The Multi-Trillion-Dollar Future of Light

Why photonics is moving closer to the bottlenecks in AI, defence, space and advanced semiconductors.

Light feels almost too ordinary to think of as an investment theme. We see it every day, we use it without noticing, and most of the time it simply feels like part of the background.

Yet the more we look at the next generation of technology, the more light starts to show up in places where the old systems are beginning to struggle. Data centers need faster ways to move information. Satellites need better ways to communicate across orbit. Defence systems need cheaper and more precise ways to detect and respond to threats. Semiconductor manufacturing already depends on light to produce the most advanced chips in the world.

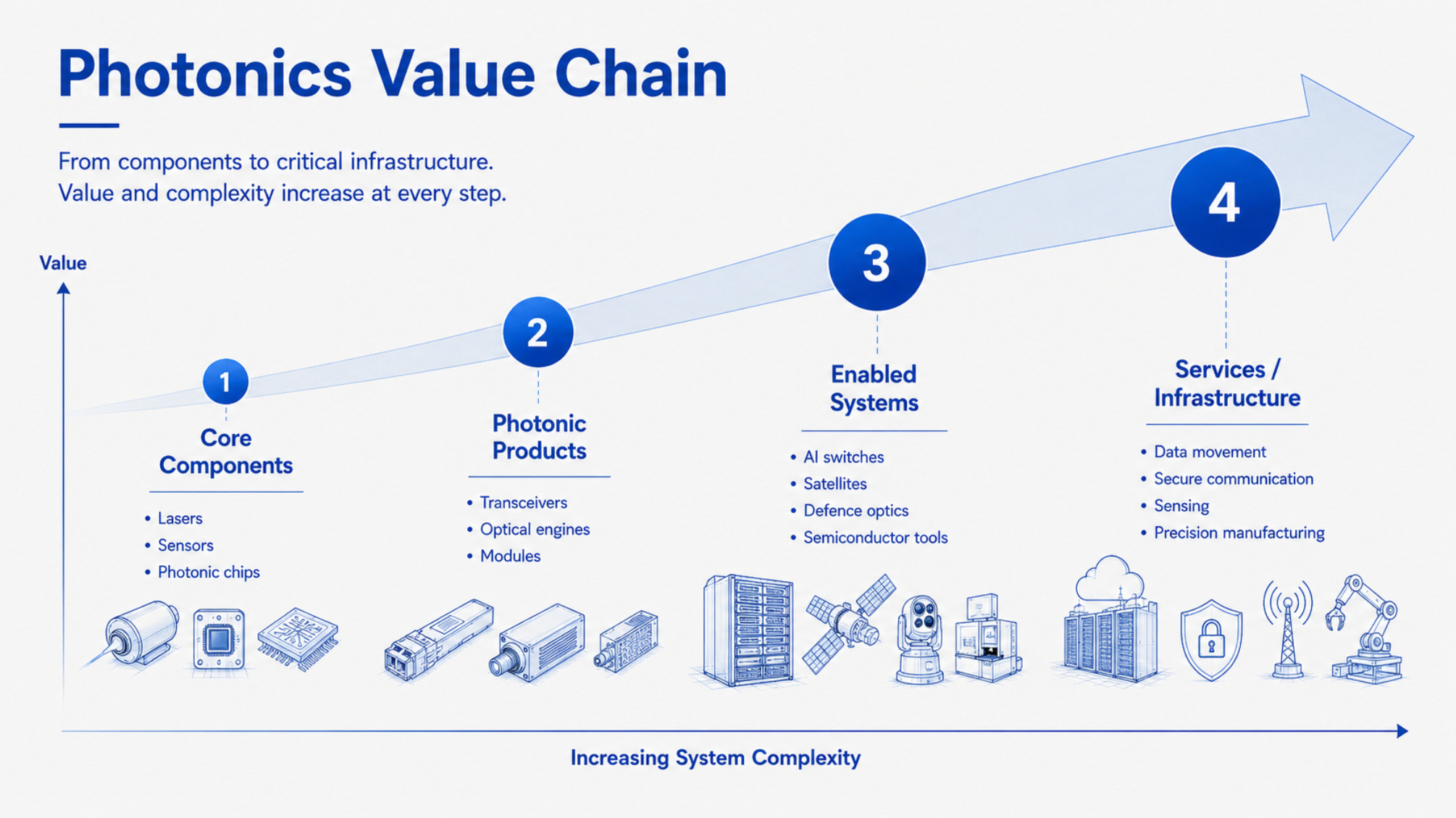

That is where photonics comes in: the use of light to transmit, detect, measure, manufacture and communicate. It is already a large market, but the broad average may not tell the most interesting story. The real question is where light moves from useful technology to critical infrastructure.

That is the theme we want to explore in this post.

Disclaimer

Do you appreciate our publication? Then you help us enormously with a like, comment, share and/or restack.

Chapter 1: A Large Market With Uneven Growth

The headline number

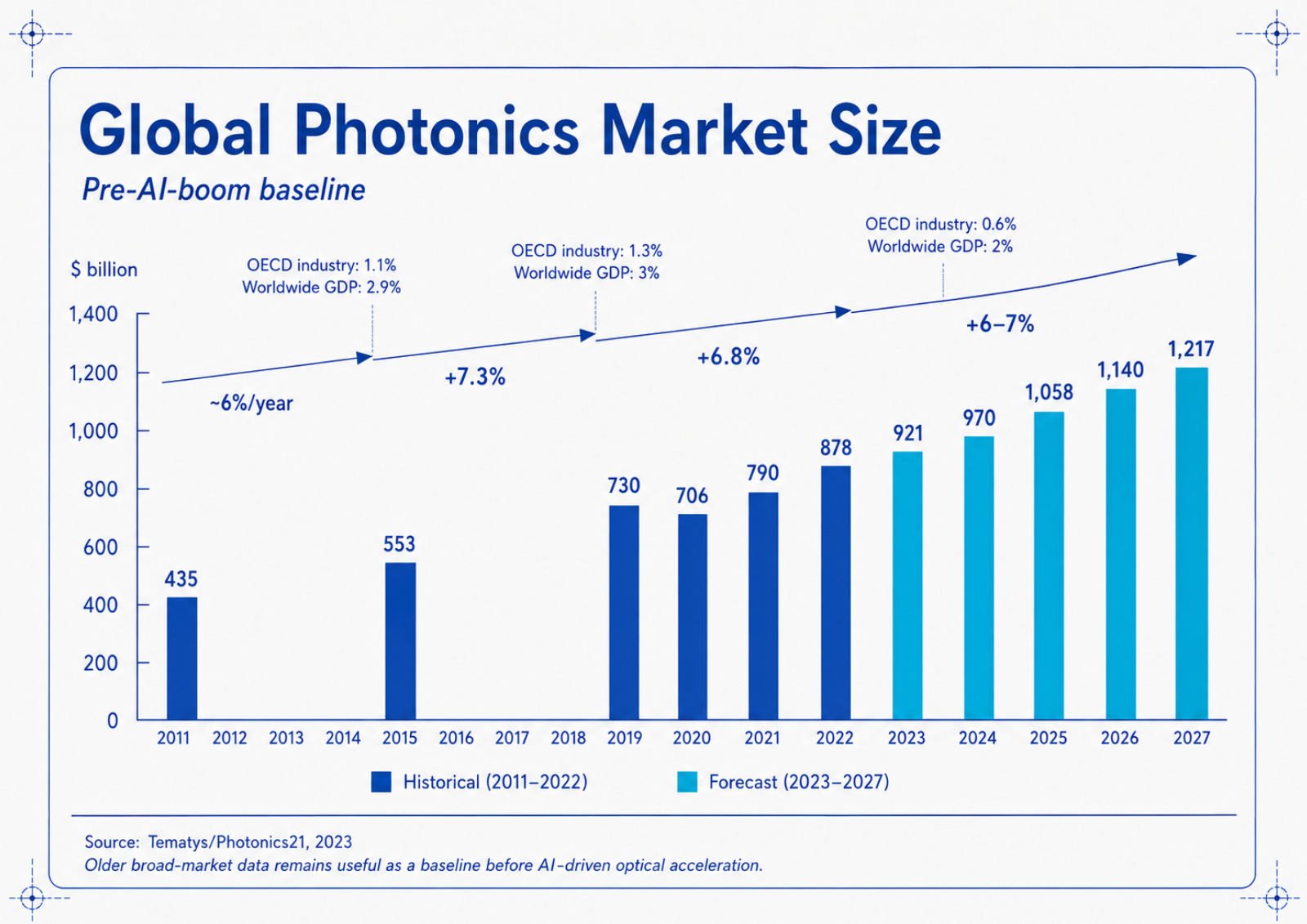

The photonics market is already large. Several estimates place the broad global market close to $1 trillion, with figures around $980 billion for 2024 and projections moving toward roughly $1.2–1.3 trillion later this decade.

