the company preserves its exceptionally strong pricing power. This effectively protects and secures revenue and profitability, even when total beer volumes in Western markets decline.

Festivals as Strategic Testing Grounds and Connection Platforms

Alongside major sporting events, global music and cultural festivals form a fundamental part of the marketing strategy. The aim is to facilitate so-called “meaningful connections” with the consumer. These large-scale events provide the brewer with a unique platform to reach local audiences through globally recognized stages. A prominent and successful example of this is the brand’s active presence at the leading U.S. festival Coachella.

The brewer uses these high-energy, social environments strategically. They do not merely function as large physical points of sale, but also serve as important testing grounds for consumer behavior. In recent years, HEINEKEN has specifically tested festival-oriented activations to analyze how the message of “moderation,” or responsible consumption, can be effectively embedded in busy nightlife and festival environments. These efforts provide the company with crucial consumer data on how best to serve its target audience at the moment they actually attend a concert or race.

Responsible Consumption as a Core Message

This focus on moderation forms a structural and increasingly important part of the overall marketing mix. HEINEKEN aims not to treat social responsibility as a side issue, but to use its marketing power to make responsible consumption “cool” and aspirational.

To achieve this, the company follows the strict policy objective of investing at least 10% of the full Heineken media budget annually exclusively in campaigns that stimulate responsible consumption, such as the well-known “When You Drive, Never Drink” campaign. The 2025 results show that this standard is comfortably exceeded in practice: the operating companies jointly invested 26% of the media budget in this message, reaching an estimated 1.4 billion unique consumers worldwide. By seamlessly integrating this message into both sports and festival sponsorships, HEINEKEN strengthens its reputation while simultaneously limiting strategic risks around stricter alcohol regulation.

Normally, this is where the paid section begins.

For this company deep dive, we are keeping the full analysis free.

Below is the part we would normally reserve for paid readers: the financial foundation, cash flow map, owner yield, valuation, rating, risks, and the conditions that would invalidate our thesis.

If you find this valuable, you can support TVF enormously with a like, comment, share or restack.

Chapter 7: Valuation

In our financial model and investment thesis, we assume a balanced, neutral base case. Here, we prefer realism over speculation. On the one hand, persistent macroeconomic pressure, geopolitical volatility and the upcoming leadership transition with CEO Dolf van den Brink departing in May 2026, make an unrestrained, explosive acceleration of growth in the short term unlikely. On the other hand, the downside risk is strongly protected: through disciplined execution of the EverGreen 2030 strategy and successful innovations in the premium and LONO segments, such as Heineken 0.0 and Heineken Silver, HEINEKEN has proven that it possesses an extremely resilient moat.

This chosen model reflects the fundamental balance in the company’s current dynamics, where volume pressure and inflation in mature Western markets are being managed by structural demographic growth in emerging economies such as Vietnam, India and South Africa. This stability, combined with continued cost savings, provides the most rational and reliable foundation for our further valuation analysis.