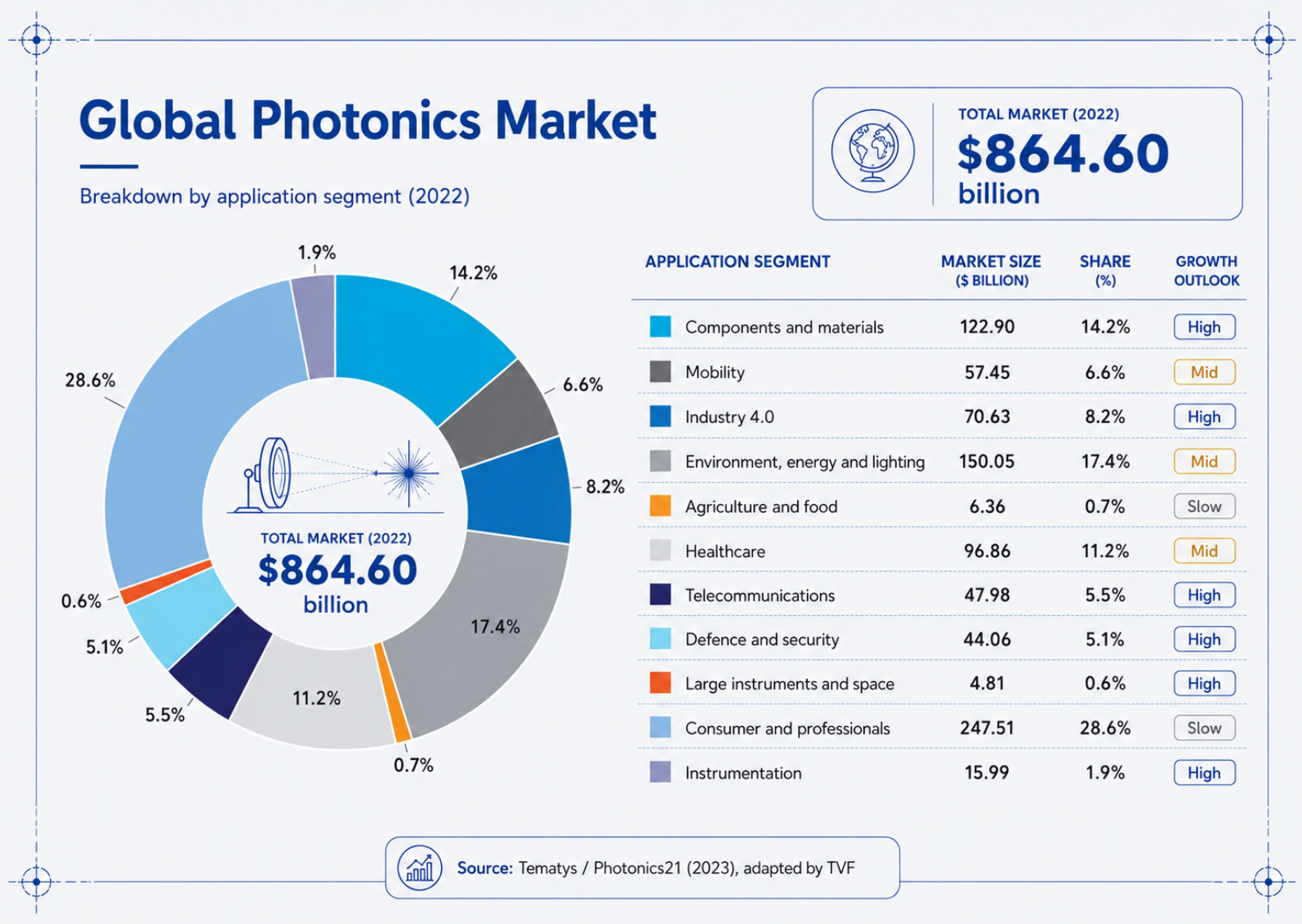

Those numbers sound impressive, but they need context. Photonics is a wide category. It covers technologies that generate, control, transmit, detect or measure light. In practice, that can mean lasers, lenses, sensors, optical transceivers, photonic chips, fibre networks, medical imaging devices, industrial laser machines, semiconductor tools and communication systems.

This creates a definition problem. Some reports focus on the core technology: lasers, optical components, sensors, transceivers and photonic chips. Others include full systems built around those components, such as displays, medical imaging equipment, industrial laser tools and communication hardware. That explains why one source can describe photonics as a near-trillion-dollar market, while another focuses on a much smaller core component market of roughly $381 billion.

For investors, that distinction matters. If a report includes a finished medical imaging machine, an industrial laser system or a display, the revenue may sit partly with companies that are not pure photonics suppliers. The investable layer may be much smaller: the laser, sensor, optical component, transceiver, photonic chip or packaging technology inside the final product.

So the headline market size is useful for scale, but it does not tell us where shareholders can actually earn attractive returns. The better question is which parts of the chain control a scarce capability, have pricing power, or solve a bottleneck that customers cannot easily avoid.

The average growth rate

The broad market does not grow at one speed. Most broad-market estimates point to steady mid-single-digit annual growth, often around 5–7%. That is attractive for a large industrial market, but it hides the shape of the underlying opportunity.

Large mature segments pull the average down. Displays, lenses, conventional lighting and older optical components already have scale, but their growth is relatively slow. These areas make photonics look stable and established.

The faster growth sits in smaller subsegments. Silicon photonics, optical interconnects, co-packaged optics, space laser communication and high-end defence optics are earlier in their adoption curves. Some of these markets are still small, uncertain or forecast-driven, but they are linked to real system bottlenecks: AI data movement, chip-to-chip communication, satellite routing, drone defence and semiconductor precision.

A simplified view of the market looks like this:

This split is the core of the thesis. Photonics already has scale, but scale alone is not the reason to study it. The more interesting question is whether specific parts of the value chain are becoming more important because older systems are starting to reach their limits.

Where light moves closer to the bottleneck

The strongest areas are the ones where light is no longer just useful, but increasingly tied to system performance.

In AI, the bottleneck is data movement. GPUs need to communicate with other GPUs, servers with other servers, and racks with other racks. As clusters scale, electrical interconnects face harder limits around distance, heat, signal loss, bandwidth and energy consumption. That is where optical transceivers, silicon photonics and co-packaged optics become more relevant.

In space communication, the bottleneck is bandwidth and routing. Laser links allow satellites to communicate directly with each other, reducing dependence on ground infrastructure and changing how data can move through a network.

In defence, the bottleneck is cost and precision. Cheap drones and repeated attacks create pressure for cheaper response layers. Light-based systems are relevant not only through high-energy lasers, but also through electro-optical sensors, infrared imaging, targeting systems and laser communication.

In semiconductor manufacturing, the bottleneck is precision. Advanced chipmaking already depends on light-based tools to produce and inspect structures at extreme scale. This is the strongest proof that photonics is not a distant concept. It is already embedded in one of the most important supply chains in the world.

Chapter 2: AI and the Copper Wall

AI is becoming a data movement problem

AI is usually discussed as a chip story. Nvidia gets the attention, hyperscalers place the orders, and investors follow the capex numbers.

But a data center is not just a room full of GPUs. Those chips only create value if they can work together. As clusters grow, the connections between chips, servers and racks become part of the bottleneck.

That is where photonics becomes relevant. AI still needs more compute, but the next phase of scaling also depends on how fast and efficiently data can move through the system. A powerful GPU is less useful if it spends too much time waiting for data from another part of the cluster.

The limits of copper

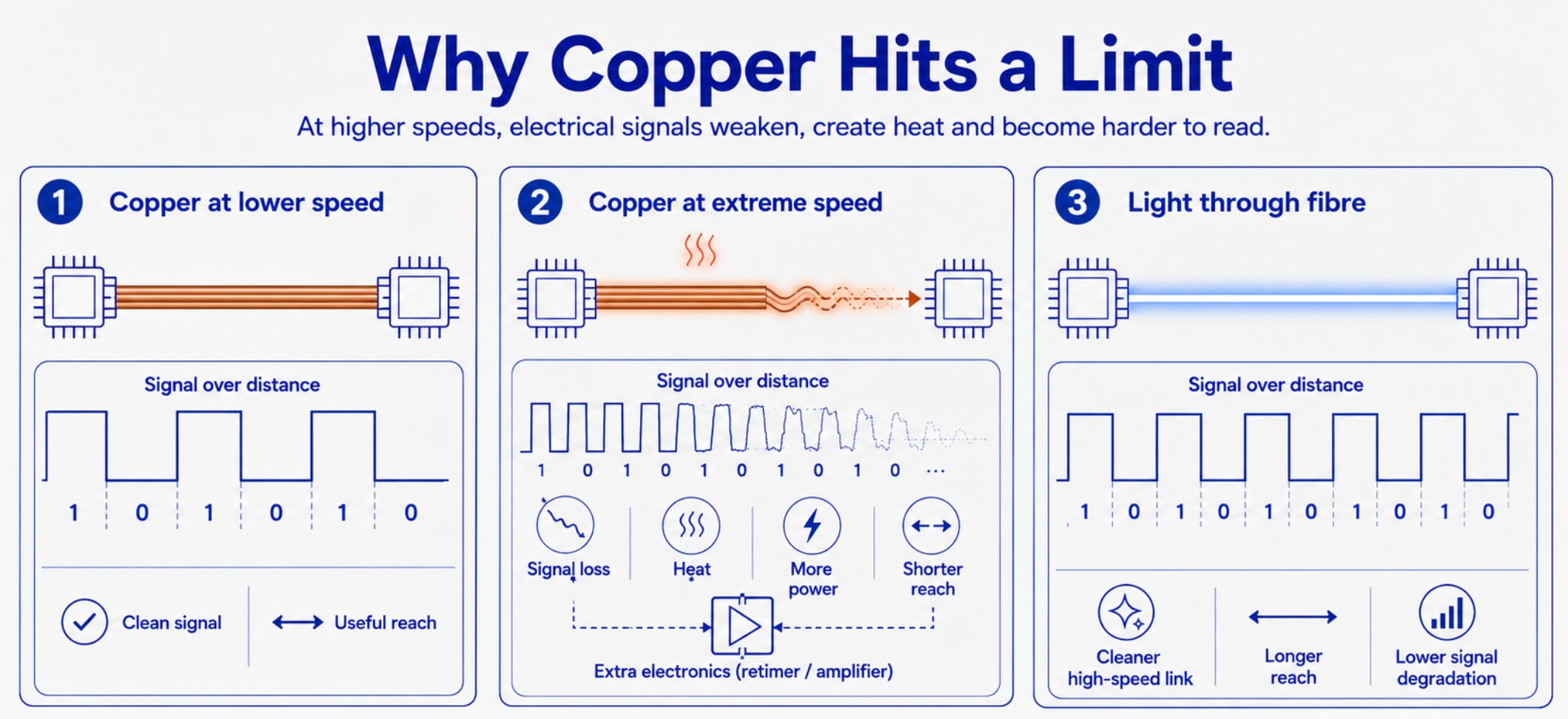

Copper has been the default material for electrical connections for decades. It is cheap, reliable, familiar and still works well in many parts of a data center.

The problem starts at extreme speeds and densities. Data moving through copper is an electrical signal. At lower speeds, that signal can stay clean over useful distances. At very high speeds, the signal weakens faster, creates more heat and becomes harder to read at the other end.

The faster the data moves, the less time there is between each 0 and 1. The signal starts to blur, and extra electronics are needed to clean it up, strengthen it or correct errors. Those extra components use power, create heat and add complexity.

This is why copper’s useful reach becomes shorter at higher speeds. In an AI cluster, that matters because data still has to move between chips, servers and racks. The larger and denser the cluster becomes, the more attractive it becomes to move high-speed data with light.

Why light helps

The basic idea is simple. Copper becomes harder to use when high-speed data has to travel further. Light can move that data through fibre with less signal loss and less electrical interference.

Data centers already use this today. Electrical signals are converted into light, sent through fibre, and converted back into electrical signals where needed. Optical transceivers are the bridge between the electrical world of chips and the optical world of fibre.

For years, that bridge mostly sat further away from the chip. Fibre was used to move data over longer distances, while copper still handled many of the shorter connections inside racks, servers, boards and switches. That worked well enough when speeds and densities were lower. AI changes the pressure on that architecture.

As clusters grow, even short copper paths become harder to scale. More data has to move between more components, at higher speeds, with lower latency and less power waste. That is why the industry is trying to move optics closer to the source of the data. Silicon photonics brings optical functions onto silicon-based platforms. Co-packaged optics moves the optical engine closer to the switch or compute chip. The goal is to reduce the distance that high-speed data has to travel through copper before it becomes light.

This is now showing up in the AI infrastructure roadmap. In 2025, NVIDIA announced co-packaged optics networking switches with silicon photonics for AI factories, with headline claims of up to 1.6 terabits per second per port, 3.5x better power efficiency and 10x better network resiliency compared with traditional methods.

The market forecasts are starting to reflect the same shift. Yole Group estimates that co-packaged optics could grow from roughly $46 million in 2024 to $8.1 billion by 2030. Forecasts like this should be treated carefully, especially in an early market, but the direction is useful. The broad photonics market may grow steadily, while the subsegments closest to AI bottlenecks can move much faster.

The real AI angle is the movement inward. Fibre has existed for decades. What changes now is where the optical layer sits. AI is pushing light deeper into the machine, closer to the chips and switches where the data starts.

Wireless communication solves a different problem. Bluetooth, WiFi and radio waves are useful when mobility and convenience matter. AI clusters need massive bandwidth, predictable latency and controlled connections between thousands of components. In a dense data center, wireless signals would create too much interference and too little capacity. The practical debate is therefore mostly between copper and fibre, with optics moving closer to the chip.