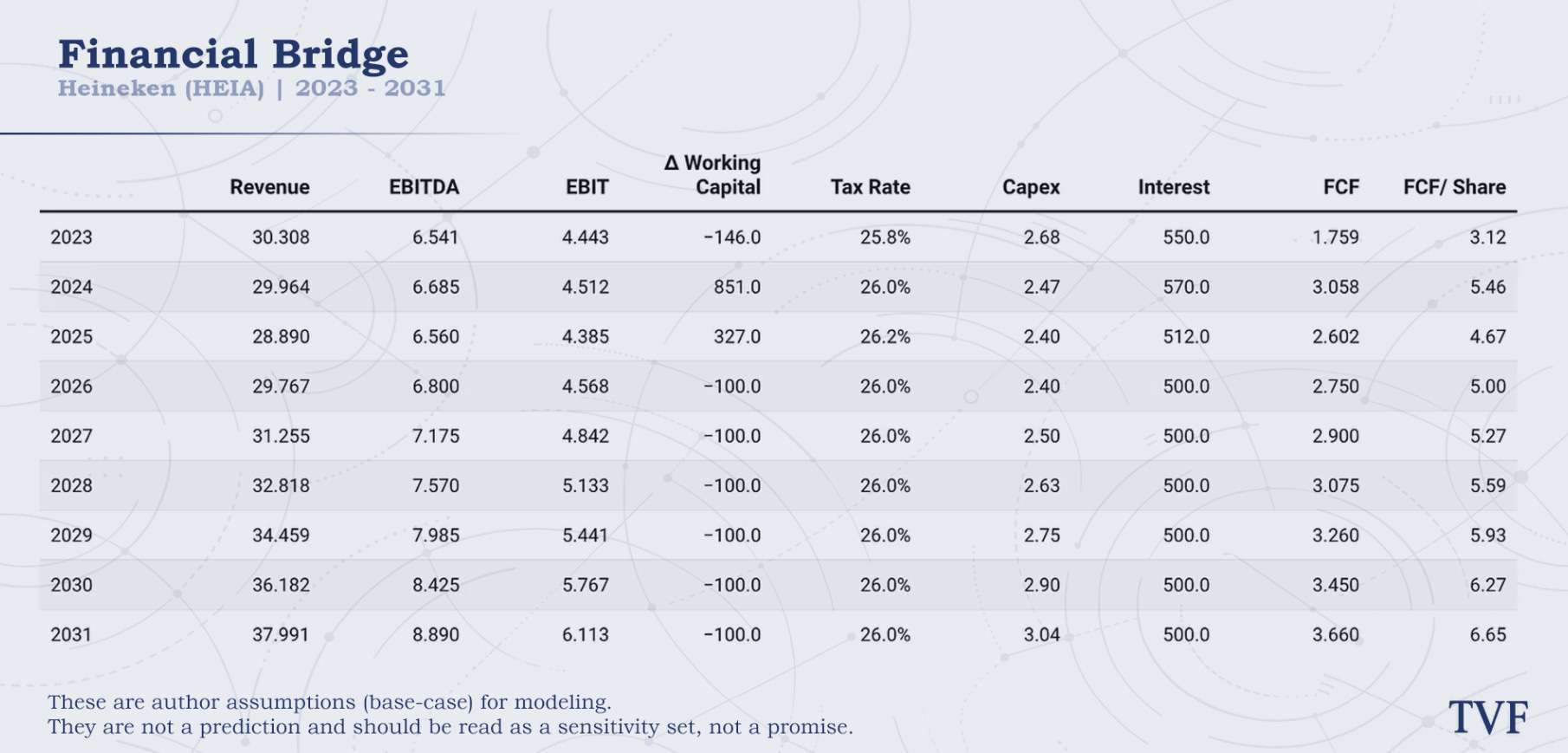

The financial projections for the period through 2031 reflect the fundamental transition HEINEKEN is undergoing. Whereas the historical years 2023 to 2025 were still heavily influenced by macroeconomic shocks and volume pressure, the financial bridge to the future shows a normalized and more profitable growth path. The assumption for structural top-line revenue growth is set at around 5% per year. This percentage was not chosen arbitrarily, but follows directly from the brewer’s own Value in Use (VIU) models, in which expectations for local volume growth and long-term inflation by region are effectively embedded.

The recent figures confirm that this is a realistic and even robust assumption. Ongoing volume pressure in mature markets, such as the U.S. and parts of Europe, is more than offset by the success of the targeted premiumization strategy. Consider the continued market dominance and rollout of the higher-priced Heineken 0.0, the explosive growth of Heineken Silver, which is performing exceptionally well in the critical Asia-Pacific region, and a relentless focus on priority markets that are expected to account for 90% of future growth. This strategic shift toward value over pure volume, combined with the proven pricing power during recent inflationary waves, structurally supports higher and safer revenue growth.

The most crucial element in the constructed bridge, however, is continued margin expansion. In the projections, the operating margin (EBIT) steadily rises toward 16.1% in 2031, up from 14.7% in 2023. This increase is the direct financial translation of the “EverGreen 2030” strategy. Through the renewed focus on productivity, with a hard operational target of €500 million in gross cost savings in 2026, strong operating leverage is created. As a result, profitability grows structurally faster than gross revenue.

Further down the income statement, we see that this profit efficiently translates into growing free cash flow (FCF). In recent years, working capital still fluctuated heavily due to normalizing supply chains. For the longer term, however, the model prudently assumes a structural investment, or outflow, of €100 million per year to support rising sales. At the same time, capital expenditure (Capex) is assumed to continue growing significantly toward more than €3 billion. This is a necessary assumption: the company’s demanding ecological requirements and net-zero targets simply require continued and substantial investment. Nevertheless, free cash flow continues to rise strongly, providing a robust foundation beneath the company’s valuation.