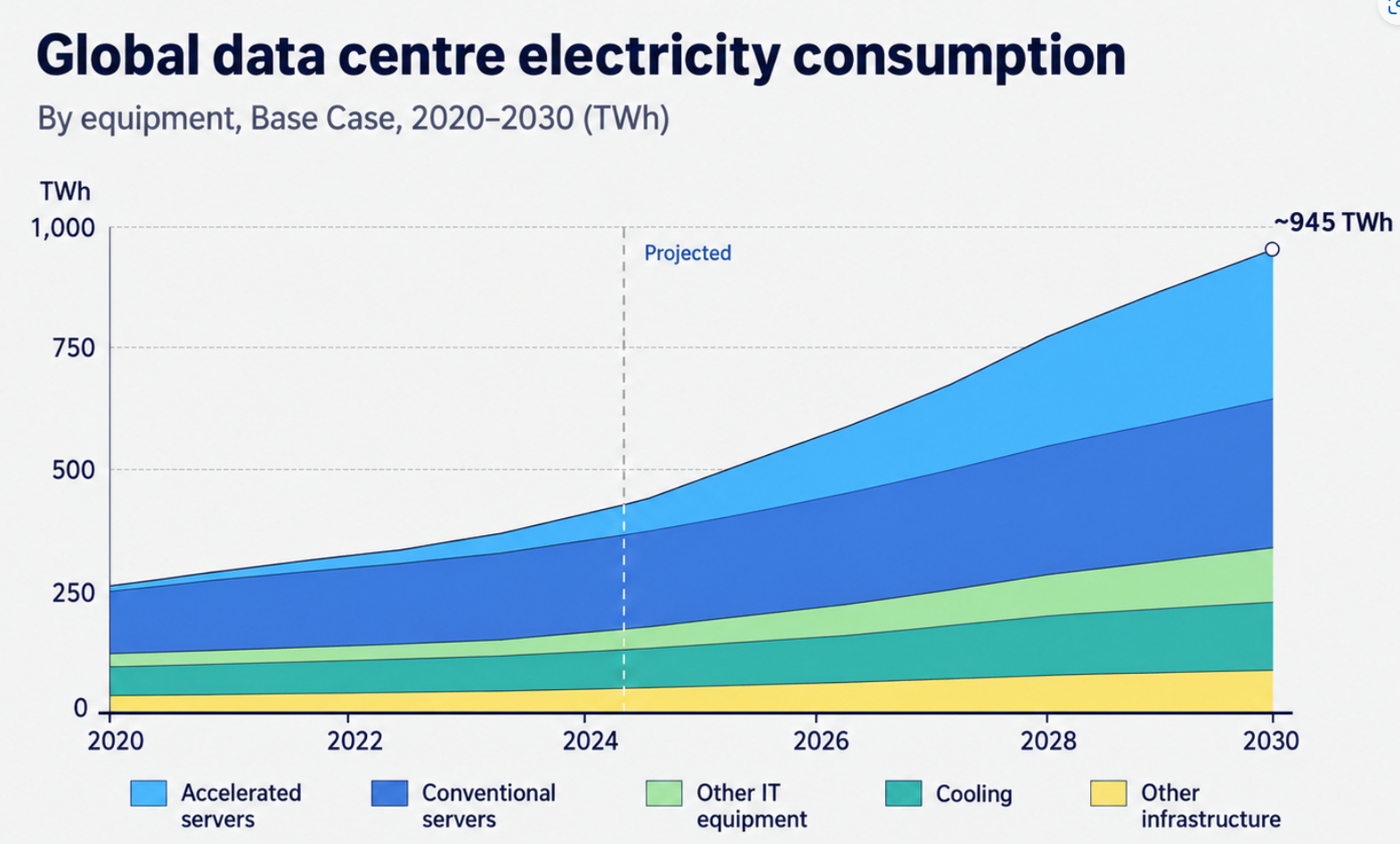

The energy angle

Data movement consumes power too. Every extra retimer, signal correction layer and high-speed electrical connection uses energy and produces heat. In a world where AI data centers already face grid constraints, permitting issues, cooling requirements and power availability, interconnect efficiency becomes part of the economics of AI infrastructure.

The research points to large differences in energy per bit between optical and electrical data movement, although the exact numbers depend heavily on architecture and source. The direction of travel is still clear: optical links can reduce the energy needed to move data across high-speed connections, especially when distance and bandwidth requirements increase.

Photonics will not solve the entire data center power problem. Compute will still consume enormous amounts of electricity. Cooling will still matter. Grid access will still matter. But interconnect power is one of the pressure points where photonics can help the overall system scale more efficiently.

That makes optical data movement more than a technical detail. It becomes part of the economics of AI infrastructure.

Copper is still essential

The copper wall should not be misunderstood. Copper is not disappearing from AI data centers. It remains essential for power delivery, electrical infrastructure, short-reach connections and the broader grid buildout. Every AI data center still needs electricity, and that electricity still needs to move through physical infrastructure.

The useful distinction is between copper for power and copper for high-speed data movement. Copper remains the infrastructure of electricity. Light becomes more interesting as the infrastructure of information.

That distinction also matters for investors. A bullish view on photonics does not automatically weaken the copper thesis. If optical interconnects help AI clusters scale further, the total demand for power infrastructure may keep growing. That can increase the need for copper in grids, substations, power distribution and data center electrical systems.

The real shift is architectural. Copper keeps moving power. Light takes on more of the high-speed data burden where copper becomes less efficient.

Where value may accrue

The AI photonics value chain is broader than the obvious AI winners. It includes optical transceivers, silicon photonics platforms, lasers, modulators, photonic chips, switches, foundries, packaging equipment and testing systems.

This matters because the companies that capture value may not be the ones most visible in the AI discussion. Nvidia may integrate photonics into its networking platforms. Broadcom and Marvell may benefit through high-speed connectivity and switching. Coherent and Lumentum may benefit if lasers become more strategically important. Foundries, packaging specialists and testing companies become relevant if the hardest part shifts from designing the optical component to manufacturing it reliably at scale.

So the opportunity is real, but the value chain is complicated. The winners may be the companies that can make photonics fast, reliable and cheap enough for hyperscale deployment.

The real AI thesis

The strongest AI thesis is focused on the frontier. Legacy systems will continue to use copper where it is cheaper and good enough. Photonics becomes most relevant in high-density AI clusters, high-speed switches, optical interconnects and architectures where data movement becomes the limiting factor.

That is enough to make the theme important. AI scaling is increasingly a systems problem. Chips matter, but the network around the chips matters too. If the cluster is the computer, then data movement is part of the compute engine.

This is why light matters in AI. It may become one of the key technologies that allows the next generation of clusters to move data fast enough, far enough and efficiently enough to keep scaling.

Chapter 3: Defence and the Cost Curve Problem

Modern threats are changing the economics of defence

The defence angle starts with a simple problem: many modern threats are getting cheaper, smaller and more numerous.

Drones are the clearest example. They can be used for surveillance, targeting, disruption or direct attack, often at a much lower cost than traditional aircraft or missiles. That changes the economics of defence. If a country has to use expensive interceptors against cheap drones over and over again, the defender may win the individual engagement but lose the cost equation.

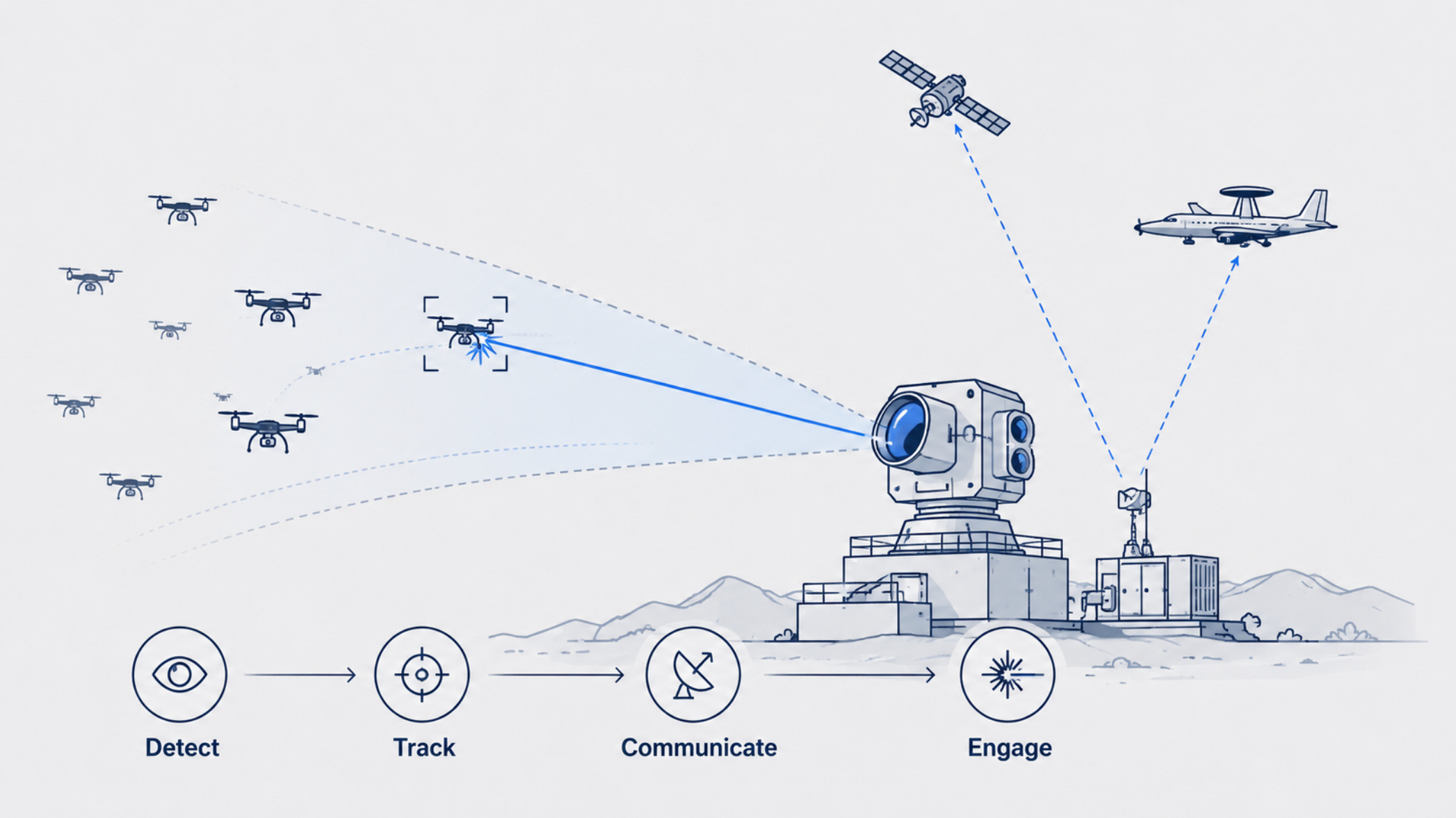

This is one of the reasons why light becomes more relevant in defence. Modern defence systems need better detection, faster targeting, lower marginal cost and more scalable response layers.

Photonics fits into several parts of that chain. Electro-optical sensors help detect and identify targets. Infrared imaging helps track heat signatures. Laser communication can improve secure, high-bandwidth links. High-energy lasers may eventually become part of layered defence systems against selected threats, especially where repeated engagements make cost-per-shot important.

The key point is that defence photonics is broader than laser weapons. Lasers get the headlines, but much of the value may sit in the less visible layers: seeing, tracking, targeting, communicating and only then engaging.

The sensor layer may be the first opportunity

Before a threat can be intercepted, it needs to be detected and tracked. This is where optical and infrared systems already matter.

Modern battlefields are crowded with drones, missiles, aircraft, vehicles, decoys and electronic noise. Radar remains critical, but optical systems add another layer. Cameras, infrared sensors and electro-optical targeting systems can help identify and classify targets, especially when they are small, low-flying or difficult to separate from the background.

This is also where photonics is already commercially and militarily relevant. Defence systems need better “eyes”: sensors that can work at long range, in difficult environments and with enough precision to support targeting decisions. As autonomous systems and drone warfare expand, the need for reliable sensing becomes more important.

That may make sensors, infrared imaging, targeting systems, optical components and laser communication equipment more realistic near-term opportunities than the most dramatic high-energy laser headlines.

Lasers are about economics, not science fiction

High-energy lasers are often discussed as futuristic weapons, but the more interesting argument is economic. Missiles are expensive. Drones and other low-cost threats can be cheap enough to create pressure on traditional air defence systems.

That is why the recent DragonFire contract matters. The UK awarded a £316 million contract to MBDA UK to supply DragonFire laser systems for Royal Navy ships, aimed at counter-drone use. The quoted cost per shot is around £10. That does not make lasers a universal replacement for missiles, but it does show why governments are interested: against repeated low-cost threats, the marginal cost of each engagement starts to matter.

Israel’s Iron Beam points in the same direction. It is being developed as an additional laser layer inside a broader air-defence architecture, alongside systems such as Iron Dome, David’s Sling and Arrow. The point is not that lasers replace the whole stack. The point is that they may become one more response layer where precision, speed and lower cost-per-shot matter.

Satellites can improve detection and targeting, but the basic physics still apply. A satellite can help detect a threat earlier, track where it is moving and send better targeting information to the defender. The laser still needs a clear path from the weapon to the target. If the target is behind the horizon, hidden by terrain, blocked by buildings or moving through conditions that weaken the beam, the satellite can tell you where the target is, while the laser may still struggle to hit it effectively.

Weather and atmosphere also matter. Rain, fog, smoke, dust and turbulence can scatter or weaken the beam. Power and cooling matter too, because a high-energy laser is an entire system that needs electricity, thermal management, tracking, beam control and integration into a platform.

So lasers are unlikely to replace missiles across the full defence stack. They may become an additional response layer, especially for point defence against selected drones or repeated low-cost threats. Missiles remain necessary when range, speed, poor weather, over-the-horizon engagement or immediate destructive force matter more. Guns, electronic warfare, jamming, sensors and kinetic interceptors also remain part of the system.

Light adds another tool where precision, speed and lower marginal cost matter. The opportunity is real, but narrower than the most optimistic laser headlines suggest.

Communication is another defence use case

Defence also needs communication networks that are fast, secure and difficult to disrupt. This is where laser communication becomes relevant.

Radio communication is flexible and proven, but it uses spectrum that can be crowded, monitored, jammed or regulated. Laser communication uses narrow beams of light. That can offer high bandwidth and a lower probability of interception, because the signal is more focused and harder to detect unless someone is directly in the path.

This matters especially in space and military networks. Satellites, aircraft, ships and ground systems increasingly need to move large amounts of data quickly and securely. Optical links can help create high-capacity communication routes between platforms, especially when resilience and low detectability matter.

There are limits here too. Laser communication requires precise pointing. Space-to-ground links can be affected by clouds and atmosphere. Military systems need to be rugged, reliable and interoperable. That makes adoption slower and more complicated than a clean technical chart would suggest.

Still, the direction is important. Defence is becoming more data-heavy, more sensor-heavy and more networked. Light can play a role as a sensing layer, a targeting layer, a communication layer and, in selected cases, an engagement layer.

The investment angle

For investors, the defence opportunity is difficult but important. Many systems are embedded inside large defence primes, government contracts, classified programs and long procurement cycles. At the same time, the underlying demand drivers are real. The battlefield is becoming more sensor-driven, drone-heavy and networked.

The most realistic near-term value may sit in components and systems that are already needed: electro-optical sensors, infrared cameras, targeting systems, laser rangefinders, optical communication terminals and counter-drone layers. High-energy lasers may become important over time, but they should be treated as one developing layer within a broader defence stack.

This is why the defence chapter fits the broader photonics argument. Light becomes more important where older systems become less scalable.

In AI, that pressure comes from data movement. In defence, it comes from cost, precision and the rising volume of low-cost threats. Both point to the same broader conclusion: photonics becomes more interesting when it moves closer to the bottleneck.