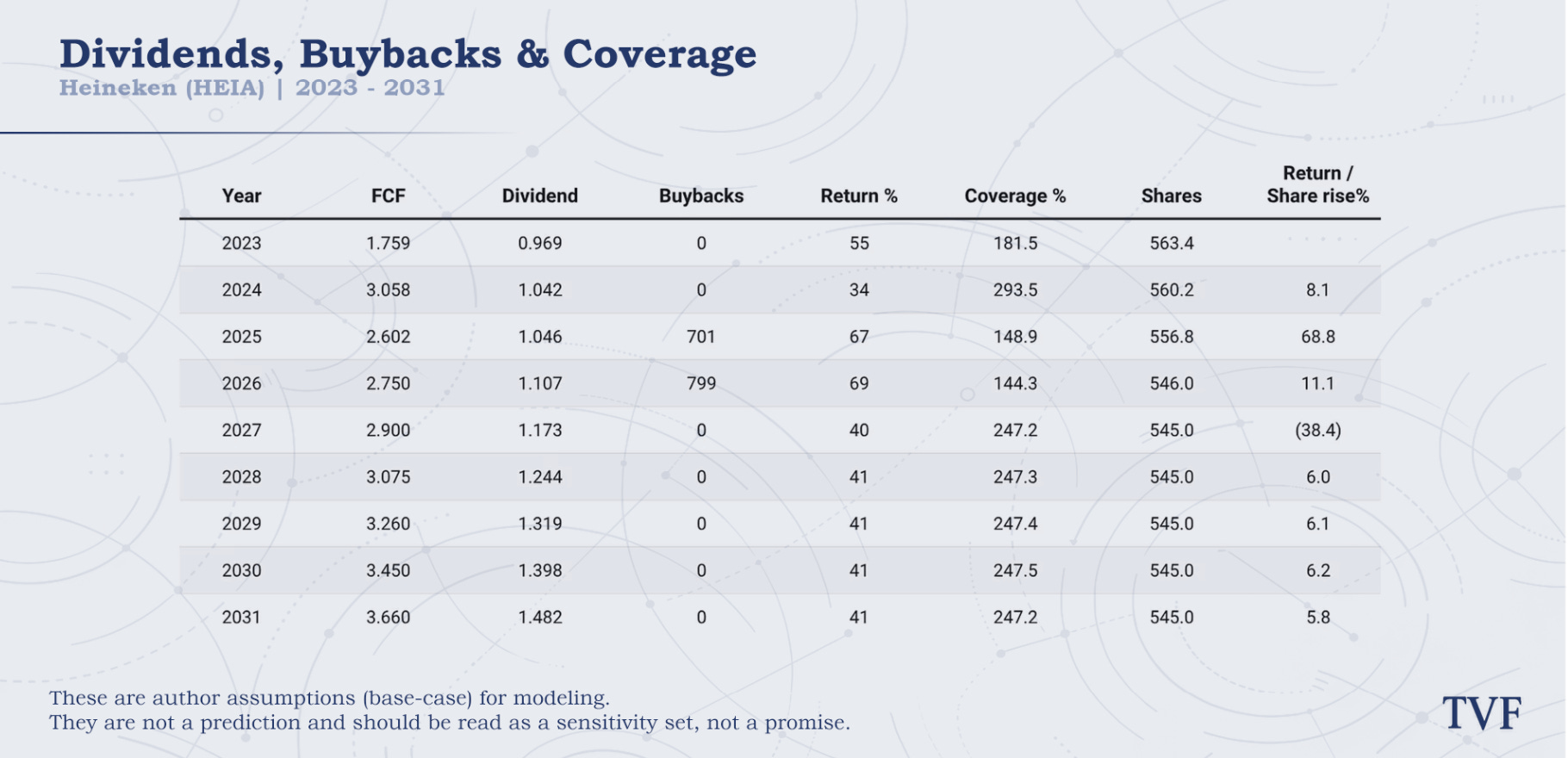

Capital Allocation: Dividend, Buybacks and Coverage Ratio

The way HEINEKEN then allocates these rising cash flows to shareholders also shows a clear shift in financial policy. The shareholder return bridge illustrates how the company is currently moving toward more active capital distributions. The dividend forms the stable foundation. In the 2025 annual report, management officially widened the dividend policy range from 30-40% to 30-50% of net profit (beia). In the bridge, the assumption is made of a constant payout ratio of around 40%. This policy choice ensures that shareholders directly benefit from margin improvements and that the absolute dividend payment grows reliably each year.