Chapter 4: Space as the Bridge Between AI and Defence

Data does not always need to follow the ground

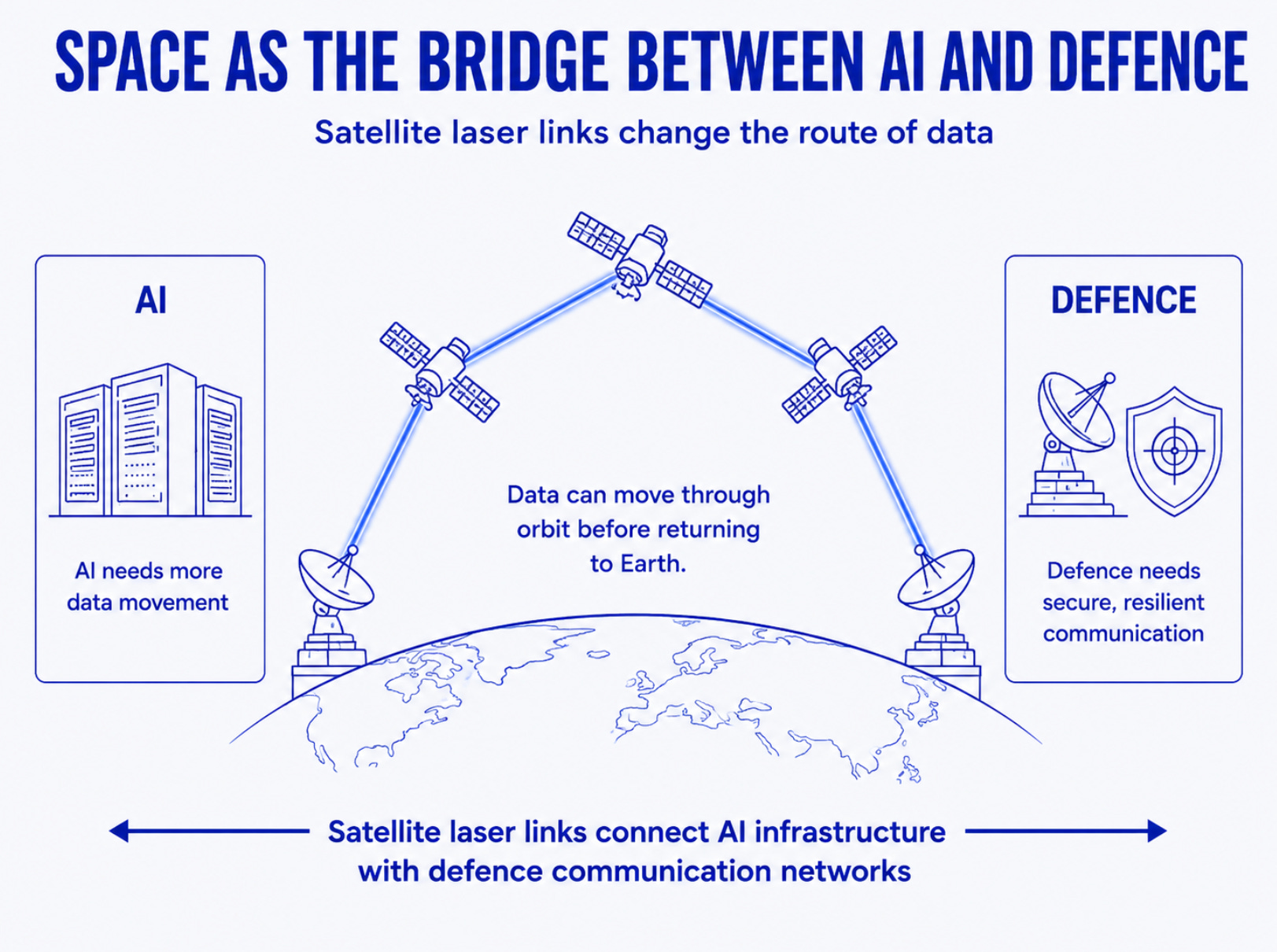

Space communication shows another way light can become infrastructure. On Earth, data usually follows physical routes: fibre networks, ground stations, submarine cables and terrestrial infrastructure. In space, laser links can change that route.

Satellite laser links allow satellites to communicate directly with each other. Instead of sending data back to a ground station first, a satellite can pass that data to another satellite through orbit. That can reduce dependence on ground infrastructure and create more flexible communication networks.

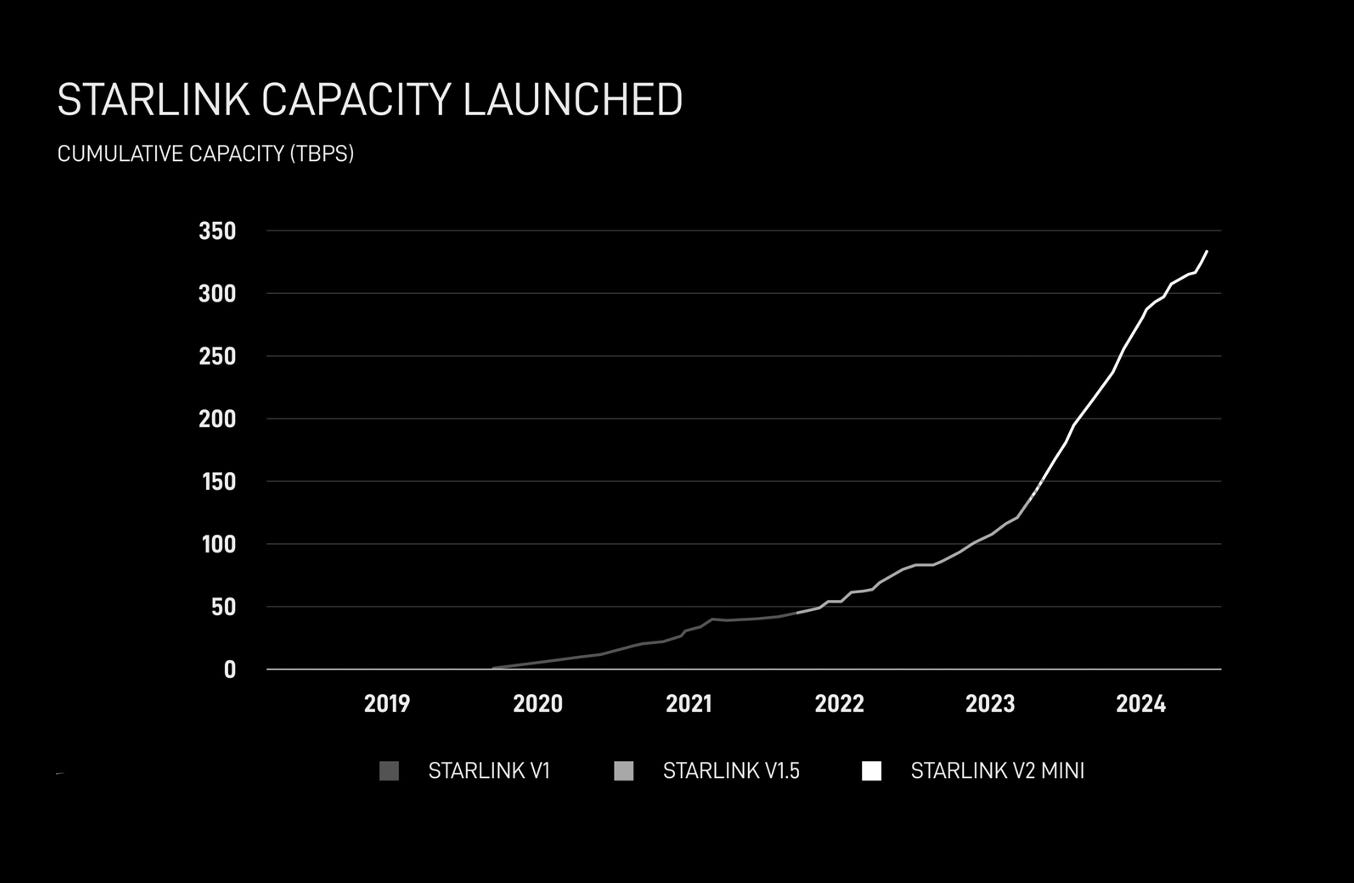

This is already visible in Starlink. In its 2024 progress report, Starlink states that each satellite contains three optical inter-satellite links, or “space lasers”, operating at up to 200 Gbps. These links allow satellites to pass data to each other in orbit instead of always sending it back to a ground station first.

That changes the network architecture. A satellite constellation becomes less dependent on the exact location of ground infrastructure, because data can move across the constellation before returning to Earth. Reuters also reported that SpaceX plans to sell its satellite laser technology commercially to other satellite companies, which suggests that laser inter-satellite links are moving from internal infrastructure toward a broader space-connectivity market.

This does not make terrestrial telecom infrastructure obsolete. Mobile networks, radio access, core networks and private 5G still need terrestrial equipment. But satellite laser links add another communication layer: one where data can move through orbit before returning to Earth.

Why light works well in space

Space is a natural environment for optical communication. There is no copper wire and no fibre cable between satellites. Radio waves still matter, but they face limits around spectrum, bandwidth, congestion and interception. Light offers another route.

Laser links can carry large amounts of data through narrow beams. That makes them useful for high-bandwidth communication between satellites, especially when networks need to move more data with lower latency and less dependence on ground relays.

There is also a physics advantage. Light travels faster in a vacuum than it does through glass fibre on Earth. That does not mean every route through space will be faster, because distance, routing and network design still matter. But it helps explain why orbital data routes become more interesting as satellite networks become denser.

The bridge to AI

Space fits the photonics thesis because it connects two large infrastructure needs.

AI needs more data movement. Defence needs faster, more secure and more resilient communication networks. Satellite laser links sit between those two needs. They can help move data across geography, connect remote systems and support networks where ground infrastructure is limited, exposed or too slow to build.

This becomes more important as AI moves into defence, logistics, remote sensing, autonomous systems and real-time decision-making. The value is not only the ability to communicate faster. It is the ability to change where data flows.

The more speculative case: data centers in orbit

The more speculative version of this idea is orbital computing. If AI data centers on Earth are constrained by power, cooling, land and permitting, space offers an obvious but difficult thought experiment: move some compute into orbit, where solar energy is abundant and geography is less restrictive.

That would make photonics even more important. A space-based data center is only useful if data can move efficiently between satellites, compute nodes and ground infrastructure. In that model, laser links become part of the basic architecture.

The caveat is large. Orbital data centers still face major technical and economic hurdles: launch costs, radiation, thermal management, hardware replacement, utilization and communication capacity back to Earth. For now, the cleaner near-term thesis is that satellite laser links are becoming a more important communication layer. Any future orbital compute model would make that optical layer even more critical.

The limits matter

Space laser communication is promising, but it should not be treated as magic. Market forecasts vary heavily depending on what is being measured. Some sources focus only on hardware, such as terminals. Others include broader services or enabled communication value. That can create huge differences in market-size estimates.

The technology also has practical limits. Laser beams need accurate pointing. Space-to-ground links face weather and atmospheric problems. Different satellite networks may use proprietary systems, which creates interoperability issues. A laser network is only as useful as the system it connects to.

That makes space a strong supporting chapter, rather than the whole thesis. It proves the architectural point: light can reshape communication networks. But the investable opportunity depends on who controls the terminals, components, standards, platforms and services around those links.

The space conclusion

Space is the bridge between AI and defence because it connects both themes through communication. AI needs more data movement. Defence needs faster and more resilient networks. Satellite laser links sit at the intersection of those needs.

The broader lesson is simple. Light can make communication faster, but in space it can also change the path communication takes.

Chapter 5: The Bottleneck Inside the Bottleneck

Photonics creates a new manufacturing problem

Photonics can help solve part of the AI data movement problem, but it also creates another bottleneck: manufacturing.

Moving data with light sounds clean in theory. In practice, optical components have to be produced, aligned, connected, tested and cooled. A fibre, laser, modulator or photonic chip is only useful if it can be integrated into the system with enough precision and reliability.

That becomes harder when optics move closer to the chip. Traditional optical transceivers can sit at the edge of networking equipment. Silicon photonics and co-packaged optics push the optical layer deeper into the system. That can reduce the distance high-speed data has to travel through copper, but it also makes the package more complex.

This is the bottleneck inside the bottleneck. AI clusters may need photonics to move data more efficiently, while photonics itself needs better packaging to scale.

Precision and reliability decide adoption

Electronics and photonics do not behave in exactly the same way. Electrical connections are relatively forgiving compared to optical ones. Light needs precise alignment. If an optical connection is slightly off, the signal can weaken or fail.

That makes packaging and testing more important. Optical fibres, lasers and photonic chips need to be aligned with extreme accuracy, and the system has to work electrically and optically at the same time. The research we collected suggests that packaging and testing can represent a very large share of total module cost. The exact number needs a source check, but the direction is clear: the challenge is making photonics reliable, repeatable and cheap enough for hyperscale deployment.

Reliability becomes more important as optics move closer to expensive switches or compute chips. A pluggable optical module can be replaced. A deeply integrated optical engine is harder to service. If a laser or optical component fails inside a tightly integrated package, the consequences can be much larger than the cost of the failed part itself.

Thermal sensitivity adds another layer. Data center racks are already becoming hotter and denser. Adding more optical functionality closer to the chip can improve data movement, but it also increases the need for better thermal management and system-level design.

This is why adoption may be uneven. The physics can be attractive while the manufacturing curve still takes time. Hyperscalers may want the efficiency gains, but they also need technology that can run at scale without turning into a maintenance problem.