The absolute driver of rising value per share in the short term is the aggressive share buyback program worth €1.5 billion over the years 2025 and 2026. Because the company definitively cancelled more than 10.5 million shares in the spring of 2026, future earnings will be distributed over significantly fewer shares, around 545 million. The assumption in the tables that buybacks are set to zero from 2027 onward follows directly from a fundamental assumption about HEINEKEN’s strategic capital allocation. The company’s official financial policy states that sufficient resources must remain on the balance sheet to grow the business not only organically, but also explicitly through acquisitions.

In recent years, the brewer has been highly aggressive in pursuing acquisitions to future-proof its portfolio. This is clearly visible in major capital investments, such as the recent acquisition of the beverage and retail activities of Central American FIFCO for approximately $3.2 billion, and earlier acquisitions and stakes in Distell, Namibia Breweries and innovators such as Tenzing and Stëlz. The expectation is therefore that free cash flow after the completion of the buyback program in 2026 will primarily be reserved for this ongoing M&A strategy. The company will need its financial firepower for targeted acquisitions in the strategically crucial LONO segment and innovations within Beyond Beer, in order to remain relevant to younger generations and adequately serve the changing, more moderate alcohol consumer. Even if this capital shift toward acquisitions means that share buybacks stop, the model shows that structural return per share from 2028 onward continues to grow by more than 6% per year on purely autonomous operational strength.

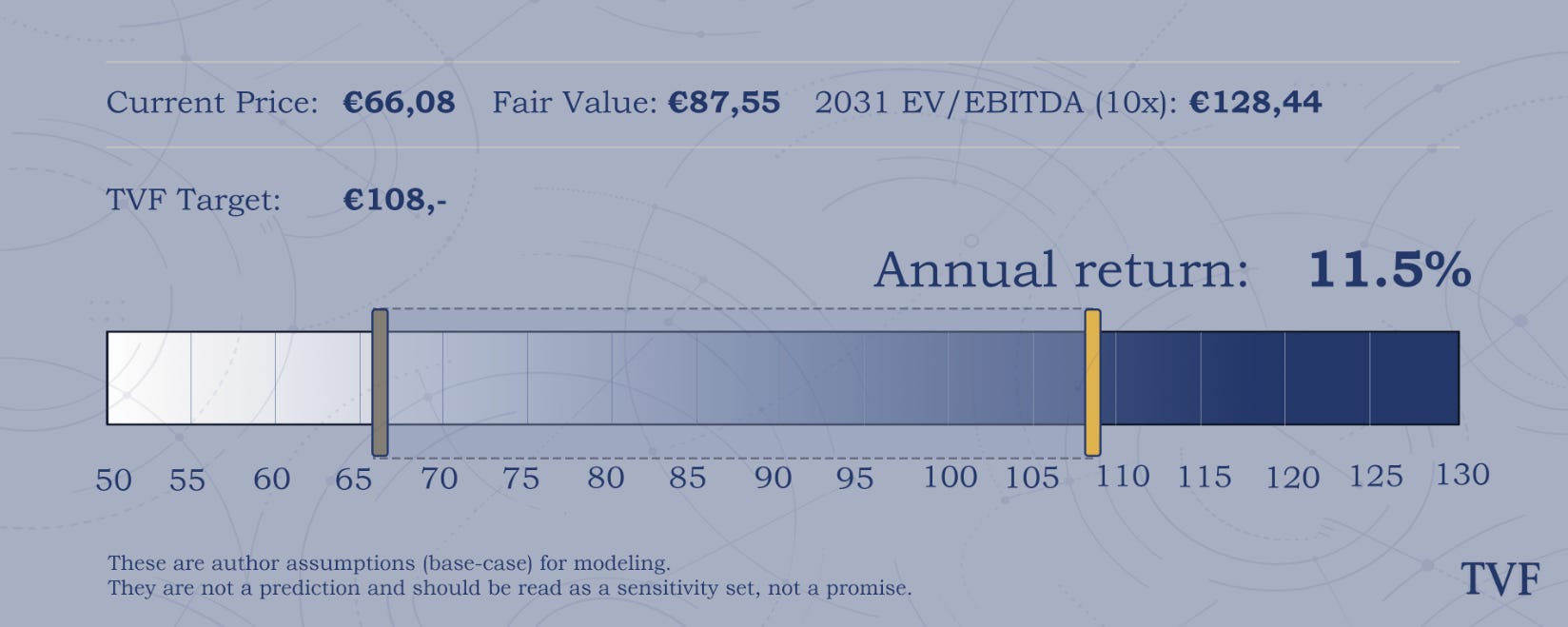

Valuation summary

Today: €66,08

DCF fair value: €87,55

Based on 7.2% WACC and 2.0% terminal growth

2031 EV/EBITDA target: €128,44

Based on 10x EV/EBITDA

TVF Target: €108,-

Expected total return: 11,46% per year, composed of:

8,43% price return

2,93% dividend yield

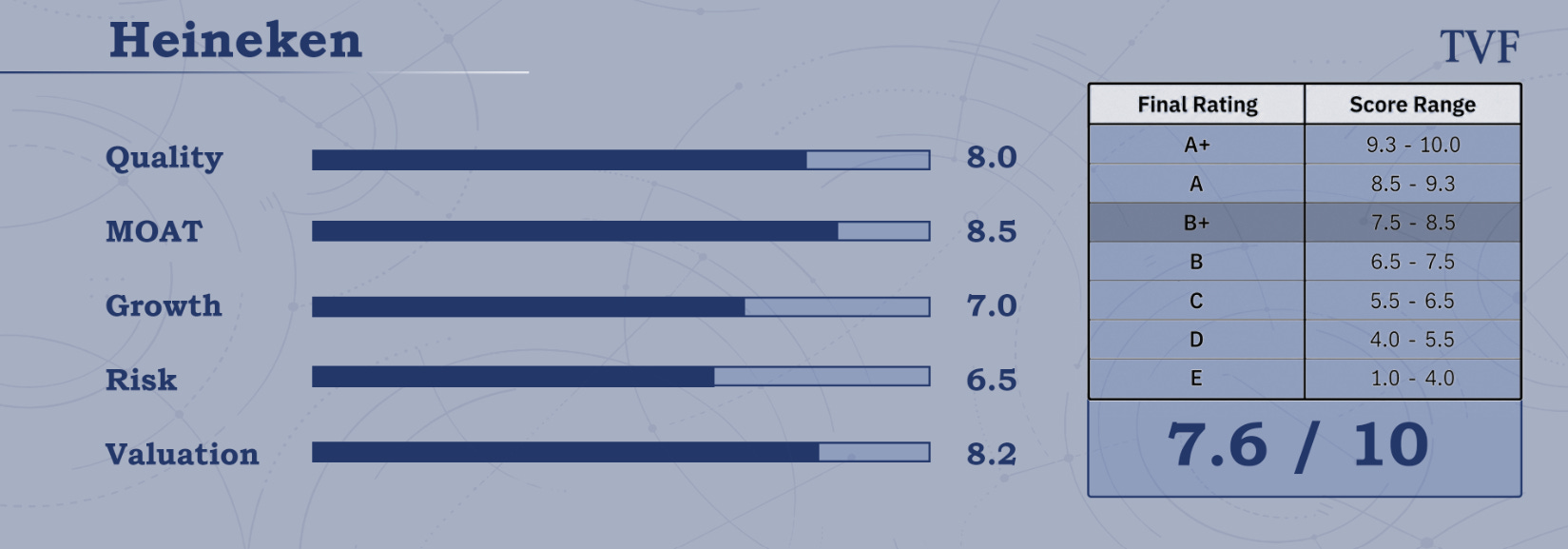

Chapter 9: Rating

Quality — 8.0/10

HEINEKEN has a fundamentally rock-solid business model with an unparalleled global footprint and a highly balanced portfolio. Although the broader beer market has recently been under pressure due to inflation and changing consumer behavior, management has shown strong operational control under the “EverGreen” strategy. Through aggressive cost savings, with a target of €500 million in savings in 2026, and strong pricing power, the company managed to expand its operating margin to 15.2% in 2025. There were some operational frictions, such as long and difficult negotiations with large European retailers that caused temporary local disruptions, but the underlying brand value remains extremely strong and the execution of the premiumization policy is highly robust.

MOAT — 8.5/10

HEINEKEN’s economic moat is exceptionally wide. The absolute dominance of the flagship brand, and specifically the global number one position of Heineken 0.0 in the alcohol-free market, is almost impossible for competitors to replicate. The distribution infrastructure, including the massive rollout of tens of thousands of 0.0 taps in hospitality venues, creates an enormous barrier for entrants. In addition, the brand successfully connects itself to premium sports platforms through multibillion-dollar partnerships with Formula 1 and Premier Padel, locking in global visibility. Finally, the extreme capital requirements for the complex sustainability transition, net zero and water compensation, act as an increasingly high barrier to entry for smaller brewers.

Growth — 7.0/10

HEINEKEN’s growth outlook is in a strategic transition phase. In Western markets, Europe and North America, physical volume is stagnating or shrinking due to the growing trend of alcohol moderation and economic pressure. However, the company is powerfully compensating for this through two axes: premium innovations and emerging markets. Innovations such as Heineken Silver, which is growing by thirty percent in Asia, and the LONO segment (low and no-alcohol) are attracting new generations of consumers. At the same time, emerging economies, particularly in the Asia-Pacific region, with +10.1% volume growth in Q1 2026 driven by countries such as Vietnam and India, and in Africa, are delivering robust volume growth and enormous long-term potential.

Risks — 6.5/10

The risks surrounding HEINEKEN shares are substantial, mainly driven by macroeconomic and geopolitical factors. The strong presence in emerging markets makes earnings highly vulnerable to volatile exchange rates and devaluations, as was recently clearly felt in Nigeria, Egypt, Mexico and Brazil. Geopolitically, the company has taken significant hits from the impairments in Russia and the forced shift to a licensing model in the unstable DRC. Furthermore, there is the risk of international trade wars and U.S. import tariffs, as well as the fundamental threat of climate change, water scarcity, which has a direct impact on brewing capacity.

Valuation — 8.2/10

The current valuation reflects the significant macroeconomic uncertainty and geopolitical punishment the stock has recently experienced. With our calculated target value of €108, the share trades at the current price, around €65, with a very substantial margin of safety relative to intrinsic value. The market currently seems blind to the structural margin improvements and is heavily focused on volume pressure in the West. For investors entering now, the shareholder-return environment is highly favorable: an expanded dividend policy of 30-50% payout combined with an ongoing €1.5 billion share buyback program. Once macroeconomic headwinds in emerging markets ease, the path is open for a significant upward re-rating toward the fair value of €108.

Conclusion: A Robust Quality Stock

HEINEKEN is anything but a wobbling giant; it is a textbook example of a resilient and relatively safe quality stock. The company has certainly taken its share of blows in recent years, from the painful impairments in Russia to ongoing volume pressure and inflation in mature markets, but it has not fallen victim to strategic arrogance. The foundations are rock solid, the global scale is unmatched and with successful premium innovations such as Heineken 0.0 and Heineken Silver, management proves that it still has a precise understanding of the changing consumer, including the trend of alcohol moderation.

Investors must face reality: the global beverage market is in a complex phase full of geopolitical headwinds. Yet HEINEKEN’s current path does not offer uncertainty, but rather tight and proven execution. The disciplined execution of the EverGreen 2030 strategy, focused on continued margin expansion and strict cost savings, with structural savings targets of hundreds of millions of euros, provides an extremely reliable floor beneath profitability. Emerging markets, where 80% of the world’s population lives, also offer enormous and long-lasting growth runway.

Given the broad operational moat and the continuous generation of strong cash flows, the risk/reward profile at this stage is highly attractive. HEINEKEN is no longer an uncertain “show me” story; the company is already structurally proving that it possesses pricing power and can realize margin recovery, supported by the recent confirmation of expected organic profit growth of 2% to 6% for the current year. Combined with a substantial share buyback program and an expanded dividend policy, under which 30% to 50% of net profit is paid out, the stock offers a comfortable cushion against market volatility. For investors looking for a defensive and safe foundation with upside potential, staying on the sidelines at these valuation levels is the least sensible position.

If macro-economics is your thing, check out our other newsletters and subscribe. We recommend:

Author: Ayden van Loon

Disclaimer & disclosures: This analysis reflects the author’s opinion at the time of writing and is not investment advice. Investing involves risks, including the possible loss of (part of) the invested capital. All valuation outputs (including DCF, price targets, and expected returns) are model-based estimates and highly sensitive to assumptions (such as cash flows, leverage, capex, discount rate, and terminal growth). Facts may be sourced from public materials considered reliable, but their accuracy cannot be guaranteed.

Position / conflict of interest: The author holds A position in Heineken. This can change at any time and without prior notice.

Note: I wrote this piece and conducted the research myself. AI was used for feedback/editing support and to generate some of the images.