Besi as a packaging example

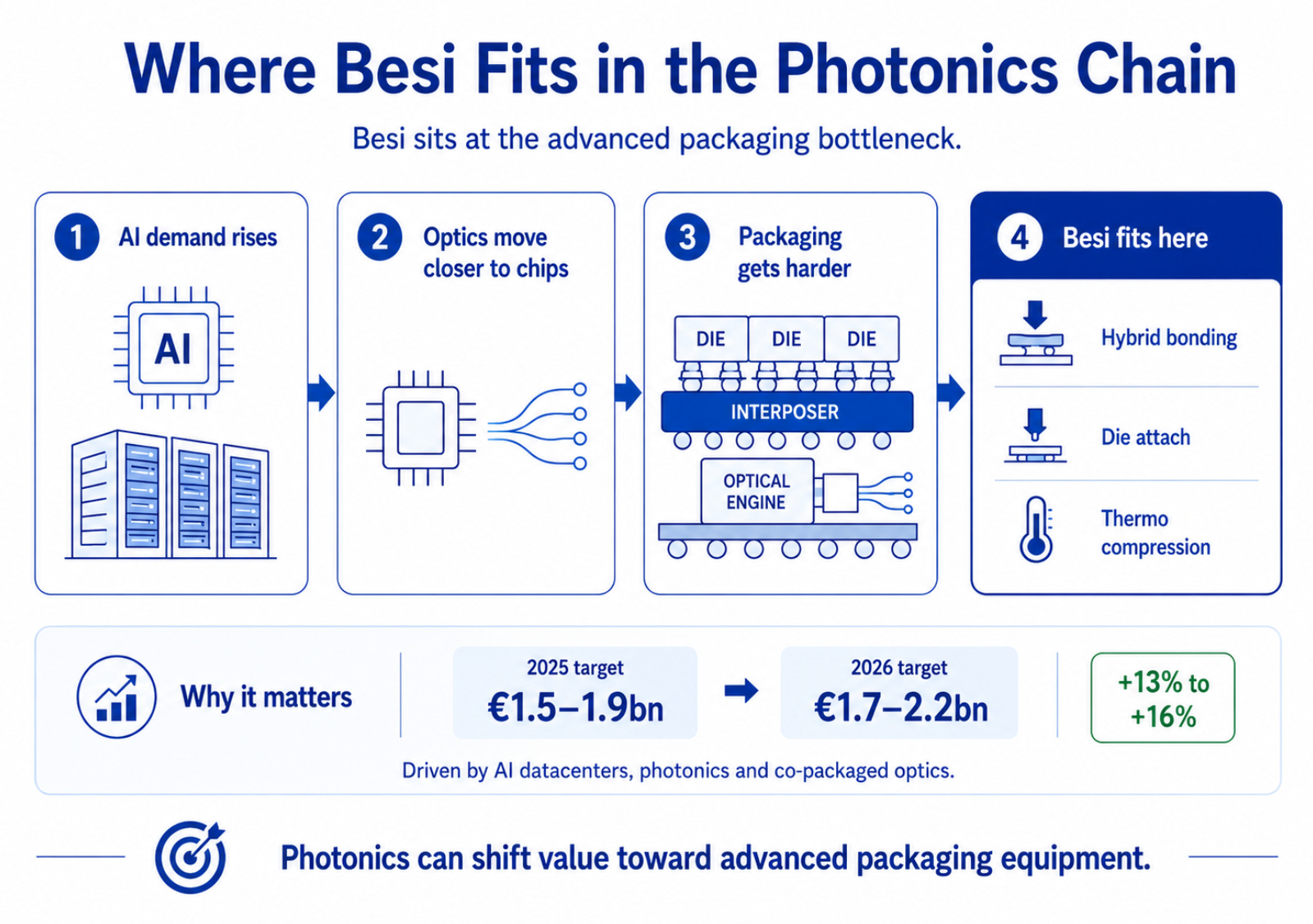

This is where a company like Besi becomes interesting. Besi is not the obvious name in a light-based investment theme, and it does not need to be a pure photonics company to matter. If the bottleneck shifts toward advanced packaging, the equipment used to assemble complex chip packages becomes part of the story.

Besi supplies semiconductor assembly equipment and is strongly associated with advanced packaging and hybrid bonding. That is relevant because high-performance chips increasingly depend on combining different dies, materials and interconnect layers with very high accuracy.

For photonics, this matters because optics moving closer to chips requires more than a good laser or photonic chip. It requires the ability to assemble optical and electrical parts into a package that works reliably at scale. If that becomes the bottleneck, advanced packaging equipment companies may sit closer to the value creation than the first reaction would suggest.

The point is subtle. Besi is not automatically a photonics winner. But photonics can make packaging a larger part of the investment case. Companies that help the semiconductor industry bond, align, assemble and test increasingly complex packages may gain indirect exposure to the same trend.

The real risk

The biggest risk in this part of the thesis is that photonics remains too expensive, too customized or too difficult to manufacture at scale.

A technology can be better on paper and still lose time in the market if it is hard to package, hard to test or hard to repair. Copper remains attractive where it is cheap and good enough. Traditional pluggable optics remain attractive where serviceability matters. Co-packaged optics and deeper optical integration need to prove that the performance gain is worth the added complexity.

That makes this chapter important for the broader thesis. Light may solve several bottlenecks, but photonics has bottlenecks of its own. The winners may be the companies that turn optical performance into industrial production.

The packaging conclusion

The photonics opportunity is not only about moving data with light. It is also about making light manufacturable.

AI may create the demand for faster data movement. Silicon photonics and co-packaged optics may provide part of the technical answer. Packaging, testing and reliability will decide how quickly that answer can scale.

For investors, this is where the theme becomes more interesting and more difficult at the same time. The visible story is about lasers, fibre and optical data movement. The investable story may also sit in the less visible layer: the equipment, processes and companies that make photonics reliable enough for mass deployment.

Chapter 6: What This Means for Investors

The investment conclusion is more complicated than the technology conclusion.

The technology conclusion is clear enough. Light becomes more important when older systems start to struggle with bandwidth, distance, heat, precision, cost or resilience. That is why photonics shows up in AI data centers, satellite networks, defence systems, semiconductor manufacturing and advanced packaging.

The investment conclusion is harder. Photonics is not one clean sector. It is a technology layer spread across many different markets. Some of the purest companies are private. Some listed companies have photonics exposure, but only as part of a much larger business. Others may benefit indirectly through equipment, packaging, testing or system integration.

That means investors should not treat this as a simple theme basket. The better question is where the bottleneck sits, who controls that layer, and whether the economics are attractive enough to matter for shareholders.

A company can have photonics exposure and still be a weak investment if it sells commoditized components, lacks pricing power or sits too far away from the bottleneck. Another company may never market itself as a photonics company, but still benefit if it controls a critical layer in packaging, testing, lasers, sensors or semiconductor equipment.

That is why this post should be read as a map, not a stock-picking list. The goal is to understand where light is becoming more important, where the system is under pressure and which parts of the value chain deserve deeper research.

The investable theme is real, but selective. Photonics will not reward every company connected to optics. It will likely reward the companies that turn light into something customers need at scale: faster data movement, better sensing, more precise manufacturing, cheaper defence layers, more resilient communication or more reliable advanced packaging.

Final Conclusion: Light Is Becoming Infrastructure

The most important takeaway is that photonics is already large, but market size is not the main reason it is interesting.

The real reason is that light is moving closer to some of the hardest bottlenecks in modern technology. AI needs more efficient data movement. Defence needs better sensing, targeting, communication and lower-cost response layers. Space networks need higher bandwidth and more flexible routing. Advanced chipmaking already depends on light, and advanced packaging may decide how quickly optical systems can scale.

That makes photonics different from many technology themes. It is not one product cycle or one end market. It is a deeper enabling layer. In some areas, it is mature and steady. In others, it is still early, uncertain and difficult to manufacture. The broad market may grow at a moderate pace, while specific subsegments grow much faster because they sit directly on top of system bottlenecks.

That also means the theme needs discipline. Some forecasts are too broad. Some markets are still small. Some applications are technically difficult. Defence adoption can be slow. Space communication still has practical limits. Co-packaged optics and silicon photonics still need to prove reliability, cost and manufacturing scale.

But the direction is important. The world is asking more from its infrastructure: more data, more precision, more resilience, more bandwidth and more efficiency. Copper, radio, missiles, ground networks and traditional packaging will all remain important, but light is taking on a larger role where those systems become less scalable.

That is the core of the thesis.

Photonics is interesting because old systems are being pushed to their limits, and light is becoming one of the ways the next layer of infrastructure gets built.

If macro-economics is your thing, check out our other newsletters and subscribe. We recommend:

Author: Jeffrey Kieboom

The Valuation Framework (TVF) turns market and sector news into clear economic models and links those themes to company notes that translate insights into valuation.

This publication is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. It does not take into account your personal financial situation, objectives, or risk tolerance. Investing involves risk, including the risk of loss. Any scenarios, estimates, and forward-looking statements reflect judgment at the time of writing and may change without notice; outcomes may differ materially. The analysis is based on publicly available sources believed to be reliable, but accuracy, completeness, and timeliness are not guaranteed. References to companies, commodities, and markets are illustrative and not endorsements. I may hold positions in securities mentioned, and those positions may change at any time. Nothing in this publication is intended to encourage or facilitate the circumvention of sanctions or other applicable laws and regulations.

Note: I wrote this piece and conducted the research myself. AI was used for feedback/editing support and to generate some of the images.